IDFC First Bank, formed by the consolidation of IDFC Bank and Capital First in 2018 and subsequently simplified by a reverse merger with IDFC Limited in 2024, has evolved from an infrastructure-biased lender to a retail-oriented private bank. The bank now offers a comprehensive bouquet of products and services in retail, wholesale, and wealth management with a clear mandate of building its granular liability franchise.

During Q1 FY26, the bank recorded robust growth with funded assets increasing 21% year-on-year to ₹2.53 lakh crore and customer deposits up 26% at ₹2.57 lakh crore. Retail deposits now account for 80% of the base versus merely 27% at merger time, and CASA ratio touched 48%. Borrowings structurally declined to 10% of liabilities from 48% previously, and the credit-to-deposit ratio has relaxed to 93.4% from 137%, indicating a better funding profile. This has come with a consistent downtrend in cost of funds, reducing the premium over peers.

On financing costs, net interest margin softened to 5.71% due to repo rate pass-through and decline in the microfinance business impacting spreads. However, net interest income increased 5.1% year-on-year to ₹4,933 crore, or 11.8% if the impact of MFI is excluded, while fee income increased 8.5% with 91% being from retail segments. Operating expenses moderated to aid for improved efficiency. Profit after tax was at ₹463 crore, rising 52% quarter-on-quarter but decreasing 32% year-on-year, as provisions stayed high at ₹1,659 crore.

