ICICI Prudential Life Insurance Company, India listed in 2016.

It sells life insurance products and manages mutual funds under “ICICI Pru” and earns fees from the same.

The rationale for investment

The company is around since 2000 and is a stable company and a leader among private insurance companies

Life insurance penetration in India will continue to grow as it is still behind global benchmarks

Private insurers have steadily won more market share against LIC

In Buffett terms, insurance companies enjoy “float” which means they collect premiums first and have to pay dues only when claims are raised by people. The company can meanwhile invest this float and earn returns, like all insurance companies do. The company has strong “Free Cash Flow” , a measure of shareholder value creation

It has decent managment and pedegree

At the moment it is the only listed pure play life insurance co. It may at some point become part of Nifty index, etc. Also MFs looking for sectoral diversification may have to buy it. Due to these reasons, some more institutional buying of the stock may happen over the long term.

Risks

It is relatively expensive right now (July 2017) at a PE of 40. Thus there may not be any immediate 1-2 year gains

Like many financial stocks, it may fall 40-50% in case of a market crash.

More than 70% of the insurance product it sells are ULIPs i.e. Unit Linked Insurance Plans. In case of a long-term market correction, customer interest in ULIPs may also fall.

Disclosure: The author is invested in this company.

Disclaimer: This is not a recommendation for investment. The author is not a financial adviser. Do your own research before investing in any securities.

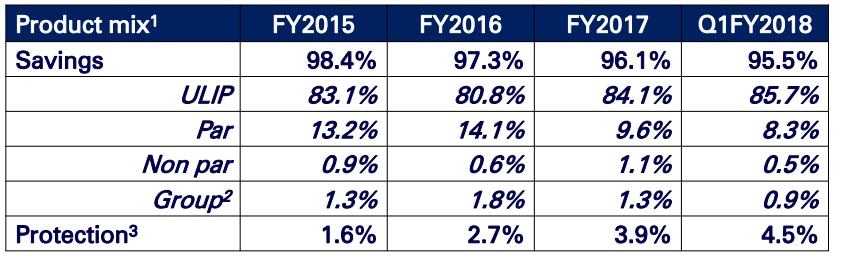

the company has been trying to improve the protection as a % of mix.

Moreover in case of life insurance business costs are front loaded which can be observed from the fact that the company pays a higher commission on new premium. Key Performance Indicators

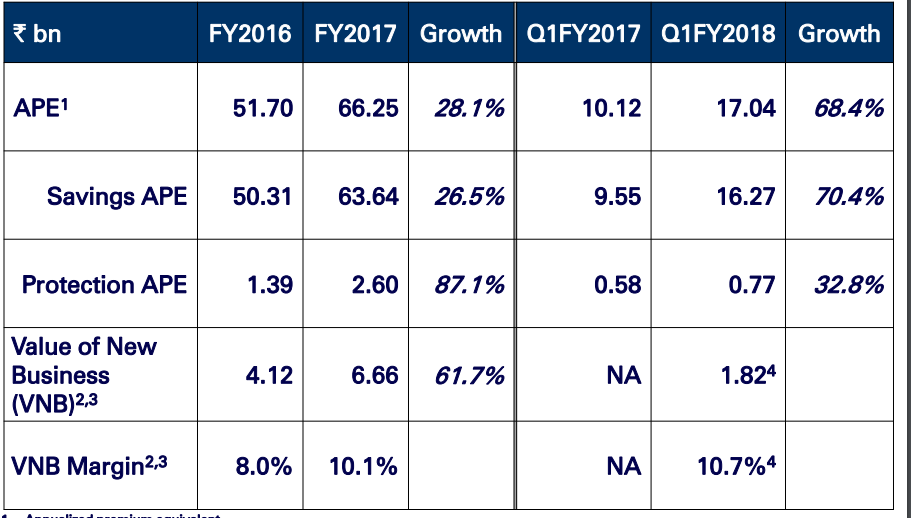

1.As regards Q1 the company has grew its APE (Annualised Premium Equalivalent) at 68.4% while industry growth has been 15.3%

2. The company has been able steadily persistency across periods

3.The company has been steadily been able to increase the value of new business that it underwrote in the quarter and increase the new business margin.

