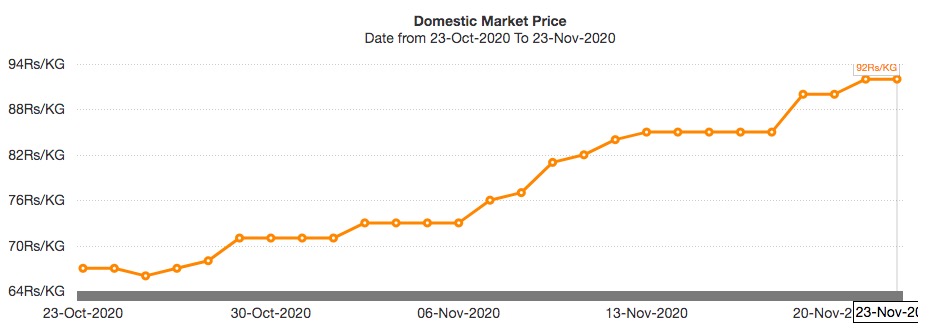

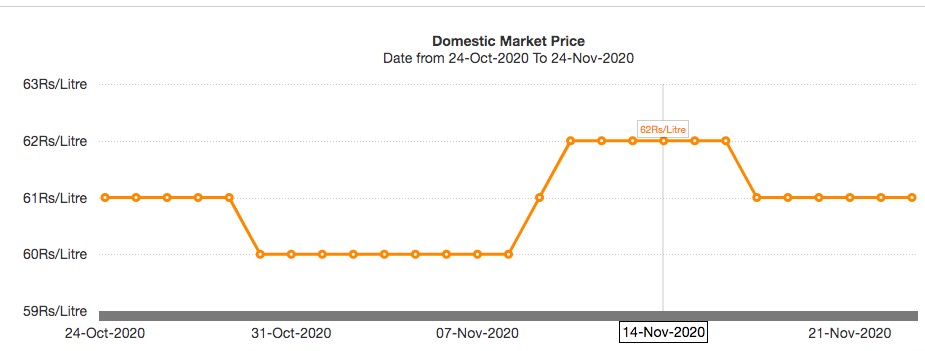

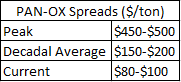

Current PAN & OX prices attached below. Spreads seem to be very high because PAN prices are increasing whereas RM(OX) prices are flat

2 Likes

Thanks for you data.

This stock can do very well

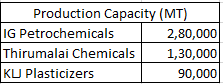

Being duopoly in India along with Thirumalai

can you pls post the latest chart of PAN & OX spread?

Any one tracking IG Petrochem. Today there was a 20% jump in prices.

2 Likes

In August 2021, the government of India imposed anti-dumping duty in August on the PAN.

Rating of company upgraded by Ind-Ra in Oct 21

Current price is 685. Looks attractive.

Note : Invested at 635

1 Like

Anyone tracking this company? Looks like margins have gone down after the company ventured into new products.

1 Like

IGPL has good CAGR but it was because of fall in oil price which led to increase in margin ,Its largest and lowest cost producer of PAN in India & and only MAN manufacturer in India .

