HDFC Bank shows a bearish head and shoulders breakdown. It has been trading below 200 dema for quite some time even before last week’s crack. And on the way up during the Covid rally it has been a relative underperformer. Target could be 1150 region which was the neckline for the cup and handle bullish pattern on the way up which can be seen on left side of the chart.

16 Likes

Reliance. I was bullish on this earlier over the medium to long term looking at the flag like breakout. But now it too seems to be weakening in the wake of generalised market meltdown. The head and shoulders pattern is not classical here, but on the whole pattern looks weak with a nearly 300 rupee fall if the pattern plays out.

14 Likes

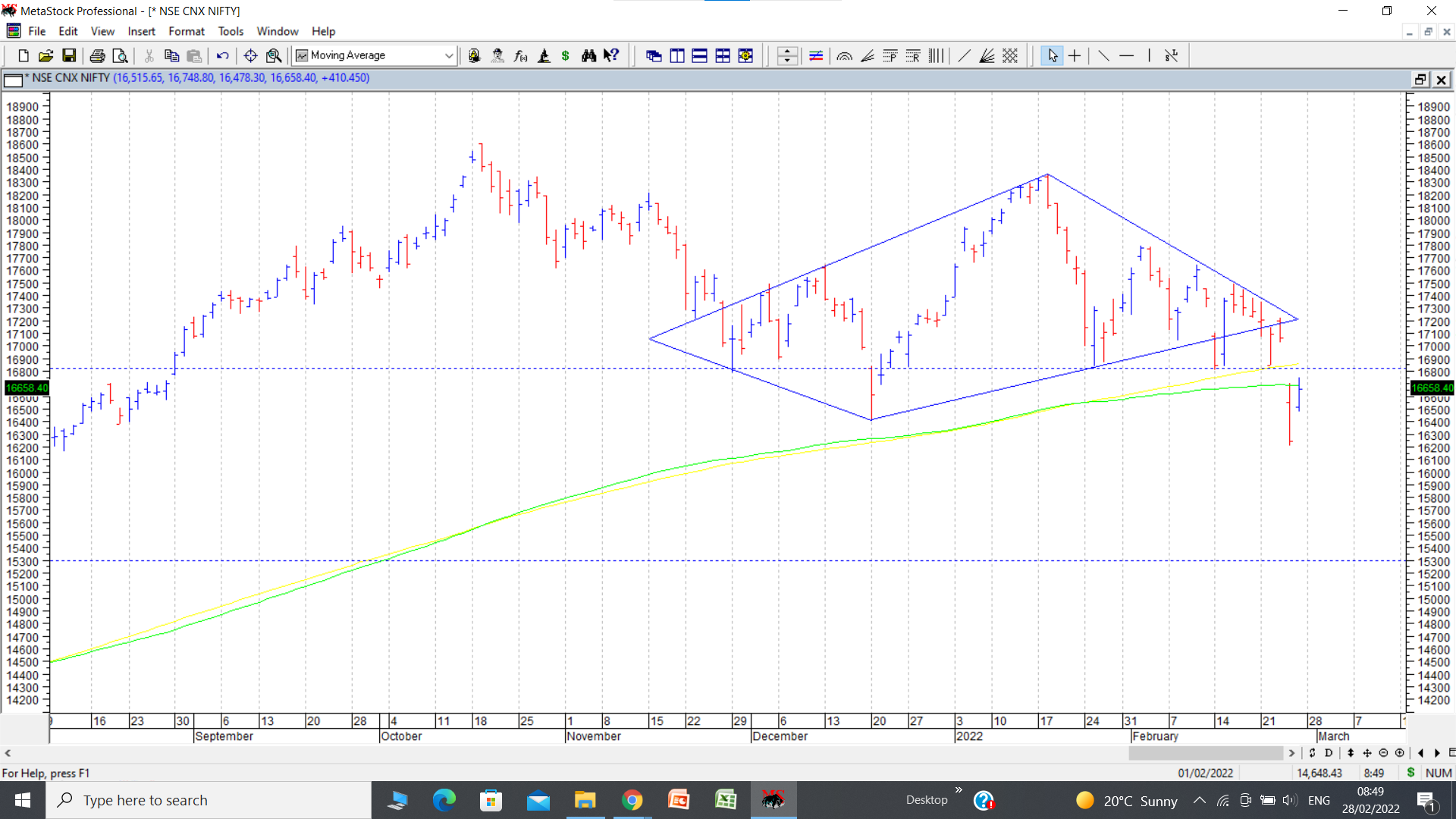

Nifty seems to have broken down from a diamond pattern. (this is similar to a 3D image of a head and shoulders pattern. If we take out the dip to 16410 during earlier fall in Dec 21, then there is a clear head and shoulders breakdown. If this pattern plays out, target can be 15300.

