I find it difficult to understand the business model of insurance companies. So I have left them alone till now. Now I have decided that if at all I take a dip it will be when I see a good chart pattern. In the short term there could be some excitement in these names due to the impending IPO of LIC.

I dont track Mastek, so not much idea about promoter buying and its impact.

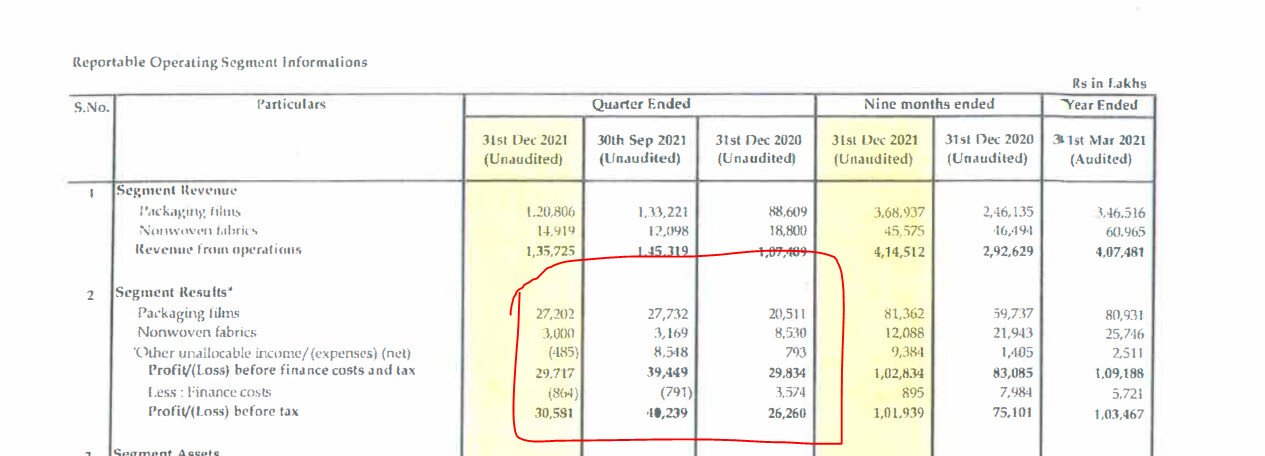

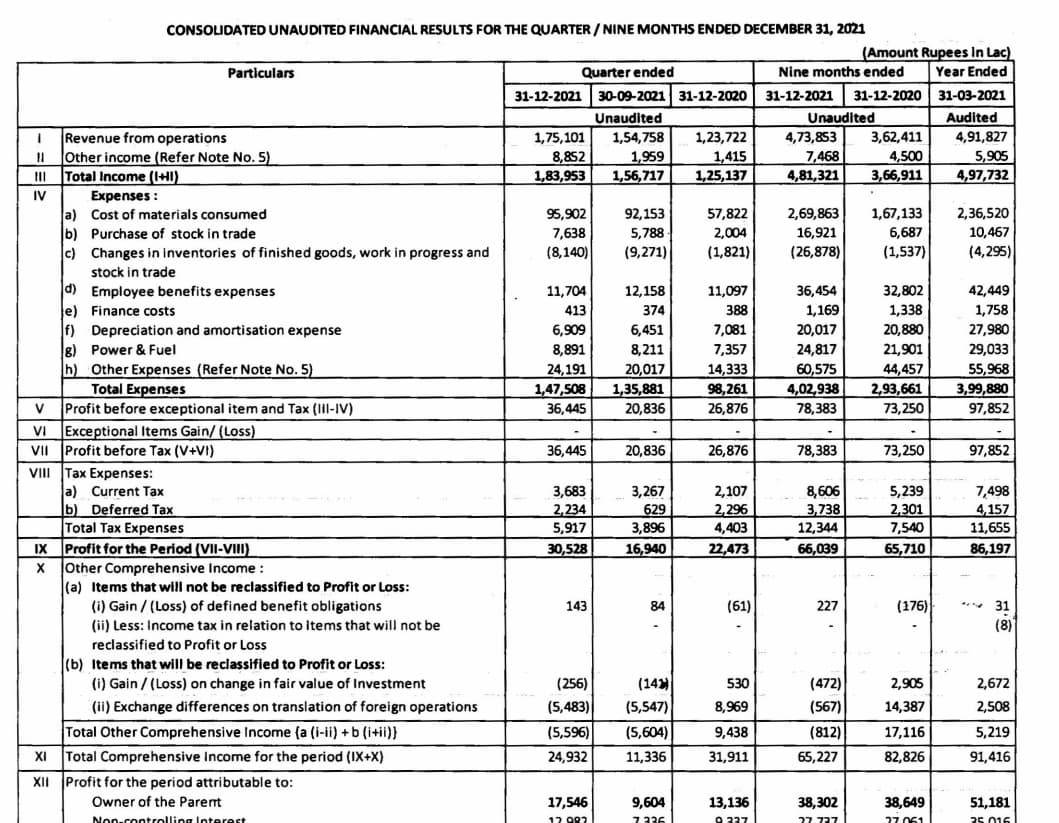

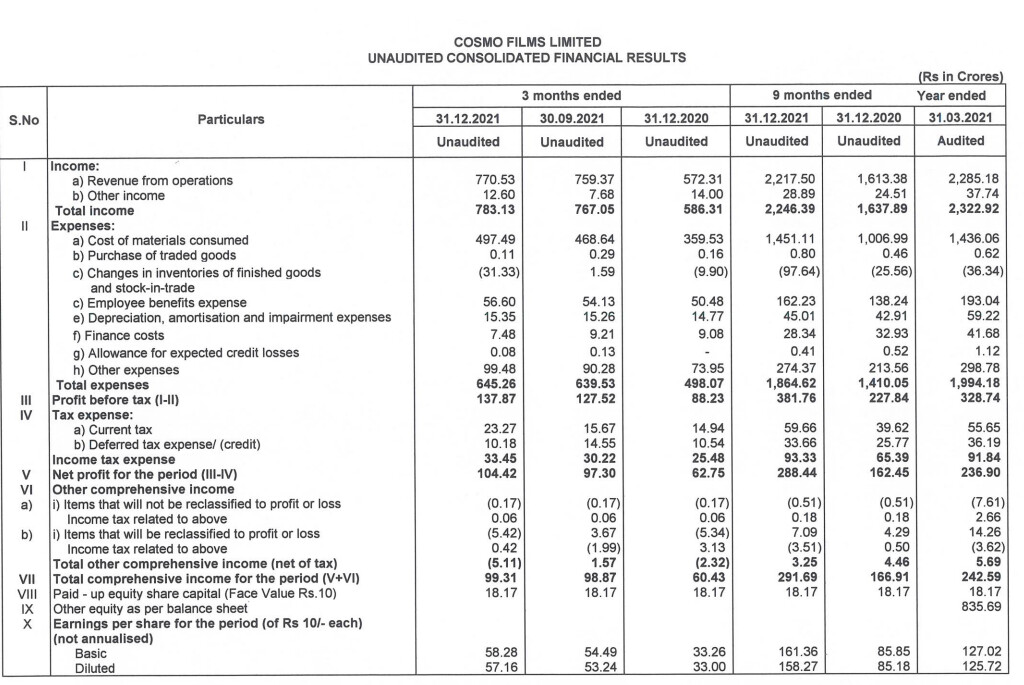

Most polyfilms companies have posted good results for Dec qtr. Uflex numbers are the standout numbers in terms of impact. But I do not like the management and have not looked at it closely.

Among others, in order of preference, I like Polyplex, Cosmo Films and Jindal poly.

The only problem with this sector is that its a typical cyclical sector having a good time and we have no idea how long this is going to last.

Polyplex q3 fy 22 presentation provides a good outlook for next quarter barring unforeseen circumstances. The other good aspect of Polyplex is dividend yield which remains very healthy. And the possibility of stake sale by promoters.

Your assumption that banking/financial and technology have higher weightage in most portfolios, even mutual funds is correct.