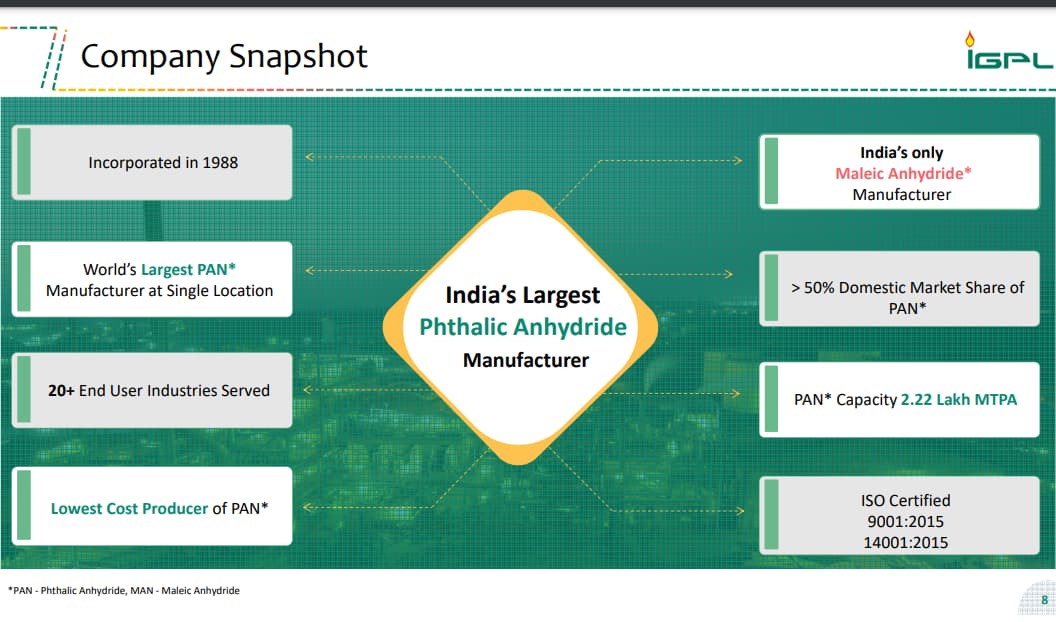

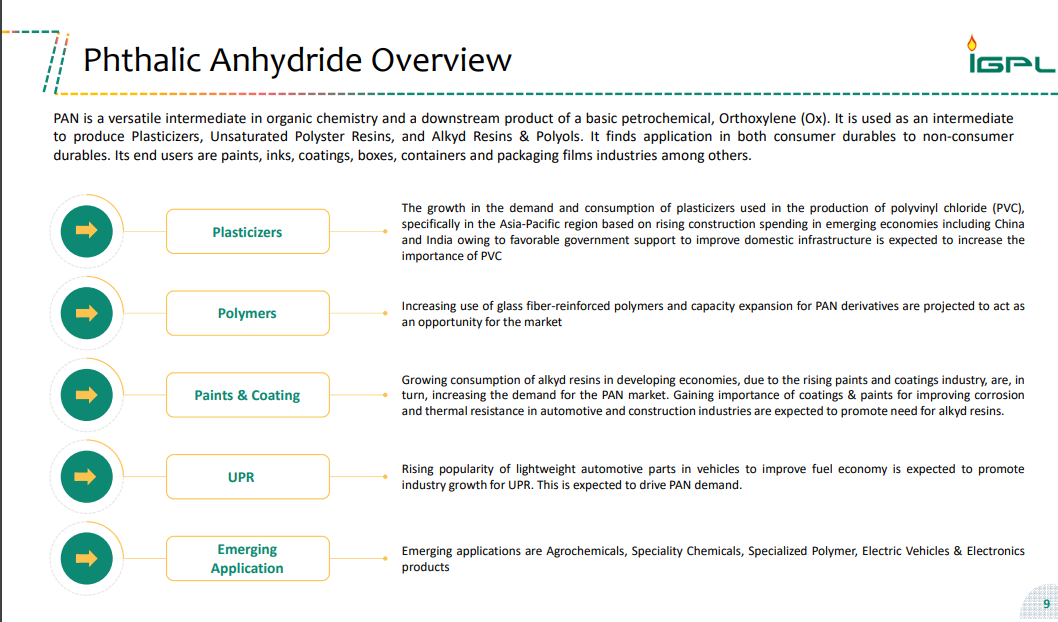

Here are pictures of slides in the ppt

the company also makes full use of byproducts made while manufacturing PAN by making benzoic acid & MAN of it

the company is also planning to CAPEX

the only thing left keeping company behind is margins

1 Like

Things seem to be getting interesting here - one of the lowest cost producers (IG Petro) in a cyclical industry has now posted a loss at the EBITDA level. A further reduction in spreads would lead to shut-down of capacities in Taiwan, Korea & China.

Gross/EBITDA margins are at their lowest in recent history - main reason being…

Phthalic Anhydride-Orthoxylene (PAN-OX) spreads have almost come down to the company’s conversion cost of ~$85/ton. Further, Maleic Anhydride prices (where company earns an EBITDA margin of ~95%) are 10%-15% lower than PAN prices (compared to 10%-15% higher historically).