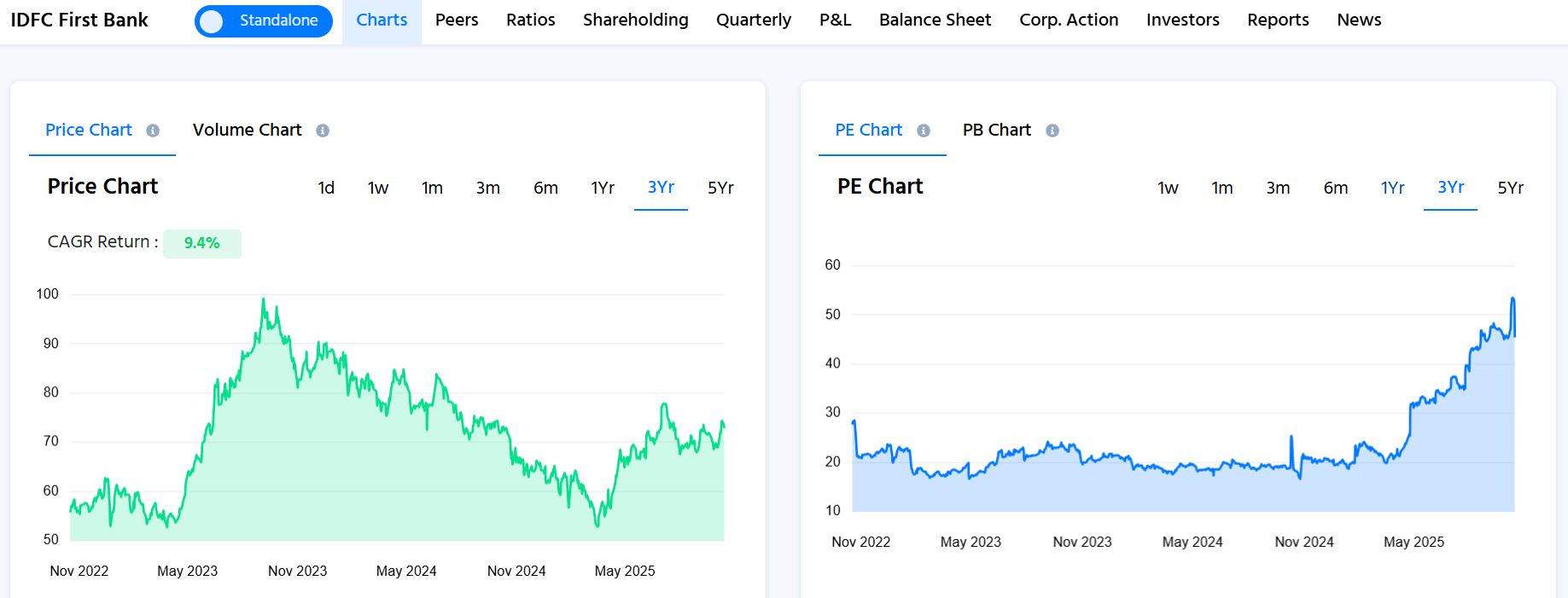

The stock’s return profile shows a mixed trend, with one-year CAGR at -7.5% reflecting weak near-term performance, while the three-year CAGR of 13.9% and five-year CAGR of 17.7% indicate steady wealth creation over longer periods. This suggests that despite recent corrections, the stock has rewarded patient investors over time. On the valuation side, the PE chart remained broadly stable in the 18-22x range for almost two years but witnessed a sharp re-rating from late 2024 onwards, now trading above 45x. Such a rise signals higher market optimism around earnings growth and structural improvements, though it also leaves limited margin of safety in the near term unless profits expand meaningfully

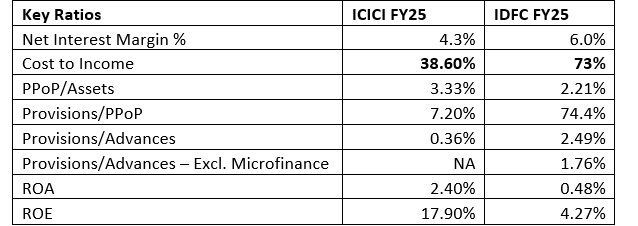

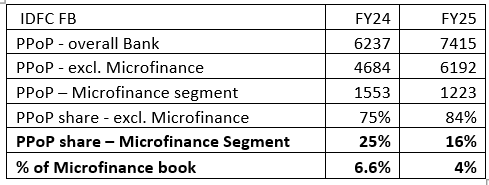

Asset quality remained healthy with gross NPA of 1.97% and net NPA of 0.55%. Provision coverage ratio was healthy at 72.3%. The MFI portfolio contracted 37% y-o-y to ₹8,354 crore, now only 3.3% of total assets, but with better collection efficiency at 99%. Slippages increased to ₹2,486 crore, although management clarified that retail and MSME segments are still robust.

Growth drivers were mortgages, auto finance, business banking, and wholesale loans that together accounted for 82% of overall growth. Wholesale exposures remain to exhibit excellent credit quality with 77% rated A and above, while concentration risks have decreased and infrastructure lending has approached zero to less than 1% of the book. An equity raise of ₹7,500 crore planned will bring capital adequacy to 17.6% and CET 1 ratio to 15.38%.

The President of India (Government) holds ₹4,572.67 crore. The government’s stake started around 3.69%, rose to a peak of 9.11%, and is currently 9.09%, reflecting a substantial and largely stable ownership. Ashish Dhawan’s current holding is ₹634.55 crore, with his stake gradually increasing from 0% to 1.26%, indicating a small but steadily growing position.

Forward-looking, management is anticipating credit costs of 2% for FY26, NIM recovery to 5.8% in Q4 as repricing of deposits filters through, and cost-to-income ratio declining towards 65% by FY27. Credit card and retail liabilities businesses are approaching breakeven, reflecting structural enhancements.

Curious to hear members’ opinions on IDFC First Bank’s recent performance and return trends.Keen to know how others view its strategy, funding profile, and growth drivers.

-

How do you view IDFC First Bank’s shift from infrastructure to retail lending?

-

With retail deposits now at 80% and CASA at 48%, do you think the funding profile is sustainable?

-

How do you interpret the stock’s mixed return trend (-7.5% 1-year vs. +13.9% 3-year CAGR)?

-

Do you see the high provisions in Q1 FY26 as a temporary factor or a structural challenge?

Which growth segments, mortgages, auto finance, or business banking, will drive the next phase?