Coming to current scenario, I have observed resilience/outperformance from banks/financials since past few weeks and months. I think there is a case to find out good companies in the space and invest in them.

Fundamentally most of them are coming out of stress and have now started reporting very good numbers since past couple of quarters. Secondly if economy were to revive, there could be a strong demand for credit and that would provide growth impetus to these companies. Many of them are available at very attractive valuations.

I am personally invested in Karur Vysya bank as a techno funda bet. One can also create a basket and try to play the theme.

Hitesh Bhai - Read about the above and it looks interesting, aiming to become an integrated player. Upcoming financial burden, needing 700 Cr. for the ISMT acquisition and 700~1100 cr. for planned capex in the next 18~24 months, may become a drag in case the business cycle turns negative. However, I assume that the the group is well reputed and can wiggle out of such a worst case scenario.

What will be the tipping point for you to change the status to ‘holding’ from ‘watching’?

Hitesh Bhai, how do you read Schaeffler Q4 results. 20% increase in topline and 35% in profits. PE now looks like comes to 40 from 43. Do you feel the growth now doesn’t seem to justify valuations?

In case of kirloskar ferrous, I would want to see a quarter or two of good results along with strong confident management commentary. As of now although there is topline growth, margins seem to be constantly under pressure. Plus the integration of ISMT successfully would be an event that needs to be watched.

The thesis here would be transformation of a part of the business from pure commodity business to a more stable converter type of business. The latter is less vulnerable to raw material price fluctuations.

If the transformation happens successfully, then there could be some amount of re rating. But as said before it remains in watchlist.

Schaeffler results have been very good. Both topline and bottomline growth has been good. But run up had already happened before results and hence I think price will probably undergo some consolidation before making a major move.

Maximum money is made when there is positive surprise. Here, a large part of the results was expected if we look at the pre results rallly. And 40-45 PE is not too cheap. At such valuations, one has to invest considering growth prospects. If we invest at such valuations, re rating may not be too much, unless we have another madcap frenzy. So returns expectations has to be in line with growth rates.

Technically it has formed a lower top and lower bottom formation by breaching an important bottom level of 1686. On the back of good results, there could be a bounce, but scaling the previous all time highs might prove difficult.

In the current market, we have many examples of companies delivering good results and still remaining range bound. I think the scenario is that if results are out of the park, (e.g sharda crop), stock can go up a lot. If results are as expecated or only slightly above expectations, stock price remains range bound. Or corrects slightly if stock price has had a strong run up prior to declaration of results. (e.g acrysil, pokarna, usha martin) And if results are poor, all hell breaks loose. Making money consistently in these kind of markets is often difficult and we may need to temper our expectations in the short to medium term, or enhance the investment horizon. How long this phase of markets last is anybody’s guess.

Had a Question related to low float stocks. We’ve seen what happened to Hle glascoat. Stock was cornered and when few institutions came in+ earnings kept growing. Stock went beyond even the wildest imaginations to 6.5k from barely Rs100-200. As earnings compounded with cornered float. I sold out at 850 and missed a 30bagger in 2 years. (Game of regrets)

Similarly currently I own Saregama. Which is again a story of low float+Strong potential for earnings to compound at 25-30%+strong industry structure.

In such companies is there any selling framework that can be used? As it often ends up becoming an example of theory of reflexivity.

More earnings growth+Float cornered=Virtuous cycle.

What is your funda or techno Criterion in such companies?

How does one deal with such situations wherein the stock is richly valued at 40 times earnings while the company keeps delivering decent growth and improving ROE quarter after quarter?

One approach is to keep holding the stock hoping the co’s growth momentum continues and let the stock price take care of itself over a couple of quarters.

The second approach is to take some money off the table when a rally happens, thereby protecting gains made until this point? One of the rules I’ve heard about but never followed till date is “When in doubt, sell half. Repeat”.

Which of the above approaches works best based on your experience?

Hitesh Bhai - while nifty hasn’t corrected much( 6% ) and neither did Midcap index( 10% type), many proven and time tested quality names are well below 200 EMA and some even below long term median PE valuations. To name few

ASTRAL, BALKRISHNA, LALPATH, HDFC LIFE, DIVIS , PI IND , HDFC, HDFC Bank , HUL , Infoedge, Havells and possibly many more. Even Asian paint etc are near 200 EMA.