While domestic demand for PAN continues to grow (accounts for ~90% of the company’s revenue), geopolitical issues have temporarily impacted the key end-user industries (Pigments, Paints, Plasticizer, Specialty Chemicals). Rising Orthoxylene prices (key raw material - a derivative of crude oil), excess supply of Maleic Anhydride (MAN) are further reasons.

Virtual duopoly in the domestic market (IG Petro & Thirumalai), while KLJ has now backward integrated (used to import earlier). IG Petro is the second largest PAN manufacturer globally. This is predominantly a regional business and setting up a new plant takes 3-4 years (availability of raw material is a constraint).

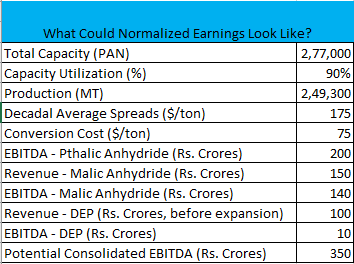

Company has also forward integrated into Diethyl Phthalate (DEP) where EBITDA margins are relatively stable (in the range of 10%-15%).

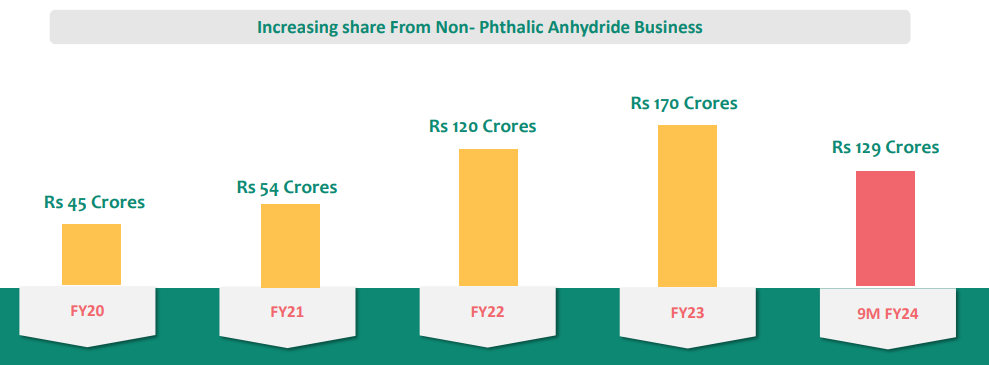

The share of Non-PAN business in the company’s revenue has been steadily increasing.

Meanwhile the company’s new plant has just commenced production and is expected to add ~Rs. 500 crores to the topline. Another Rs. 200 crore capacity expansion in DEP is being planned, with potential for Rs.800 crores in revenue. Demand for DEP is growing at 10%-15% annually.

Both IG Petro and Thirumalai have increased capacity. They expect the capacities to be absorbed given the strong domestic demand and growing use of PAN. China has built up 2 MT of MAN capacity for use in downstream capacities which are coming up (expected - Jan 2025). In the interim, this excess supply is leading to depressed prices. Overall things should only get better from here?

While the pain may last for a while, can the company do an EBITDA of ~Rs. 350 crores once the situation normalizes? If we assume this, company’s Profit After Tax should be around Rs. 200 crores (Other Income offsetting interest expense and depreciation of around Rs. 70 crores).