4. The company has a wide access to customers due to ICICI Bank

Key Risks

How will mass surrenders in ULIPs affect its numbers

Profits are a derived numbers as they are derived by using certain assumptions even a small change in assumptions can affect the numbers very widely

Not sure about customer satisfaction with the king of products that the company has been selling because returns in ULIPs are linked to markets

I would have been happier if the company sold more protection policies and sold mutual funds for savings portions(however mutual fund business is no where related to icici prudentail life)

Not sure like how this open architecture where a bank can sell insurance product of any insurance company will affect its business

One way of valuing a life insurance company is to see how many years of Value of New Business (VNB) the price is discounting after deducting Embedded Value from Market Capitalization of the company.

Market Capitalization on 25/Oct/17 = 56,212 crores

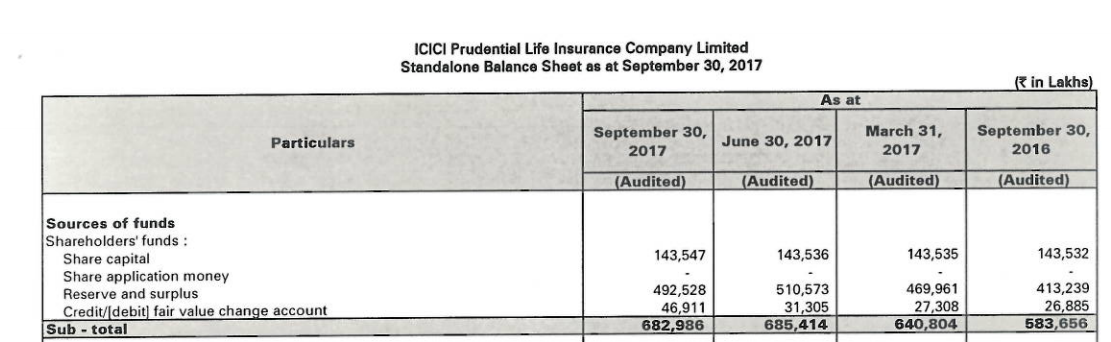

EV (Q2FY18) = 17,200 crores

MCap - EV = 39,012 crores

Value of New Business (VNB) (FY17) = 666

Most surprising aspect of the company is very high growth in VNB, according to q2fy18 report vnb is growing at 70% with is really mind boggling growth.

Assuming a vnb growth of 60% next 10 years

According to this the price is discounting a VNB growth of next eight years. The paper suggest the price should discount next 15 years of growth.

If we agree to this valuation metric and company could deliver 60% VNB growth for next 10 years the stock is massively undervalued.

I am new to insurance sector and I have little clarity on terms used in the valuation of such companies. Can anyone please explain what is Value of New Business?

It is difficult to predict for eight years. 60% is a very high number even for a couple of years. Also ICICI Pru Life is not a small company in small/mid cap space.

Value of New Business (VNB): VNB is used to measure profitability of the new business written in a period. It is present value of all future profits to shareholders measured at the time of writing of the new business contract. Future profits are computed on the basis of long term assumptions which are reviewed annually. Also referred to as NBP (new business profit). [From ICICI Pru Life disclosures].

Please take time to go through a couple of annual reports, DRHPs of insurance companies for better understanding. You may also go through this thread for more information: Life Insurance Companies - Comparison.

They were able to grow the VNB every year and even more than 71% that they managed this time.

Even the VNB Margin is going up steadily from 5.7% to 11.7% now. I feel they are in a sweet spot now. They are growing the VNB and the VNB margin also is increasing. Good thing is they have still more room to expand the VNB Margin. SBI Life has a VNB Margin of 15.4% and HDFC Life does 21.6%.

I’m not an analyst or have a crystal ball. My guess is that they should grow by 30% in the near future coupled with expansion in VNB Margin.

