Brief Introduction

I G Petrochemicals Ltd. (IGPL) promoted by Dhanuka Group is an established market leader in Phthalic Anhydride (PAN) started its production in 1992.Currently, total current capacity stands at 1,69,250 MTA

Orthoxylene (OX),3rd derivative of crude is the single raw material required for manufacturing of PAN.

The plant is located at MIDC, Taloja in Raigad District, Maharashtra, India, 50 Km from Jawaharlal Nehru Port Trust (JNPT), Nhavasheva, Maharashtra ,giving the company triple advantage 1)in the vicinity of chemical belt in western india (70% of domestic sales) where majority end user are located 2)close to Gujarat from where 70% of raw material is sourced 3) close proximity to ports & 90% of export of PAN happens at this port only.

Can check export data with this link https://www.zauba.com/exportanalysis-phthalic+anhydride-report.html

IGPL operates it’s plant based on the processes of the licensor M/s Wacker Chemie GmbH, Germany. The process is Wacker’s Von-Heyden’s Low Energy Process and the plant has been engineered by M/s Lurgi GmbH , Germany

The Company has been named in the Fortune India Next 500 in July 2015 edition, a comprehensive monthly magazine covering the ranking of India’s Mid Sized companies. The Company is ranked at 168

Usage of PAN

Phthalic Anhydride (PAN) is used in manufacturing plasticizers, which are most essential in making PVC products, shoe soles, cables, pipes and hoses, leather cloth, films for packaging and other products.

PAN is 2nd most imp product used in manufacture of paints and coating as an intermediate of alkyd resins

PAN is also used in the production of unsaturated polyester resins used in making fibre glass reinforced plastic used for building materials,marine & transport industry.

It has application in CPC used in printing inks,Photovoltaic cells.

Customers

• Big paint companies like Kansai Nerolac,Berger,Akzo Nobel.

• Plasticizer company KLJ Plasticizer (Largest Manufacturer of Plasticizer in SE Asia),PCL Oil & Plasticizer

• MNC chemical co like Scott Bader,Ashland,Sabic

• Domestic Chemical Co like Aarti industries

• AOC Resin (Global supplier of Polyester resin)

Competitive Advantage

- Lowest cost producer of PAN globally mainly due to

• Self sufficient in-house generation of power

• Higher recovery and reengineering process - Maintained consistent highest capacity utilisation 90% for last 5 yrs despite capex which shows huge consumption pull for PAN.

- Diversified product use in multiple industries resulting in low dependency on any particular customer.

- Great locational advantage near to port resulting in huge logistic cost saving, better inventory management & lesser lead time.

- Better recovery process as steam generated from process are utilised resulting in lesser fuel cost.

- Only 4 other domestic manufacturer but only Thirumalai Chemical being major competitor

Thirumalai Chem(1,45,000 MTA) 2nd largest manufacturer

Asian Paints uses mainly for captive consumption

Mysore Petrochem closed operation at Raichur, Karnataka, belongs to Dhanuka group of I G Petro

S I Group mainly for captive consumption

Positives

- Started paying Div Re.1 in FY 15 after completing major capex.

- Promoter holding good 72.22% stake without any shares pledged.

Increased stake from 71.88% in Dec 13 to 72.22% purchasing shares from open mkt - Debts are reducing significantly

Financial Yr Debt(in Cr)

FY 14 185 Cr

FY15 131 Cr

H1 FY16 116 Cr

4 Anil Goel, very known investor is increasing stake from 1.54% (4.75 lacs) in June 15 to 1.79 %(5.5lacs) in Sept 15.

He is holding 1 lac shares (.32%) in his wife name Seema Goel. So in toal holding more than 2 % or 6.5 lacs share.