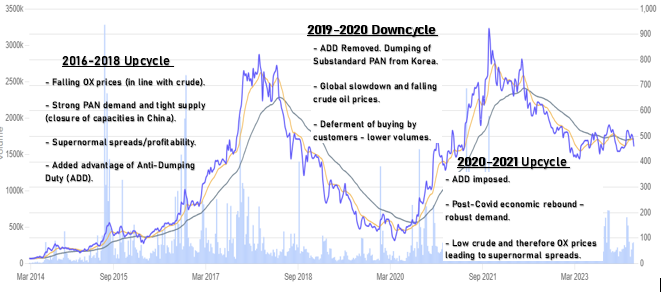

Brief Context on Past Cycles

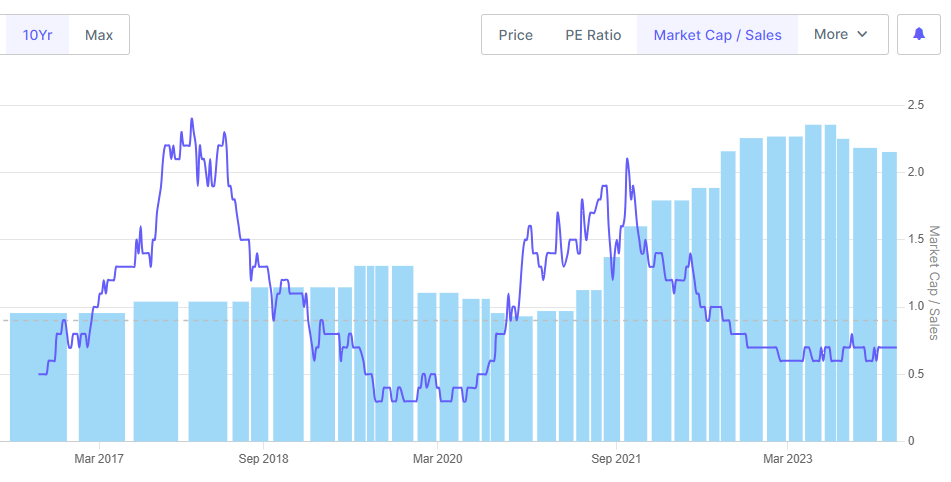

The tricky part seems to be - how does all this translate in terms of valuations/potential entry point? If this doesn’t work out, what could be the potential downside? And if it does, is the upside large enough to compensate for the waiting period and all the volatility?

A few open-ended questions in this context:

-

Price/Sales could be one way to look at it. However, with volatile sales, both due to fluctuating PAN prices as well as increase in volume from new plants, this on it’s own doesn’t provide the full picture?

-

Given that IG Petro is one of the lowest cost producers of this commodity with a net debt free balance sheet, a reasonable P/E or EV/EBITDA on normalized earnings could be assigned. What could be a reasonable multiple in such a case?

-

Decrease in institutional holding (FII+DII) or insider buying could be another important indicator?

Would love to get any thoughts.

17 Likes

I do not understand the cyclical part of it. Nor will I comment on the valuation bit. However, what I do know is that the company is very well managed! I’ve been supplying cables to them for the last decade or so.

7 Likes

Thanks to some valuable feedback, learnt that there is a significant second round of capacity additions taking place - both KLJ and Thirumalai are adding about 1 lakh MT each over and above the current domestic capacity of ~5 lakh MT. This ICRA report mentions that it will take a few years for domestic demand (~5 lakh MT and growing at ~8%) to be able to absorb the new capacity.

For years these companies didn’t expand capacity when there was a shortage, so wonder what is prompting the current expansion spree. Will keep this on radar but for now there seem to be better opportunities if the market corrects.

So just trying summarize the the current developments.

IG happens to the largest player in the industry (275l Mt pa) close to 50% of total domestic capacity. One of their key customers has actually backward integrated into PAN production for DEP. Meanwhile imports have sharply fallen by more than 50%. It is simply not possible to compete with cost of production of IG and all (economies of scale and cheapest producer). A substantial quantum of PAN is consumed by the paints sector which should sustain, but there is nothing which can change exponentially either on demand/supply side (as far as I understand) however, Indian players are benefitted by imposition of ADDs, some of which shall expire by CY26 I think, unless this factor opens up something.

Asset Turns are around 1-1.2x overall, erratic PAT/OPM keep the RoE/RoCE readings very volatile as well as PAN-Ox spread is the key to track which is directly related to crude and global demand function. So factors which are within control of IG happens to be lesser.

Maybe why in FY18 when RoCE was 35%+ P/BV was 3.5, but currently oscillating between 1-1.25x. Uncertainty maybe is the reason.

Probably why they’re now diversifying into downstream plasticizers (PVC led consumption) which is more stable margins and much higher Asset turns of 5x (mgmt guidance). Full scale productions to happen by FY26 end and should be interesting.

LT Borrowings have gone up, interest cost jumped up as well, which shall add another volatile reading to track: Int coverage ratio.

All said, may not be very comfortable for many right now, but key to watch how the industry dynamics change post the ADDs expire, and if the plasticizers make the business more stable. Both factors shall play out around the same time between CY26-27.