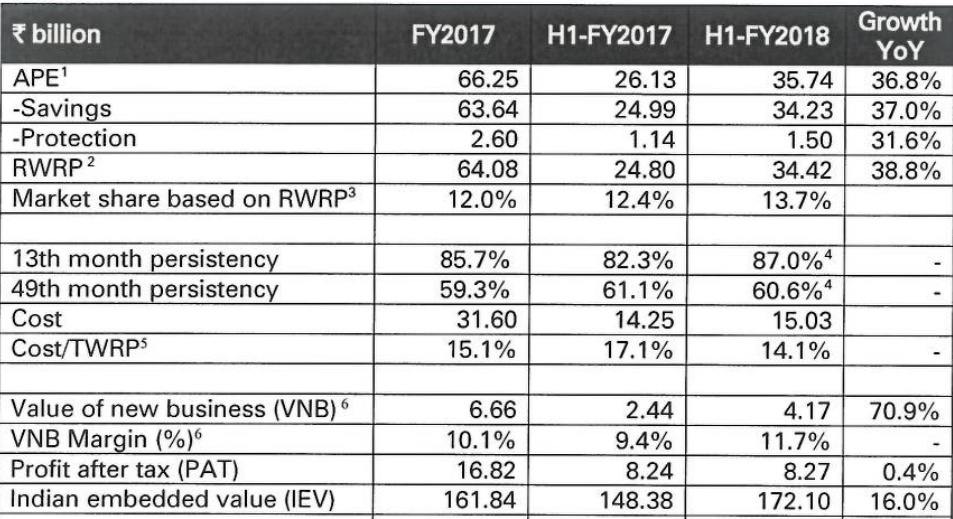

The company has continued to approach the overall market opportunity as two distinct segments-savings and protection. The savings business APE grew by 37% and protection APE grew by 32% leading to the overall APE growth of 36.8% in H1FY2018.

The company has exhibited strong 71% growth in value of new business to Rs 417 crore in H1FY2018. New business margin was 11.7% in H1FY2018, driven by an increase in protection mix and an improvement in the margin of savings products.

The retail weighted received premium or RWRP grew by 39% in H1FY2018, higher than the industry growth of 25% and private industry growth of 37%. Consequently, the market share of the company stood at 13.7% in H1FY2018. The company aims to continue to maintain leadership position amongst the private companies.

The total premium improved 27% to Rs 11484 crore in H1FY2018 from Rs 9029 crore in H1FY2017.

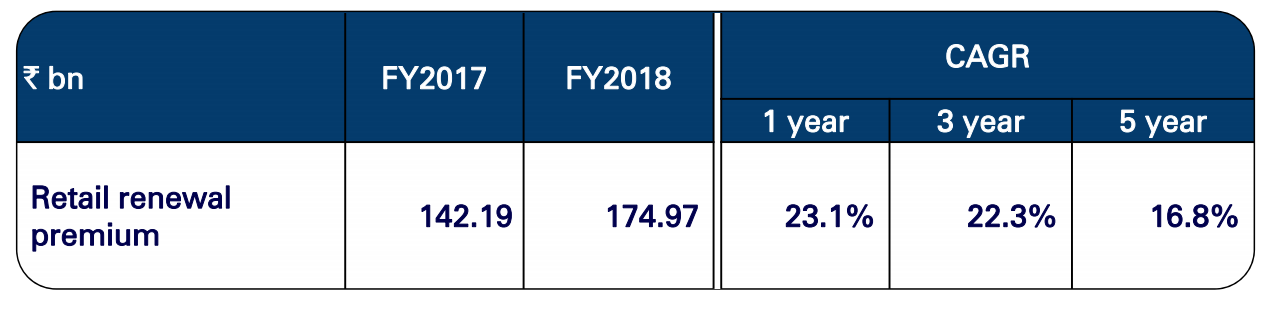

In addition to strong new business growth, retail renewal premium also grew by 23% from Rs 5699 crore for H1FY2017 to Rs 7032 crore for H1FY2018.

The protection mix increased from 3.9% in FY2017 to 4.2% for H1FY2018. Growth in protection business is also reflected in the 30.6% growth in new business sum assured from Rs 1.49 trillion in H1FY2017 to Rs 1.94 trillion in H1FY2018.

The growth of the company is well supported by strong performance across channels. During this period, Agency grew at 59%, Bancassurance grew at 25% and direct business grew at 57%.

The focus of the company on persistency continues with its 13th month persistency of 87.0% is amongst the best in the industry.

