Sameer,

For me Sun is strict No No as it has got corporate governance issues.

I have now only Abbott and HesterBio. I have also DIVIs on watchlist.

So:

Abbott: MNC + Formulations

HesterBio: Animal Pharma

Divis: APIs

Good diversification, isn’t it?

3 Likes

3 Likes

I was surprised to see same 2 stock that i keen to buy …

If u have done deep research pls share about hester bio i personally feel hester will gets abbots valuations sooner or later …

Thanks

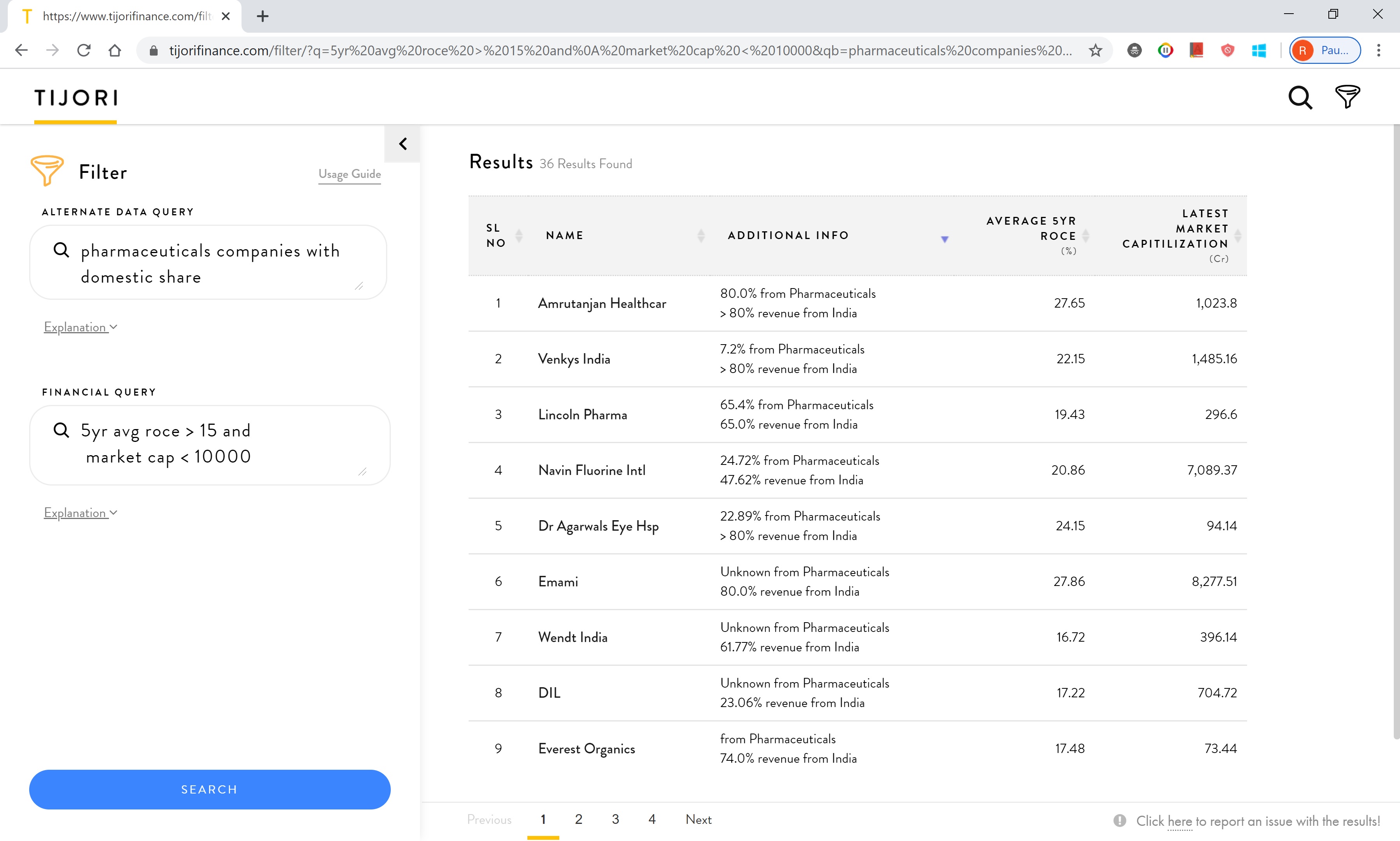

Does any one know which pharma companies are doing domestic business and which are US focused? I am sorry if it has been answered above and I am asking repetitive question. My thoughts are that domestic pharma will grow and people will start spending more on preventive care post covid.

Try Tijori Finance website - they offer filter for several key items. You will have to further refine results.

Hi Sameer,

Hitesh had recently said on his thread that the focus should be on export heavy pharma companies for now as US FDA approvals are now relatively easier

Domestic pharma companies ( cipla recently posted 30% fall in Yoy Q4 profits ) could get hammered a bit as prescriptions and hospital visits aren’t happening much.

What’s your view on pharma stocks to look at taking the above assumption to be true?

1 Like

Hi Mukund,

When it comes to investing the best mantra is: Heads I win, tails I don’t lose much. MNC Pharma companies fall in this category especially Abbott. Sooner or later FDA will hit back on Indian domestic Pharma companies and they have a hard time in recovering. If your investing horizon is long, it makes sense to hold on to consistent compounders. Simply compare the ROCEs of all the Pharma companies are you would know why some companies are better than the others.

Consider now, Divis: Divis is a major supplier to biggest pharma companies. It makes 65% of the API for world’s painkillers and about 35% of API for world’s cough syrup. Even when the company received FDA letter, it was allowed to supply some of its major products without which US companies would have crumbled. Their moat is visible in their margins which are mouth watering (25% NPM per Value Research). I think best allocation in Pharma sector (my view - no recommendations) is: 70% abbott, 30% Divis.

Source of Info:

4 Likes