3 Likes

Bad results… i think this will be the steady state profits per quarter… valuations are quite high.

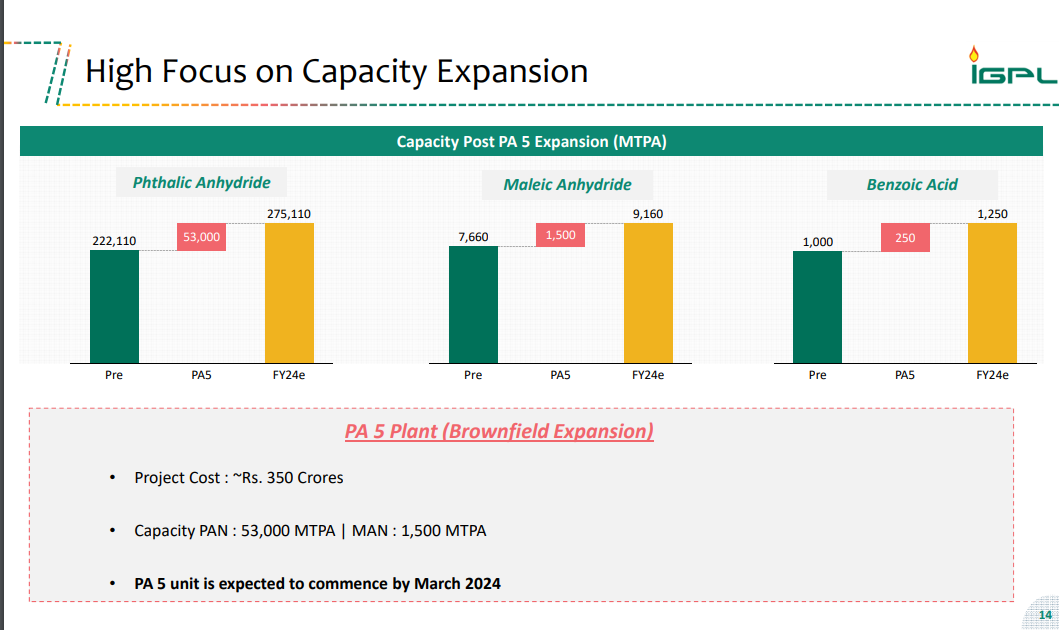

a) Company Profile: The company commenced production in 1992. It manufactures Phthalic Anhydride (PAN), which is essential for manufacturing polyvinyl chloride products, shoe soles, cables, pipes, hoses, leather cloth and packaging films along with maleic anhydride (MA) and benzoic acid (BA). The company has a total installed capacity of 2,75,110 MTPA.

B) Investment Rationale: The following is the investment rationale for the company:

-

Largest PAN manufacturer: The company is India’s largest PAN manufacturer accounting for over 50% of the domestic production and the world’s second largest PAN producer. The company also produces maleic anhydride (MA) and benzoic acid (BA) through the wash water generated from PAN manufacturing. The extraction of MA and BA enables the company to generate incremental operational cash flows that improve its profitability at no additional cost. Moreover, IGPL is the only producer of MA in India with an existing annual capacity of 8,000-8,500mtpa and meets around 40% of the domestic demand as per management, while its BA capacity stands at 1,200mtpa.

-

Recently completed expansion: The company has recently completed its capacity expansion where it increased its PAN capacity by 53,000 MTPA at the end of Q4 FY24, leading to a total capacity of 2,75,110 MTPA. The company has its manufacturing facility in Taloja (Navi Mumbai) which is beneficial due to its proximity to the end-user industry as 70% of the PAN produced is consumed in western India. The company also benefits from low procurement costs due to its proximity to feedstock supplier Reliance Industries Limited and easy access to JNPT and Mumbai ports.

-

Government’s Anti-dumping duty: In August 2021, the government of India imposed an anti-dumping duty for a 5-year period on PAN imported from China, Indonesia, Korea, and Thailand. This duty ranges from USD 40-140/MT depending upon the producer and country of export. The domestic market catered to 10-15% of its demand through imports in FY24, which was lower than the 30% levels witnessed in FY19-20. Although the profitability is largely driven by PAN-OX spreads in the international markets, the duty imposition has increased the competitiveness of the domestic manufacturers.