Overall cost to TWRP ratio for H1FY2018 is 14.1%.

The company is amongst the largest fund managers in India with an AUM of Rs 1.31 trillion. Linked funds contribute 71% of AUM with equity investments comprising of 58% of linked AUM.

The Embedded Value of the company stood at Rs 17210 crore end September 2017.

The solvency ratio continues to be strong at 275.7%.

The margin for this quarter is 12.6% and margin expansion has happened due to new unit-linked products which have a marginally better margin and even the participating business mix is slightly more. The company expects to sustain this level of margin.

The company intends to grow the protection business at a much higher rate over a longer period.

The company expects to maintain stable expense ratio.

This is hardly mis-selling, this is cold blooded cheating with criminal intent to dupe gullible public of their money to meet internal target in institutions (in)famous for their “aggressive” culture. What are the poor victims supposed to do if they are unable to get their monthly payouts to meet living expenses? I hope the guilty are awarded exemplary punitive sentences to deter such wrong doings from other officers in future. Sorry for the rant, but such criminal acts really gets me riled.

Operating metrics:

(1) 9mFY18 APE growth was 25% with protection APE growth at 32% YoY (good business growth across business lines). Management expects growth

in protection business to sustain;

(2) NBAP margins reported for 9mFY18 @ 13.7% were largely a reflection of product mix & cost structures; incremental levers for margin improvement are: a) protection growing faster than savings will feed into higher margin; b) persistency 13th month is at 86% while in assumptions it is 82%, so as it comes for review it will boost margin; and c) also, long-term persistency itself is expected to structurally improve;

(3) solvency trajectory has three elements playing out: a) dividend payout at 60%; b) savings business is gaining traction & consuming capital; c) growth in protection business - capital for whole sum assured & since premium is low, capital for same amount of premium is high;

(4) most of the protection business comes from retail - credit linked was merely INR0.38bn, of INR2bn of protection business.

Overall business:

Key objectives:

a) Customer-centric products (ULIP+ protection contributes 87.0% to total APE); and

b) focus on retail through multi-channel distribution architecture backed by strong technology platform.

Wider direct market operates in two segments - web aggregator (fee based model - no spend on advertising) and company website (needs to do advertisements to direct traffic). 50-60% business through web aggregators. For ICICI Prudential Life, one more element in direct business is own direct employee selling insurance. Any cost efficiency resulting due to direct sourcing will be passed on as a benefit to the customer.

Other highlights:

(1) Since headline rate for insurance companies at 12.5% is lower than prevailing corporate tax rate, the risk of increase in tax rate prevails. However, how much it will be raised will depend on several factors;

(2) in the short term, insurance products are more expensive than MFs, but in the long term they are at par or better than mutual funds;

(3) 55-60% of assets get allocated to equity in ULIP & balance to debt funds. Insurance products help customers switch over across asset class without tax implications.

