Praj has nearly doubled from its level a few weeks ago. So although the performance has been good and guidance is good, one needs to consider where there is comfort in buying. With ethnol blending the flavor of the season, Praj is likely to find a lot of takers so even as a momentum play it will do well. But idea should be to buy on consolidations rather than run ups and rallies.

Whether its a cyclical play or a structural story, only time will tell but at some price, the valuations will capture the structural story as well.

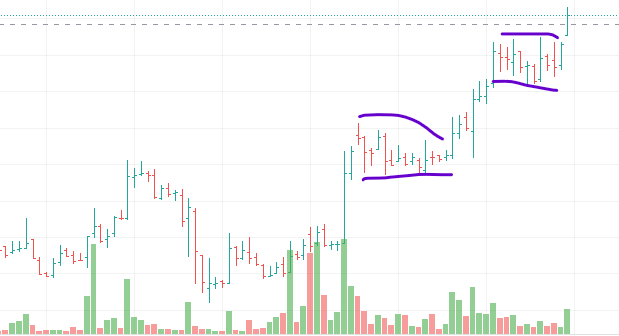

Most stocks in an industry with strong tailwinds will more or less show strong bullish patterns wherein stocks emerge out of strong base formations and start hitting 52 week highs or all time highs. Normally there is a strong rally after which stocks undergo sideways correction , usually without giving up too much in terms of price correction. This is often just a time correction. During this phase, volumes shrink noticeably . Volumes on up days are higher as compared to days of downtick days. And then stock price breaks out with heavy volumes. Volumes in these types of breakouts are often many times those seen in the consolidation phase.

Best resource to figure out these price volume patterns is to look at chart patterns of successful breakouts post base formations. Threads on technicals on VP are also very good resources. I often find good ideas from charts posted by smart guys on these threads.

You can watch Mark Minervini videos to know more about price volume breakouts.

The one thing that moves stocks in the long term is earnings. Nothing matches fast growth in companies. If you are sitting on a fast grower which does not move much, then it should not be a cause of concern. Every stock in a strong uptrend needs to consolidate for some time after a strong rally before it begins another leg of the rally. More the consolidation, stronger the breakout.

In a portfolio of say well chosen 10 stocks, usually what happens is that a couple of them are going to be range bound whereas maybe 3-5 will move fast and rest will move slowly or even go slightly down. What we have to see is the overall portfolio movement because thats where our returns come from. And that is the reason to have a portfolio approach.

Fundamental premise of a portfolio approach is that we do not know which of the portfolio stocks are going to generate the fastest and most returns as compared to the rest.

It is often frustrating to look at a certain stock in the portfolio which barely moves whereas others go up a lot. But that’s how a portfolio works and we have to learn to live with that. If one is aggressive with a trader mindset, there might be a case for a few switches here and there, but there too chances of the stock being sold going up a lot after our selling remains.

One needs a balance of patience and aggression in handling a portfolio. Usually keen observation of how things work out over a period of time teaches us a lot.

I own sanghi inds as a techno funda pick. Levels of 43-44 was a crucial level being the 52 week high. It got taken out by a gap up move and that gap remains on daily charts. Now its trying to cross the congestion zone of 48-50.

q3 fy 21 results were good. I also track the results of other companies operating in the same geography and one of the companies is shree digvijay cement. The latter has posted very good results for q4 fy 21 and could give some indications of what to expect from Sanghi inds.

I would not rate it as a very high pedigree company as compared to some top notch cos in cement space. But I have got into cement as a basket, owning orient cement, india cement and sanghi cement. I have definite stop losses marked out for my positions.

Regarding losing momentum, I have a different view here. It recently gapped up (43.70 to 45.50 was the gap which was not fully filled. It still remains unfilled) and broke out from a triangular consolidation, so seems well poised to move higher. Lets see how it goes.

Hi @hitesh2710 sir, i am still learning. Sanghi industries is paying high interest and carry high pe (if it starts paying tax , pe further up) . is it better than other player ncl industries (cement) which has low pe(7) and minimum debt.

Sanghi inds has taken up big capex of around 1200 crores and hence interest payment might have gone up. Though I see interest costs as being lower as compared to a year earlier . But overall debt has gone up due to capex.

I dont track ncl inds to no idea how to compare the two.

Do you track Neuland labs. What are your view on this after the results. The stock has corrected since the result missed the estimates.

What is your view on this from long term perspective

Hi Hitesh bhai,

I have a doubt regarding cyclicals like JSPL/Hindalco

Over the years investors or promoters did not seem to earn much via stock price appreciation. What is the incentive for promoters/owners of the business if stock price goes up & down?

If profits are not getting added up to stock price, where does the money earned by these companies during up cycles go?

Are most of the cyclicals are not long term wealth creators?

Is it not worthwhile to look at cyclical universe for long term compounders?

In cyclicals the story is usually typical and oft repeated during cycles. Business goes through ups and downs. During down cycles a few companies fold up and the stronger ones remain, only to prosper during good times. During upcycles, profits grow multifold . But then there is a popular saying that comes into play. “The more the money in your pocket, the more the urge to piss it off.” So these guys get carried off and take on massive capex only to see the cycle having turned by the time they have completed their capex.

As investors, one thing we always need to keep in mind is that cyclical stocks always have a sell price and date. We cannot expect cyclicals to behave like structural growth stories.

Now question of why would anyone want to do this business? Well, it takes all kind of people to make our world. So there are those who want to do those kind of businesses. Not ours to question why. Our choice is to invest or not and at a price and time of our choice. But that’s where most investors falter. The momentum of cyclicals going up is so welcoming that a lot of investors get sucked in at the wrong time and price.

One group of companies often termed cyclical but have been long term wealth creators have been high quality cement companies. Companies like shree cement , jk cement, ramco cement, etc have created huge wealth over the years in spite of being labelled cyclical.

I wish I knew in which stage current commodity cycle is. I would be minting money by the tons then.

But there did seem to be some froth in steel and some metal segments with everyone and their mother wanting to invest in the sector. There seems to be some cooling off in last few trading sessions whether its a major turn or just a pause in upmove needs to be seen.

Some other strong sectors seem to be cement, sugar, tea, coffee, polyfilms esp BOPP.

@hitesh2710 , Hitesh bhai would like to know your view on Shakti Pumps after their turnaround performance this year. Looking to the astronomical size of opportunity in KUSUM scheme for Solar Pump, do you think the Company and management has ability to scale up the business from this level.

@hitesh2710 Sir, please have a look at Bajaj Steel Industries. Looks like a good ‘technofunda’ bet for next 3 to 5 years

I have attached the word doc with the graphics and commentary Bajaj Steel.docx (1.6 MB)

Views invited

Thank you!

Disc: not invested yet, but planning to take a position around Rs 545-550 levels

Our choice is to invest or not and at a price and time of our choice. But that’s where most investors falter. The momentum of cyclicals going up is so welcoming that a lot of investors get sucked in at the wrong time and price.

Our choice is to invest or not and at a price and time of our choice. But that’s where most investors falter. The momentum of cyclicals going up is so welcoming that a lot of investors get sucked in at the wrong time and price.