-

Q1 FY25 results: The company’s Q1 FY25 revenue from operations grew 5.7% YoY, whereas EBITDA for the quarter stood at Rs 71 crores, a growth of 7.3%. The EBITDA margin stood at 12% versus 11.8% YoY. FY24 saw a sales decline of 11% due to a fall in volumes and realizations. However, with the commencement of the PA5, Ind-Ra expects the revenues to grow in higher double digits in the medium term. The company’s EBITDA margins declined to 5% in FY24 due to weaker PAN-OX spreads but is expected to stabilize going forward.

-

Modest working capital requirements: As of FY24 end, the company had cash and cash equivalents of Rs 233 crores. The company’s cashflow from operations were positive over FY15-24. Also, the company has moderate working capital requirements due to a comfortable credit period on purchases. The company makes local purchases primarily from Reliance Industries on a credit basis, with small quantities being imported.

C) Future outlook: The following is the future outlook provided by the management:

-

Signs of recovery: According to the management, the demand for end user industry has started showing signs of revival and chemical prices have started seeing a modest recovery. Currently, the demand for PAN is in the range of 5,00,000-5,50,000 MTPA and is expected to grow 5-6% annually. The margin between PAN-OX spread on a QoQ basis is ranging between $150-200, which indicates a price recovery of $50-100/ton sequentially. Also, in terms of volumes, the management has guided that Q2 FY25 will be 10-15% better than Q1 FY25 in terms of volumes sold, and Q3 FY25 volumes would be 10% better than Q2 FY25. It has guided for full year volumes of 2,10,000 tons versus 2,05,000 tons for FY24.

-

Contribution of the PA5 plant: Post the recent addition of the PA5 unit, the company’s capacity has been enhanced to 2,75,000 MTPA. Currently, its facilities are operating at 80-85% utilization with two plants undergoing maintenance shutdown due to which the company lost 10-15,000 of volumes on a quarterly basis. However, the PA5 unit is on its way to clock annual revenues of Rs 650 crores versus Rs 500 crores guided by the management. Due to this new plant, the company will have an operating cost saving of $20-$25. The utilization of this plant was 50-60% in Q1 FY25.

-

Upcoming capacity expansion: The company is setting up a 75,000 MTPA plasticizers capacity at a total project cost of Rs 186 crores which will be completed by Q3 FY26 end. Around 70% of the project would be funded through debt and the rest will be funded through internal accruals. The expansion shall help IGPL to diversify its product profile to capture the growing domestic demand in the downstream industries, while also leveraging its existing customer profile which the management expects to account for 70% of the turnover once the capacity ramps up. The plasticizer capacity will captively use 30,000-35,000 tons of PAN as a raw material post the set up. As per management, on the full capacity utilization, the plasticizer capacity is expected to contribute INR9,000 million-9,500 million in revenue for the full year. The company plans to move towards green energy also through setting up a compressed biogas plant at capex of around INR320 million. The plant is expected to be operational by end-FY26. It will be a fully automated plant and is expected to supply oil marketing companies. Ind-Ra believes increased product diversification would partially help reduce the volatility in profits.

-

Unsaturated Polymer Resin (UPR): Today, 95% of the Indian market uses PVC, CPVC, and UPVC pipes, which have a lifespan of 15-20 years. However, in interstate or big infrastructure projects like agriculture or water pipeline, UPR based pipes are better because they have a shelf life of 80-100 years, and they are corrosion free. Governments in Europe and America prefer UPR pipes but the same has started off late in India since the last 3-4 years. Companies like Tata Steel, which earns about Rs 2 lakh crore in revenues has recently crossed Rs 100 crore in sales from UPR pipes. Also, globally, UPR consumes 25% of phthalic. In India, it is still 5%.

-

Guidance for the future: For FY25 and FY26, the total capex would be Rs 200 crores, for which debt: equity ratio would be 50:50. The company guides for a long-term average EBITDA margin of 15% as it is based on PAN-OX spreads. With respect to revenues, the company aims to clock between Rs 2,300-2,500 crores in FY25. For FY25, the company is specifically guiding for 12-15% EBITDA margins.