5. KLJ Plasticizer, one of its major customer & Largest Manufacturer of Plasticizer in SE Asia holding 2.7 lacs share.It seems they are also confident about IGPL future

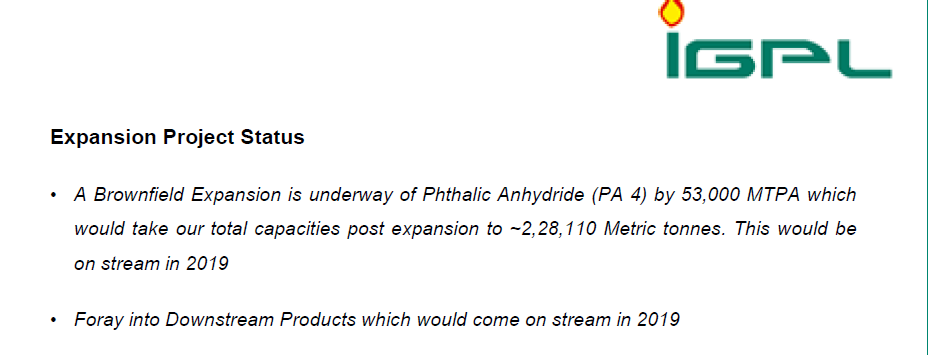

6. IGPL’s wholly owned subsidiary IGPL (FZE) entered into a Joint Venture (JV) with M/s. Dubai Natural Gas Co. Ltd., UAE (“DUGAS”) for the manufacturing of Maleic Anhydride with a capacity of 45,000 MTPA. DUGAS is a wholly owned subsidiary of the Emirates National Oil Company (ENOC) and are a well diversified large conglomerate with interest in the oil and gas industry. This JV augurs well as Middle East is currently relying on import of MA.

7. Upgrade in the Credit Rating for Long Term & Short Term Borrowings by India Ratings & Research

Particulars Old Rating New Rating

Long Term Borrowings IND BBB+ IND A-

Short Term Borrowings IND A2+ IND A1

8 Absolving of contingent Liabilities related to Excise & Custom duty of Rs 204 Cr as DTA Sales & Catalyst Case decided in IGPL’s favour in Fy 15.

9. Low Crude prices are going to benefit PA manufacturer in longer run as their raw material is crude derivative Ox.

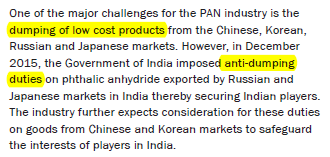

10. Anti Dumping duty on imports of PA from Russia(largest exporter of PA to India) & Japan of 106-159$ per MT from 04 Dec 2015

11. Opposing parties Japan & Russia only targeted IGPL in their case saying IGPL sales, capacity utilisation, Gross Profit, capacity have improved & other players are non performing because of competitive disadvantage with IGPL

Must Read page 41-42 of Notification in AntiDumping case (http://commerce.gov.in/writereaddata/traderemedies/adfin_Phthalic_Anhydride_Russia_Japan.pdf)

12. Indian PA industry demand expected to grow at 7-8% annually & india being 3rd largest consumer of Plasticizer will continue with PA demand.

13. Return on Capital Employed ROCE improved significantly to 25.5% in H1 FY16

Financial Yr ROCE(%)

FY 13 4.8

FY 14 8.6

FY 15 20.2

H1 Fy 16 25.5

Negatives

- Due to abrupt fall in Crude Price inventory loss can be a Partypooper

- Drastic drop in crude prices causes buyers to keep minimum inventory.

Financials

CMP-100 MCap- 307 Cr

BV-91 Expected FY 16 EPS- 28

FY16 P/E- 3.5 Debt/Equity= 0.4

Revenue- apprx 1100 Cr Sales/MCap-0.28

Conclusion

EBIDTA for H1 FY 16 stands at 73 Cr against H1 FY 15 of 43 Cr,a healthy 71% increase on account of greater operating Margin aided by falling Crude.

PAT for H1 FY 16 stands at 15 Cr against H1 FY 15 of 42 Cr, 185% increase with debts coming down & capacity utilisation of more than 90% it is expected to improve further

Debts have come down drastically & at comfortable position which augurs well for future of the company.

With new JV of 45000MT for Maleic Anhydride with ENOC it is a great opportunity for future growth in this new product whose most customers are similar & ENOC being Oil producer raw material availability will be also helpful. Middle East being importer of MA so this JV seems to be rightly placed.

Sales can come down drastically because of fall in crude prices but OPM & NPM will definitely increase because of fall in raw material prices & Sales.

At CMP of Rs 100 IGPL trading at just P/E of 3.5 & Sales/MCap of 0.28,Debt reducing I feel its available very cheap.

Disc:- Invested

Looking forward for your queries