16 Likes

Now after all these bearish patterns staring at us, we also have to think about an alternative scenario. What could make us change our bearish stance?

First would be going up above gap down area of 17000.

Second would be sustaining above 200 dema again above 17000.

Improvement in market breadth for a few days in a row.

Formation of higher low and higher top again. (we have had lower top at 18600 and 18300 and and lower low at 16400 and 16200 now for two instances.)

Personally as mentioned before, I am wary of buying the dip and in fact raised some cash on Friday’s bounce. Lets see how things pan out. My guess is this week should provide some clues to market direction for next few weeks.

39 Likes

what is your views on chart strength having characteristics

TA

all time high price and

all time high volumes

RS 73

strong resistance stock with drying volumes but above 50 SMA

FA

EPS growth 6 consecutive quarters

pre tax and post tx margins improving yet sale is decreasing

no equity dilution over a decade

sector agriculture chemical and almost very small debt

regards

I don’t track solara active pharma actively so have not listened to any concalls etc. But a look at quarterly numbers you highlighted indicates that the dec qtr results were a bolt from the blue. Maybe there is an explanation for it. Historically the promoter group has been well known for mergers, demergers, acquisitions, divestments, you name it, they have done it all over the years. This kind of history does not inspire too much confidence for long term investors.

I think a simple thumb rule like selling once the stock consistently traded below 200 dema would have saved a lot of blushes. If you see the charts putting in 200 dema indicator, then at a level around 1500 in Sep 2021 , there was ample indication of an exit.

Interestingly though, on 11 Feb 2021, there seemed to have been a selling climax with huge volumes, in fact highest weekly volumes ever. So one might keep it under watchlist for any strong bottoming formation. Usually such high volume selling climaxes indicate a short term bottom. Need to see how it goes.

@jack I don’t think we can write off pharma story at any point of time because of the kind of business it is. However there will be periods of ups and downs. It had a spectacular run till around 2015-2016 and then went into hibernation. In early Covid scare it made a sort of resurgence but it was short lived and since then it has again gone into hibernation. At the risk of sounding like a broken record, I would like ot reiterate that a sector that loses market fancy often takes a long long time to make a comeback. As investors and traders, its better to board running trains, rather than stationery (or those going in reverse direction. )

@ram1984 I dont track RHIM too closely but if the steel sector remains strong, it can do better than peers.

@yourraj I dont like talking or answering in riddles. You can put up the name of the company and we can discuss it.

16 Likes

Sir it is Gujarat Narmada Valley Fertilizers & Chemicals

Hello sir

It would be great if you can suggest your thoughts on Sree Rayalaseema Hi-Strength.

I can mention facts if you like.

Thanks!

GNFC is on a strong wicket because of its industrial chemicals division. It has reported very good numbers for past few quarters and that has led to a strong rally in the stock price. It crossed its previous all time high of 540-550 and showing good resilience in a weak market.

Only thing to watch out for in these commodity chemical companies is the prices of the main contributors. Once finished product prices correct sharply as is usually the case in most commodity chem companies, stock prices too can crash. But as of now everything seems hunky dory and chart too looks good.

Personally I am on the sidelines and waiting for the markets to settle down and show some kind of strength and then take a call.

@Shikhar_Seth I dont track shree rayalseema so not much idea about the business. Ayush Mittal might be a better resource person on this.

5 Likes

Hello Hitesh sir,

If you are tracking, it would be great if you can give your views on M&M Finance and whether it can benefit from the ongoing reversal in the Financials sector.

Hi Hitesh sir

Appreciate all your efforts and guidance

Sir What are your views on gold finance companies

Many Thanks

Mahesh

MM fin is a play on rural India credit growth. From a concall of MAS fin, someone asked a question about stress on rural economy and from whatever I could gather, there seems to be some stress there. So MM fin probably is correcting in line with that logic, though I dont track it too closely. I think for someone with a 2-3 year view, it might provide good returns as these stresses in individual pockets of economy tend to normalise over time or the companies find ways to get around those. In short term stock price has been under pressure.