Excellent insights specially for new investors who wanna understand pharma sector basics.

6 Likes

A nice video on the detailed underpinnings in global pharma.

Another nice followup is the PPFAS video from a couple of years back

5 Likes

One thing is clear - Pharma is not moving up because of expectation of increase in domestic consumption. It is going up with simple reason - expected relaxation of FDA approvals. 52 Week high by all sector, breaking 5 year highs is good. But imagine if one FDA re-issue props up then what will happen ![]()

Now, if that happens or not is anyone’s guess.

2 Likes

I think it’s going up for a mixture of reasons. Not just expected relaxation of FDA approvals. In any case, US exports are not equally important for all India pharma companies. Of course the pandemic has a lot to do with it, since the expectation is that the demand for drugs will at least not reduce for this period, plus the expectation that other sectors will be more severely impacted. Pharma in general can be expected to do well in a recession, regardless of its origins, because it’s essential spending. Though the current market doesn’t seem to be paying much attention to realities on the ground.

I don’t know if one can quantify this trend, but recently it has seemed to me that the Pharma sector has been moving in the opposite direction to the broader market, particularly finance.

Also keep in mind that many of these companies were very underpriced in March when their stocks started rising. In some cases those companies have just returned to the levels where they were 5 years ago, in 2015.

2 Likes

I will recommend not to dilute the quality of discussion by pointing to different patterns on price charts (for that we have threads on chart patterns and technical analysis). About what changed? I don’t know, market sentiment probably which is very hard to forecast. I have been studying this sector for the last 3 years and here are my observations with specific examples. As I have mentioned earlier, pharma should not be looked at from one simple lens.

- Better compliance of large pharma companies. Sun, Lupin, Dr. Reddy, etc. had lots of compliance issues, a lot of which have been addressed. For ex: Lupin recently got EIRs on about 5 of their facilities, Sun got its Halol facility out of warning letter sometime back (only to get an OAI again!), Dr Reddy’s plant got an EIR, etc.