D) Key monitorables: The following are the key monitorables for the company:

-

Debt levels: The company’s net debt/EBITDA increased to 3.65x in FY24 versus 0.71x in FY23 due to debt-laden expansion. Also, the interest coverage ratio declined to 3.5x in FY24 versus 13.3x in FY23 due to lower EBITDA levels. Although the PAN-OX spreads are expected to improve going forward, debt levels remain a key monitorable.

-

Raw material price risk: The company’s key raw material OX is a crude oil derivative and thus its price is mainly driven by crude prices. Therefore, high volatility in crude prices and PAN-OX spreads will continue to significantly impact IGPL’s EBITDA margins.

-

Product concentration risk: PAN contributed 93% to the company’s revenues in FY24, which poses a huge product concentration risk arising from a change in government regulations. However, the management intends to diversify its product portfolio by getting into other downstream derivatives and other specialty chemicals, and endeavors to have 30% of its revenue from non-phthalic products over the medium term.

-

Subdued MA prices: As per the decadal average, maleic acid has always traded at 20% premium to phthalic acid. But currently it is trading at a 10-12% discount.

-

Increasing freight rates: Freight rates have gone up by 15-20%. However, the company has the flexibility to charge the consumer any incremental rates. Also, exports is only 5-7% of the company’s sales.

-

Uncertainty regarding ADD: The management can’t comment on the government’s stance on ADD. But, as per them, it would not make a major difference as everyone sells at the international prices.

The stock trades at a TTM PE of 51x.

3 Likes

The company’s profit growth has been inconsistent. The operating profit margin (OPM) fluctuates widely, ranging from 5% to 22%.

1 Like

IGPL is pure play commodity player with domestic market leadership and cost efficiencies. However, Imports pose a significant risk to the company’s revenue and profitability.

Instances where imports have affected the revenue and margins of (IGPL):

2018-19: There are many global players that dump their products in India. To counter this, the government imposed anti-dumping duties on Russia and Japan to ensure fair trade and protect the interests of the domestic industry. There was also an import duty of 7.5% levied on phthalic anhydride to protect the domestic industry.

2019-20: The company’s financial performance was impacted due to the dumping of Phthalic Anhydride (PAN) by selected countries in the Indian market in the absence of any duty protection.

2021-22: Cheap imports from other countries would result in losing the market share by IGPL. The government imposed anti-dumping duty on PAN protecting the interests of the domestic manufacturers.

Q2 FY’24: Imports in India were approximately 9,000 tons.

Pre Q2 FY’24: One of IGPL’s customers set up a plant, reducing their reliance on imports. Previously, imports were happening at around 8,000 to 9,000 tons.

Current: Import is continuing to happen in India. Last quarter imports were around 15,600 tons.

Imports are Affected by New Entrants: When one more plasticizer player started their production, the import which was typically 25,000 to 30,000 has declined to less than 10,000.

Q3 FY’24: Slowdown in China resulted in export of PAN to the domestic market in addition to the historical players like Taiwan, Korea and Russia. The ongoing red sea crisis has also affected the ocean disruption, has escalated the freight which has halted the free movement of export, has also led to supply destruction.

Notes from IG Petro Q# and Q4 FY26 concall

Q3 FY26 Concall (IG Petrochemicals)

Lower margins driven by lower realization of PAN, High cost inventory and Lower realization of Malaic acid.

Malaic is generally sold at 30% + price of PAN, during last 9 months, the prices of MAN are 30% below PAN. The reason of low MAN prices is excess capacity created by chinese players. Current MAN prices are $700 per ton, down from $1000, 9 months back.

MAN is used in single use plastics / biodegradable plastics, but chinese government is yet to enforece it, hence chinese players are selling MAN in international markets, which is impacting prices.

MAN is produced through butane, which is output of refining oil, hence, MAN is produced by integrated petrochemical projects. IG Produces MAN through waste water, and hence, cost of production is almost zero for IG.

Thirumalai is adding massive capacity of MAN in US through butane route. Its argument is that butane is cheapest in US, and local US market can absorb the supplies.