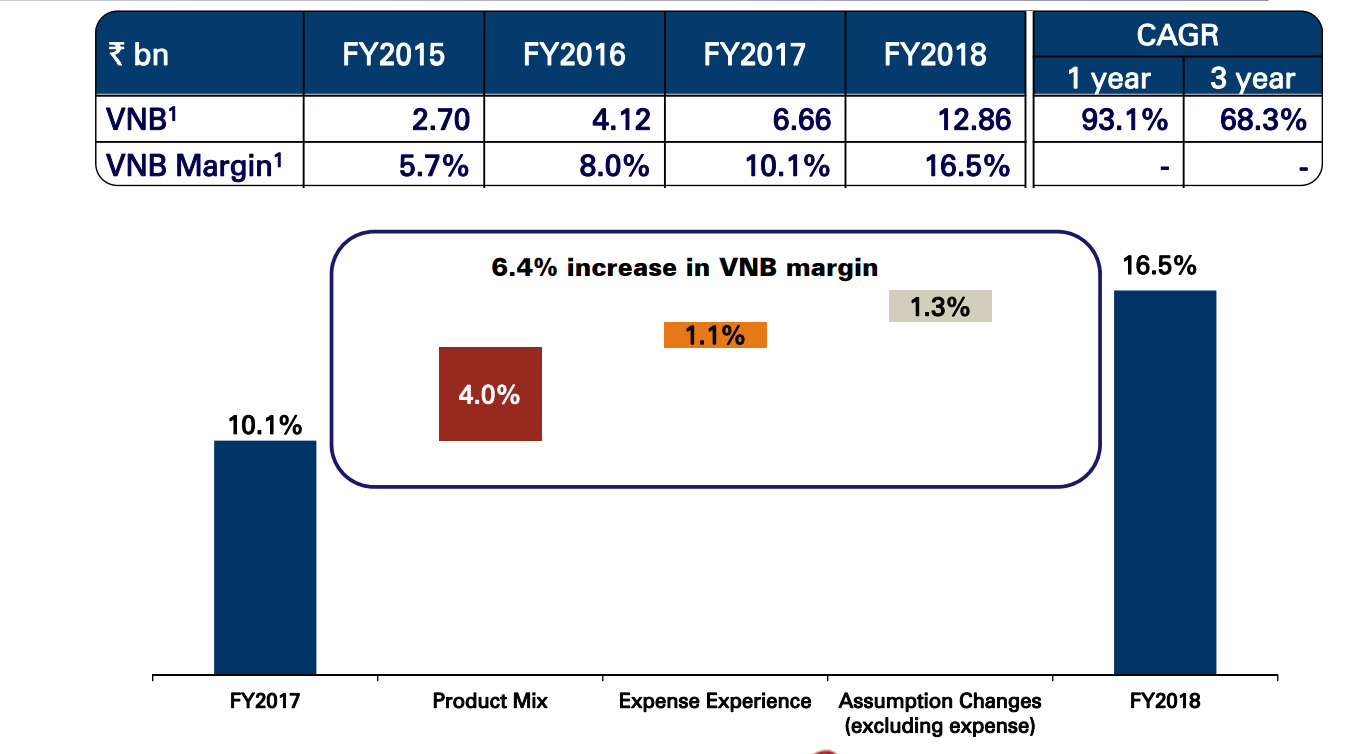

VNB & VNB Margin: VNB grew from 6.66bn (FY17) to 12.86bn (FY17) resulting in growth of 93%. The VNB margin increased by phenomenal 640bps from 10.1% to 16.5%.

Embedded Value: IEV increased from 161.84bn to 187.88bn despite healthy dividend of 11.88bn. EVOP of 36.8bn & RoEV of 22.7% are very healthy. The company said that dividend will go down in FY19 as they need to preserve capital to support growth in non-ULIP business. My feeling is healthy dividend is probably paid to help in troubles of parent group.

Protection APE: The protection business grew by phenomenal 71% i.e. 2.6bn in FY17 to 4.46bn in FY18. This has lead to growth in VNB & VNB margin. The growth in credit cover business was higher than individual life businesses. For the first time, I noticed credit protect products - Loan Protect, Loan Protect Plus, Group Loan Secure. This business has been such a driving force for HDFC life. With more players trying to get into credit protect segment, it would be interesting to track how this space evolves.

Retail Franchise: ICICI Pru has a very retail focused franchise where 98% of APE is from retail. Retail franchise has better margins than group business (high proportion for HDFC Life).

Cost Efficiency: ICICI Pru has reduced cost/TWRP from 15.1% to 13.7% i.e. reduction of 1.4%. As non-ULIP portfolio grows, it would be interesting to see how this number evolves. The cost has gone up for HDFC Life.

Renewal Premium: Renewal premium has grown at 23% for FY18 compared to 11% for HDFC Life. This might be on account of lower share of group business or more retail focused franchise.

Tax rate assumption: The company has used lower effective tax rate similar to what some of the industry players have been doing. This has added ~ 1.4bn in EV & ~1.3% in VNB margin.

Valuation: I still struggle to put a valuation number to life insurance companies. After going through several research reports for Indian & overseas insurance companies, appraisal value (AV) seems like one decent metric. AV = EV + multiple * VNB. Many reports seem to have used multiple ranging from 10-30. One can use his own multiple & come up with AV.

Disc - Forms more than 5% of portfolio. No transactions for last 90 days.