@maheshkumar There are mainly two pure play gold loan companies in listed universe. Mannapuram and Muthoot. It seems Manappuram has been under pressure due to loan book issues in NBFC part. (need to verify that. ) Muthoot by comparision seems better placed. With most PSU banks flush with money and gold loans offering a safe lending environment, there could be strong competition for gold loan customers. This probably can continue till banks start focussing on industrial and other segments.

In general too markets have been very weak and a lot of stocks have given up a lot of froth and now seem to be within reasonable range of valuations with respect to their growth prospects. But with the uncertainty related to the Ukraine situation, things are unlikely to look up unless the event is resolved one way or the other. But I feel it might be the time to make a buy list and start dipping the toes with small quantity purchases. There will be some stocks which will bottom out much earlier than the entire index and those are the ones that need to be looked at.

20 Likes

Thanks for the wonderful guidance as always, Hitesh sir.

Sir do you have any views on Jubilant Foodworks? They have made a lot of acquisitions and starting new brand chains in India. Other than recent geopolitical risks, what else might be weighing on its stock?

1 Like

Hello Hitesh Sir.

Could you please share your views on Jubilant Foodworks and its current fall. I am an investor in JubFoodwrks and currently sitting on a loss of 22%. Is this a good time to accumulate more of it or will it correct even more?

Hello @hitesh2710 Bhai,

Can you please share your views on Sapphire foods and generally QSR companies.

Hello Hitesh Sir,

Can you please share your views on TTK Prestige ?

Hi @hitesh2710 sir,

I have been tracking the Textile Industry and can see some great sectoral tailwinds. Invested in Trident from single digits and post digging understood that they are in the capex mode (digital + offline stores) mode which may take time till FY25 to show the compounded returns.

What’s your view on the whole Textile sector and Trident Ltd if tracking?

2 Likes

I do not track sapphire foods or jubilant foods in particular. But QSR companies have a long runway for growth going ahead. Some of the brands these companies have, do have a lot of pull and the delivery platforms also help in augmenting their reach.

Having said that, markets probably went overboard in valuing their businesses and that probably is getting corrected with the kind of correction we are seeing in these names. (and in fact in most names, even though they may not be too expensive  but that’s not pertinent to the topic here)

but that’s not pertinent to the topic here)

The problem I see with a lot of these QSR organised players is the kind of competition they face from locally popular outlets and other mom and pop type of operators. In my city itself, I cannot bring myself to order from Dominoes if I were to go by my choices and preferences. The same might be the case in a lot of other cities too.

But having a pan India network and big advertising budgets helps and over a period of time these companies can devise strategies to strengthen their brands and add more names to their bouquet of offerings.

I think the current correction is taking out the froth from a lot of names and more. The pendulum is probably swinging from overoptimism to the other extreme gradually and might be a work in progress. So although as businesses these names might be great businesses, we have to figure out at which levels of valuations they make great investments.

The charts of a lot of these companies have broken down and will need a lot of repair and mending before these names make a comeback. So as of now personally I would not venture out to be too brave and start buying unless I see atleast some signs of stability in markets and signs of reversal in the charts of these companies.

@Mayank14 I haven’t tracked ttk prestige since a long time so not much idea. On the charts, 710-780 was the zone of consolidation before the stock price took out its all time high zone of 890-900 and went above 1200. We need to see if the stock price gets some support from the consolidation zone mentioned and then maybe take a call.

13 Likes

Some while back there was a lot of noise about sectoral tailwinds for textile sector. Many of the textile stocks had given good results and stock prices too appreciated.

But of late, a lot of input prices have gone up and we need to see how competitive these companies can be on a global scale with problems related to spiralling raw material prices, freight costs, power and fuel costs etc. At some point of time a lot of these export focussed companies will be able to pass on higher costs but there is always a lag period and if it lasts a couple of quarters and companies do not report decent results, stock prices take a huge drubbing. I used to own ICIL and had got in around 170-180 mainly based on a very good technical set up and good quarterly numbers but on achieving targets in range of 260-270, I had exited. Even after that the stock prices did show some strength for a while but I did not fancy my chances then. Now today I looked at its price and its below 160. That’s the kind of brutal hammering these kind of cyclical companies have received. The one lesson that has been re inforced for me by this example is not to overstay our welcome in cyclical companies. Its very difficult to figure out when the music is going to stop.

18 Likes

Hitesh Bhai, suppose If one wishes to invest decent in Nifty rather than taking uncertain bets, what levels shd one look at nifty

2 Likes