Currently Butane price in $500, conversion cost is $300, so, total cost of MAN prodcution in $800, but MAN is selling in market at $670. So, producing MAN at current prices is loss making.

IG has localized customer base, but certain customers are dependent on exports.Volume of certain end user industry is down.

DP capacity is 8000 tons, which is increased to 12000 tons by debottlenecking. DP is used in fragrance market, IG has 50% market share in DP in india.

Plastizer Capex will be finished by Mar 26, with it capacity of 75,000 tons will come online. It will require 50% of PAN. Margins in plastizers are 12% above PAN margins. Plastizer has a potential of adding 500 cr to IG topline annually.

IG P&L is currently depreciating 5 plants but only 4 plants are operational. Capex for plastizer is yet to reflect in revenues, advantage of integration is yet to come in.

IG results should not be looked in isolation, entire PAN industry is losing money. PAN realizations are dependent of international prices.

Rough quarterly production of PAN is 50,000 tons. Industry margin per ton for PAN is $100, IG margins are generally $100 better than that due to complete integration, MAN + Benzoic acid.

At 50,000 ton production and $100 margin, IG can post 50 Cr EBIDTA on quarterly basis. Capacity utilization for 4 plants is 85%.

Paint demand is 15 to 20% for IG, Paint + Pigment + Plasticizer account for 55% of demand for IG.

ADD on PAN is filed by the industry, ongoing ADD is yet to finish by Aug 26.

Q4 FY26 Concall (IG Petrochemicals)

Competing with China is not possible, IG and Thirumalai are albe to post profits because of ADD on PAN from China. ADD is ending in Aug 26, and it is recommended by Commerce ministry to continue the ADD, but it is yet to be approved by Finance ministry.

5th PAN plant of capacity 50,000 tons will be utilized of Plastizer, which is a domestic game. IG Petro do not intend to go to sell PAN from 5th plant (till Plastisizer plant is ready) to international markets, where it will have to compete with China

Elevated Crude prices due to US Iran War are causing elevated PAN prices, so, the margin % is same, but absolute profit is higher. However, not able consumer industries will be able to consume price hikes and hence there can be softness in demand.

IG is a convertor with very thin margins and possiblity of inventory price erosion, very deadly. But it is also owest cost operator due to economies of scale and MAN / Benzoic acid production from wash water , without any raw materials, it adds directly to bottomline

MAN is in oversupply due to China overproduction and thus its prices are extremely depressed. Few MAN plants in germany are closed. MAN revenues for FY26 around 55 Cr.

Margins of IG Petro are majorly dependent on PAN - OX spread. OX production is dependent on Naptha to OX conversion, and how much Naptha is diverted to PX.

Rough Capex of putting 275,000 ton PAN capacity (capacity of IG Petro) is 3000 Cr

OX (Raw Material) Mix 50:50 -Reliance:Import

90% of energy requiremnt is through WHR, so majorly energy is inhouse

0.7 ton of pan is consumed to produce 1 ton of dep

Volume Guidance for FY27 - 2 Lakh Ton PAN, 25,000 Ton Plasticizer, 8,000 Ton DEP

Reasons of muted performance -

-

Low PAN Prices

-

Low MAN Prices (90% of MAN realization goes to bottomline, MAN ralizations used to be 100 Cr a year, now around 50 Cr a year)

-

5th PAN plant not fully operational

-

Plastizer capacity yet to come online

-

Depreciation and Interest cost of 5th PAN plant and Plastisizer already accounted in P&L

2 Likes

No recent post on this scrip inspite of blockbuster Q1 profit. Profit may be due to high crude price due to middle East crisis. Another point to remember is that ADD on PAN is going to expire inthis month( any news on continuity of ADD or discontinuity will result in sudden price movement). Having said that Q1 result may drive price movement in the short term. It’s result was better then Supreme ptro as it is the lowest cost producer because of both backward and forward integration. And plasticizer production will commence from Q2 which will add to margin. It is not a big exporter , so somewhat insulated from Trumps tariff tantrum. My expectation is that ADD will be extended due to China dumping. So people looking for domestic led business may find IG Petro as a worthwhile investment opportunity at present level.

Have a small holding, so may be biased. Have not gone through Q1 audio concall. Anyone tracking it may update.