Things seem to be getting interesting here - one of the lowest cost producers (IG Petro) in a cyclical industry has now posted a loss at the EBITDA level. A further reduction in spreads would lead to shut-down of capacities in Taiwan, Korea & China.

Gross/EBITDA margins are at their lowest in recent history - main reason being…

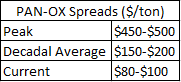

Phthalic Anhydride-Orthoxylene (PAN-OX) spreads have almost come down to the company’s conversion cost of ~$85/ton. Further, Maleic Anhydride prices (where company earns an EBITDA margin of ~95%) are 10%-15% lower than PAN prices (compared to 10%-15% higher historically).

While domestic demand for PAN continues to grow (accounts for ~90% of the company’s revenue), geopolitical issues have temporarily impacted the key end-user industries (Pigments, Paints, Plasticizer, Specialty Chemicals). Rising Orthoxylene prices (key raw material - a derivative of crude oil), excess supply of Maleic Anhydride (MAN) are further reasons.

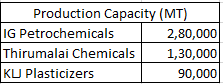

Virtual duopoly in the domestic market (IG Petro & Thirumalai), while KLJ has now backward integrated (used to import earlier). IG Petro is the second largest PAN manufacturer globally. This is predominantly a regional business and setting up a new plant takes 3-4 years (availability of raw material is a constraint).

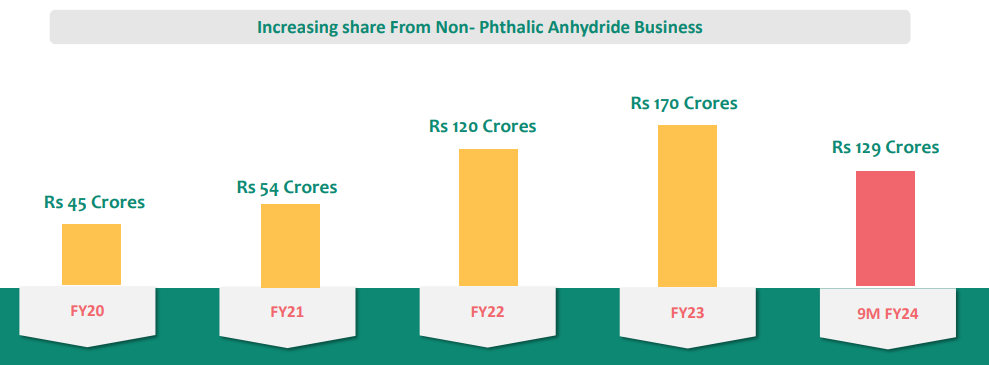

Company has also forward integrated into Diethyl Phthalate (DEP) where EBITDA margins are relatively stable (in the range of 10%-15%).

The share of Non-PAN business in the company’s revenue has been steadily increasing.

Meanwhile the company’s new plant has just commenced production and is expected to add ~Rs. 500 crores to the topline. Another Rs. 200 crore capacity expansion in DEP is being planned, with potential for Rs.800 crores in revenue. Demand for DEP is growing at 10%-15% annually.

Both IG Petro and Thirumalai have increased capacity. They expect the capacities to be absorbed given the strong domestic demand and growing use of PAN. China has built up 2 MT of MAN capacity for use in downstream capacities which are coming up (expected - Jan 2025). In the interim, this excess supply is leading to depressed prices. Overall things should only get better from here?

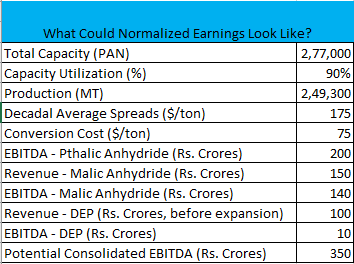

While the pain may last for a while, can the company do an EBITDA of ~Rs. 350 crores once the situation normalizes? If we assume this, company’s Profit After Tax should be around Rs. 200 crores (Other Income offsetting interest expense and depreciation of around Rs. 70 crores).

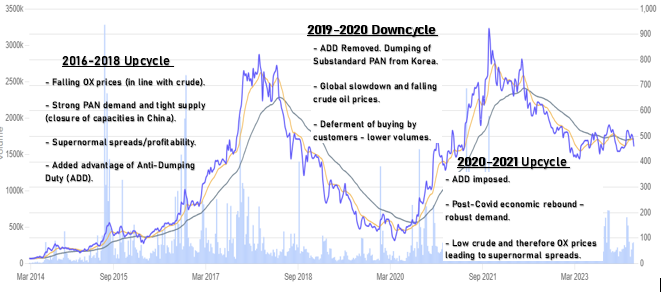

Brief Context on Past Cycles

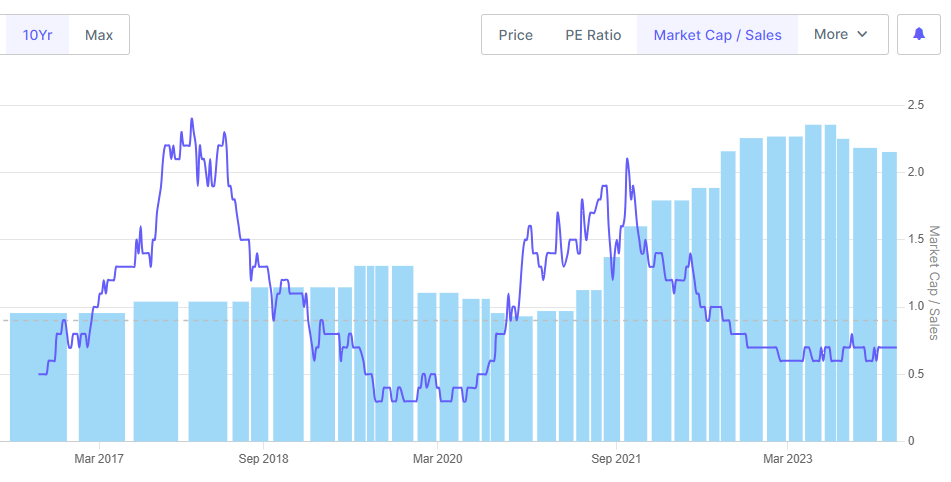

The tricky part seems to be - how does all this translate in terms of valuations/potential entry point? If this doesn’t work out, what could be the potential downside? And if it does, is the upside large enough to compensate for the waiting period and all the volatility?

A few open-ended questions in this context:

-

Price/Sales could be one way to look at it. However, with volatile sales, both due to fluctuating PAN prices as well as increase in volume from new plants, this on it’s own doesn’t provide the full picture?

-

Given that IG Petro is one of the lowest cost producers of this commodity with a net debt free balance sheet, a reasonable P/E or EV/EBITDA on normalized earnings could be assigned. What could be a reasonable multiple in such a case?

-

Decrease in institutional holding (FII+DII) or insider buying could be another important indicator?

Would love to get any thoughts.