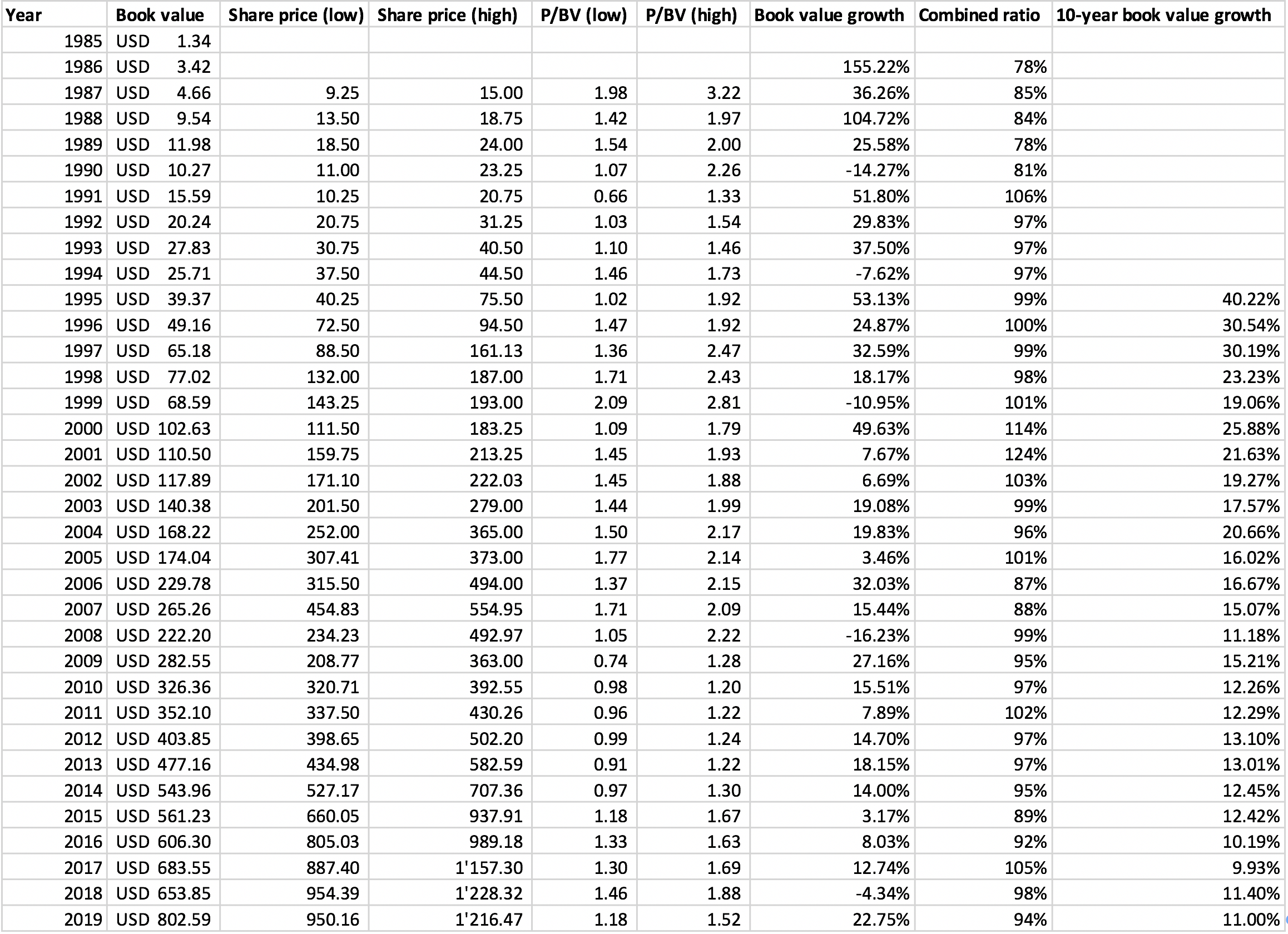

Honestly, I do not understand the current valuations of Indian insurance companies. Globally, insurance companies are valued relative to their books. I have shared the detailed valuations of Markel Corp (global leader in specialty insurance) with a track record of 34 years (book value growth ~ 20%).

During the initial part of their life cycle (similar to the stage of ICICI Lombard), they were growing their book value at 20-25% maintaining a profitable combined ratio in most years. During their rapid growth years, the maximum valuations they quoted at was 2.5-3 times book. As recent growth has tapered down to 10-12% they now quote at 1-2 times their book value. All this when their underwriting business is hugely profitable.

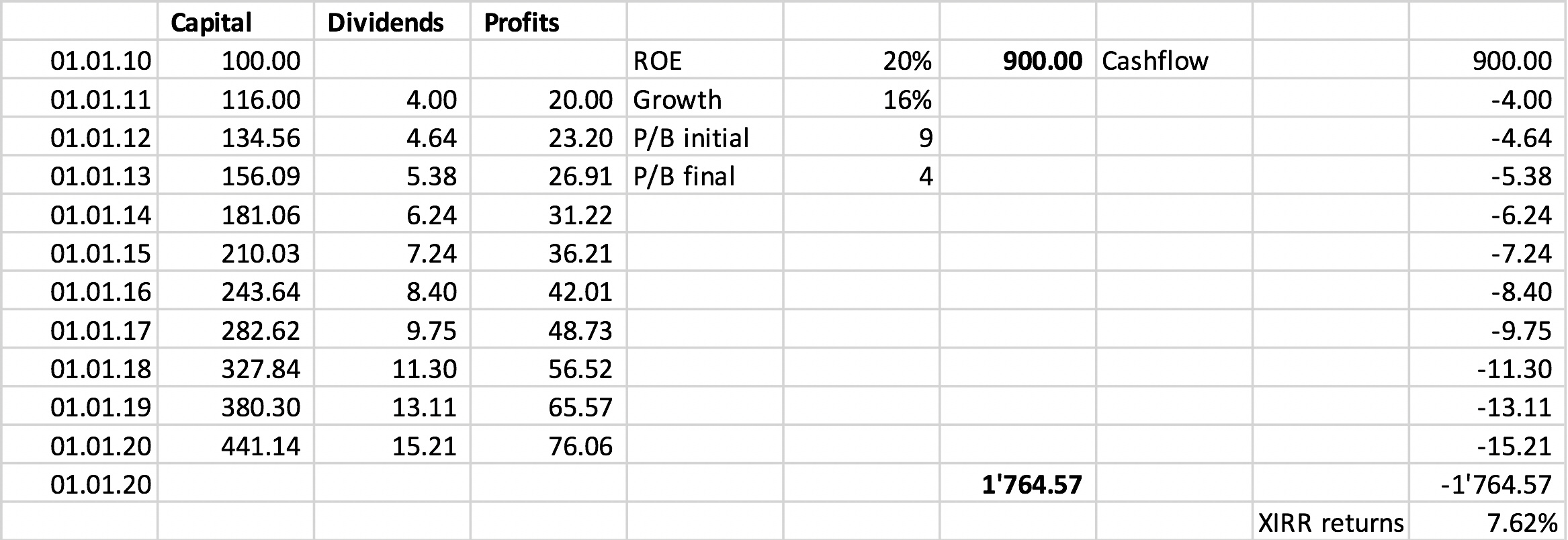

Now lets assume ICICI lombard is able to maintain its ROE of 20% over the next decade, gives 20% dividend and reinvests 80% of its profits back into the business. The current valuations are ~9 times book. Lets say an investor gets in now and is able to exit at ~4 times book (which is not at all conservative), returns will be ~7.62%. @Surender - You are right in your valuations.