- If you actually look at price erosion trends for generic pharma, it started getting better sometime last year with price erosion going back to single digits (all pharma cos talked about this on their concalls)

- Smaller pharma companies (Ajanta, Alembic) started growing their US topline at 20%+ rates. Just look at their topline numbers for FY20, you don’t need to wait this quarter. It didn’t start in Q4FY20, but started somewhere in the beginning of FY20

- Biosimilars have started to gain traction (look at biologics division topline of Biocon). Lupin got its first biosimilar approval in Europe and will launch this quarter.

- The complex generic pipeline for a number of Indian pharma companies is very strong, with a new focus on injectibles and inhalers (look at CIPLA).

On top of this, Lupin and Sun (leaders of large pharma bull market) were trading at 2 times EV/sales which is a historically low number. For a business which generates 20% operating margins, free cash at reasonable ROEs, an EV/sales of 2 times is incorrect at a 10-year Gsec rate of 6%!

All this said, currently market hasn’t differentiated b/w pharma companies giving similar price appreciation to everything that is pharma, this differentiation might happen at some point in the future. These are some of my observations and I will like to indulge in a healthy debate about specific companies.

13 Likes

Pharma Co are not homogenous and each one is in different level of maturity life cycle

The industry structure for Branded Generic ( esp India ) is very different for industry structure of API unit or Generic US pharma or Selling Patented Orphan drug .

Add to that R&D cost , establishing S&D structure is front loaded and gains come in lateron

Lets say you have company like Lupin/ Glenmark / Sunpharma -

Which has branded generic in India , API , Generic US pharma , Complex generic + biologics+biosimilars , Orphan drug etc …

How will you decide which is better value … very difficult even from Industry veteran .

So what is best way to build a Portfolio of Pharma stocks is by using with following basic metrics

-

Enterprise Value Indian Branded generic sale @ 5-7 times ( 7 times if Market share > 20% in that respective therepeutic area , otherwise reduce it depending upon market fragmentation )

-

EV of US + EU generic sales at 1.6 to 1.8 times ( Again with more Para IV or Orphan drugs or Complex generic you can increase to 1.8 times sales )

-

EV of ROW generic sale + API sales at 3 times sales

I found the above to be very good indicator of fair value of different stocks ( by the way most private deals happen at above valuations )

6 Likes

This is also my way to evaluate companies, i.e. sum of parts kind of valuation for different geographies. However, I did not quite understand how you came to these multiples. Also, what multiple will you provide for complex generics, inhalers, injectables and biosimilars? There is no historical precedence in the Indian context.

For complex generic business, margins are >20% and ROCEs are >15%, a 1.8 EV/sales implies a P/E of 12, which other business with these statistics get traded at these multiples?

Also, why give a higher multiple to an API business than a generic? API has much lower entry barriers and only companies with scale can win this game, where India as a country is at a disadvantage over China due to higher cost of power

1 Like

SInce you too evaluate companies you can share how you value companies . This will facilitate discussion better .

On Complex generics - TEVA / Mylan are examples of companies that are ahead of Indian companies - You can check their range of EV/ Sales and get and Idea for US generics what EV/Sales you would like to give …

On API again dependents on complexity / competition etc … currently DIvis trade at >10 times EV /Sales … You can again take call what you would like to assign multiple to any individual companies after understanding their product profile

That said what I have given above is broad framework for one to decide which companies is expensive or cheap … Once you get a list you can delve into details to understand whether value equation is correct .

1 Like

I am not completely familiar with the product profile of TEVA/Mylan, I will analyse their financials soon and get back.

Divis has a large CRM business which is very high ROCE and very high margin, which is why it commands a premium and not due to its generic APIs. For pure play APIs, a better comparison will be someone like Granules. Also, the long term (2004-2020) EV/sales average is ~7. The last time this ratio was >10 was in January 2008 when the value went up to 14x and then came down to 4.5x in March 2009.