While there are sector/stock specific near term margins/mkt perception aspects. Possibly FII exit could also be weighing on these.

In your views, large pool of these names having hugely underperformed in short term relative to index is indicative of something at broader level or one should take stock specific view?

How should one approach technicals in fundamentally sound companies in cases like 200 EMA breakdown/death crossover etc? Thanks.

Low float, low liquidity company showing great growth is a recipe for multibagger.

I attended the AGM of HLE, (Swiss glasscoat it was named then) before all the fun and games began. Got good vibes, but looking at very thin traded volume, at around 180-200 gave it a miss… Talk about regrets.

Selling these is the most difficult part. Especially in HLE where a business depending on Pharma/speciality chemicals and chemicals capex was taken up to crazy valuations.

I think there is no one size fits all kind of answer to problem of when to sell. Better to be following the concept of free shares. Sell partly, recover original investment, keep riding the rest. Though I find it difficult to implement and too simplistic.

Or follow some long term moving average like 100/200 day EMA, and sell on its breach. You may not be able to sell at the top, but certainly at 20-25% below swing high.

Valuations wise I think cos find it difficult to continuously sustain valuations of more than 100 PE. So maybe something to latch on to there.

If saurabh mukherjea is invested in same company, then one may give a long rope to the stock.

In the short term, zydus wellness chart seems to have broken key supports and looks weak. Fundamentally I dont track it anymore. But on longer term charts since 2012, especially using the semi log scale, it seems close to a support on a long term trendline. We need to watch out if the stock price takes support closer to this trendline and shows any signs of reversal or not before contemplating an entry.

A second one might have a falling stock price much before the big fall happened earlier this month. Perhaps the market was already skeptical about the co’s future prospects?

Dear Hitesh

Is it the pharma story ending? Whether the money is moving out of defensive to growth story, since the covid fears are behind us. I can feel lot of big pharma breaking the supports, like wockhardt, Lupin…your thoughts please.

What are your views on refactories viz. RHI magnesita. Many steel companies are contemplating huge capex as they are getting ready to meet increased demand. We can read arcelormittal Nippon plans of huge capex in India. Any views on this ? Stock had a good run up recently on the back of good results

We have seen severe cuts across the indices and many stock prices. Reminding us of the kind of falls we saw during the Covid fall back in Feb -March 2020. This is one of the few instances when the 200 dema has been broken and there has been a huge gap down. The gap ranges approximately from 17000 to 16700. And today’s close is close to 16250 which is nearly 450 points below the lower range of the gap.

Many stocks have formed bearish head and shoulders, rounding top etc kind of bearish patterns.

In the near term we seem to be extremely oversold and can see strong bounces in response to some kind of positive news or even letting off of negative news. How and when this bounces materialises needs to be seen.

Personally this time I am a bit worried and not too keen to buy the dips which earlier used to be the thing to do. I would first like to see the broader market settle down after the fall and see some signs of markets bottoming out and then take a call. Till then my stance would be to sell on rallies except in companies where I am quite clear about the growth path going ahead for next few quarters.

Will update once the picture becomes more clearer.

Some large cap charts have formed clear cut bearish patterns which causes concerns about the overall market direction. Putting up L&T chart below which shows a typical bearish head and shoulders pattern with potential targets at 1530 marked in dotted line. Solid blue line is previous all time high region of 1585. So if the bearish pattern plays out then these are the targets we should watch out for. 200 dema at 1730 remains a crucial level to watch out for. On Friday there was a gap down on daily charts ranging from 1800-1816 which needs to be watched out for resistance.

Making money consistently in these kind of markets is often difficult and we may need to temper our expectations in the short to medium term, or enhance the investment horizon. How long this phase of markets last is anybody’s guess.

Making money consistently in these kind of markets is often difficult and we may need to temper our expectations in the short to medium term, or enhance the investment horizon. How long this phase of markets last is anybody’s guess.