I agree and thanks for pointing it out, its very useful ![]() I have tried to explain my analysis of different pharma companies here. I will get down to the valuation part soon

I have tried to explain my analysis of different pharma companies here. I will get down to the valuation part soon ![]()

2 Likes

Some very rudimentary observations about the pharma industry

- More than 20 companies that trade at a market cap > 10,000 Cr

- All of them are profitable at an average promoter holding of 55%+

- Mid size companies as of date are tracking better on capital efficiency that the large ones. The large ones have grown at 10%+ even during the past 5 years

- Barring the 2015-2019 period, more often that not pharma has made money for investors

- On an average the gross asset turns is around 2.5x, for specialized players this can go as low as 1x but with much higher margins to ensure ROCE stays above the 20% mark unless there are huge R&D investments

Unit Economics

At a gross asset turns of 2x, one needs 100 Cr capex to make revenue of 200Cr. Assuming a working capital cycle of 120 days, this revenue base will have approx 70 Cr stuck in working capital. Hence on a capital employed base of around 170 Cr, to make the ROCE threshold of 20% pre tax, the EBITDA margin (assuming depreciation to gross block of around 6%) will need to be higher than 20% - which most companies manage to do.

For this reason my take is that making money in a pharma business consistently does not take too much of management skill. This is one of those business segments (like IT services) where an average management can be profitable on a consistent basis and grow the business at a hygienic number.

Extending this very same logic, I see greater value in reducing risks than chasing after the mythical unicorn which can net multibagger returns from the current price. Such multibagger returns tend to occur in industries where you have a consolidated market structure and 1-2 players end up dominating the industry for years to come. I just do not see this happening in pharma unless one has very deep domain knowledge and understands all perspectives well - product development & research, developments in customer facing markets, regulatory oversight, legal and other perspectives. None of our pharma companies are into high end research anyway, so the possibility of outsized returns from a single drug/R&D endeavour that can last for years is close to NIL.

So my expectation from the pharma basket is to look for 15-20% return over the medium term while minimizing risks on the regulatory & legal fronts. Now PAT growth by itself may well deliver 12-15% for a decently run pharma business, so the 15-20% target is actually immensely doable.

I hence prefer the principles of elimination for the pharma sector rather than selection. One also has a lot of choices in this sector, so practical considerations should matter too.

My ideal mix would be -

- One strong domestic market focused business that is not too expensive

- 1-2 API makers that are well positioned to benefit from the local manufacturing drive one is likely to see

- 1-2 formulation heavy businesses selling into markets where the regulatory environment is either easy or getting easier, these need to be able to deliver around 20% revenue growth. Also track the commercialization schedule of ANDA’s already filed over the past 3-4 years. The easiest way of siphoning off money in a pharma business is ghost R&D and one needs to spend some time to rule this possibility out

- Niche player only if one is willing to do the work it takes to understand the business really well and quantify the risks involved

What I would want to avoid -

- Those with a history of US FDA observations where things could not be resolved within reasonable time

- Organizations with promoter pledging, history of frequent capital raising and M&A activity

- Those that are tracking very low on ROCE (which means a lot of investments have been made which are yet to bear results and one does not have a handle on when these could pay off and to what extent)

- Businesses that are too expensive relative to the growth prospects

34 Likes

Hi, I am not sure if I am asking something which has been asked. I think it will be good to pick 1-2 companies which are domestic and focus on India business. Also pick 2-3 companies which are export based and 1-2 focus on chronic disease. Also 1-2 could be injectable and rest could be oral.

My question is how to get this information. e.g. I have shortlisted few companies like Dr Reddy, Aurobindo pharma, Granules India, Alembic pharma, Jubilant Life science, Divis, Sanofi. But I dont know which one operate in domestic and which is majorly export based. Also which one focus more on chronic disease. I know Jubilant Life science focus on radiology, injectables. But dont know about others. So any guidance or pointer will be helpful