Ratings downgrade.

Ceo resign is Big red sign?

2b109890-b73d-4551-9f57-eac6c24eabf9[1].pdf (273.0 KB)

Flat revenue growth and net profit to loss.

They are disposing the retail business of EVOK furniture which should reduce losses in future.

Company will raise ₹205 Cr through rights issue, details of which are not provided at present.

2 Likes

======Aug 2024 results=====

A…HINDWARE

1…Building product

Rev@489 cr

Ebit@26cr

Ebit margin@5.4%

2…Bathware

Rev@326cr

Ebitda@42cr

Opm@12.7%

Pbt@10.4cr

3…plastic pipe

Rev@163cr

Ebitda@10.9cr

Opm@6.7%

Pbt@-4.43cr

4…Condumer

Rev@110cr

Ebitda@3.0cr

Opm@2.7%

Pbt@-6cr

B…CERA

Revenue@547cr

Ebitda@ 92cr

Opm@17%

I have not studied cera but as per screener, cera has 10%-15% revenue from tiles and other items

So if we substract it from total revenue,

547cr-16%=460

Now, lets compare bathware segment of both

1…Hindware

Bathware

Rev@326cr

Ebitda@42cr

Opm@12.7%

2…Cera

Revenue

547cr-16%=460cr

Opm@17%

Is hindware losing its marketshare and opm to cera ??

1 Like

Aug 2024(Q1 2024- Concall)

1…Bathware segment

A…Restructuring

=Q1 was affected due to

A… restructuring and consolidation of sanitary and faucet segments

@25% affected

B…Slow down of market leads to low revenue but fixed cost is there

So ebidta decreased

=In the September quarter, we are not expecting any deterioration in our bathware segment performance because of the sales force restructuring, which we have done in the June quarter.

=That’s a onetime impact we took out, 25% of our off-roll and on-roll manpower at that time. And we believe it had whatever impact it had to have

happened in quarter 1. Quarter 2 will basically be more reflective of the market

.

=Building upon the success of our cost optimization and business streamlining initiatives, we have

deepened synergies between our Bathware and consumer appliances business.

=This collaboration has resulted in improvements in efficiency and cost. Early wins in warehousing,

logistics, marketing and particularly institutional sales channels are promising.

= While the full impact of our back-end integration will be realized in the coming quarters, we are also streamlining our sales force to optimize efforts and expect extremely positive results.

B…Complete insourcing

=Focus is completely to in-source material and provide alternate to imports. This will also help us further garner up the margins, which we had talked about because right now, when we import from China, a lot of margins are left with the vendors in China, which we plan and intend to bring it in-house

2…Pipe segment

=We feel that pipe business has an

ample opportunity to grow

=We have expanded our product portfolio with the successful launch of 24 products for underground drainage systems. Additionally, we are set to introduce high-value offerings such

as Double Wall Corrugated pipes and Fire sprinkler systems by this year end

=We expect 16-18% volume growth and Double digit ebidta growth

3…Consumer segment

A… Restructuring

=Our consumer Appliances business delivered INR111 crore in revenue with an EBITDA of INR3 crore at a 2.7% EBITDA margin reflecting the positive impact of restructuring cost optimization and exiting our loss-making retail furniture business

=What we have done is we are now having a lot of synergies which are shared between Bathware as well as our consumer business in terms of our back end.

B… Exiting from loss making

=We believe that kitchen is our core business. That’s where we

make our margins.

=And currently, there are some categories which are eroding all the margins which we are earning in the kitchen part of the business. So, this evaluation is currently on. Once

the conclusion is done and we make appropriate decisions, take an approval from the Board, I

can share more details to the investors.

4…Restructuring

=So, as an answer to the Bathware business, in the bathware business, we had only one specific objective around merging our faucet business into your sanitaryware business in terms of the

manpower, in terms of the sales force

=We have done that. So, no more restructuring to happen for the bathware business.

= Additionally, what we have done is we are now having a lot of

synergies which are shared between Bathware as well as our consumer business in terms of our back end. So, the marketing, logistics, warehousing, the synergies are coming into both

consumer as well as our Bathware business.

= So that’s already happened now in terms of our execution is done. The benefits will start coming into us in the course of the year.

= We will be evaluating if there are any categories where we would be not making money or we’re losing. So, some evaluation of the categories in our consumer business is an ongoing exercise, which we do. So, if any other restructuring which can happen is around those lines. But for that, I think most of our restructuring has already been done, and the benefits will start coming in the second half of the year.

4…Capex

=new plant will start contributing from Q3 2025

=Other new plant @170-180cr@rokree plant

5…Board has approved raising fund@205 cr

6…Capacity utilization

=Our capacity utilization in Q1 FY25 for sanitaryware was about 86%, and for faucet it was about 58.5%.

7…Expected growth

=We feel on a medium to long-term range we should continue to grow on an average 15% to 18% on sales, and 20% plus on the EBITDA margin.

=next 3, 4 years, we’ll be able to demonstrate 20% CAGR on EBITDA.

Disc…invested

4 Likes

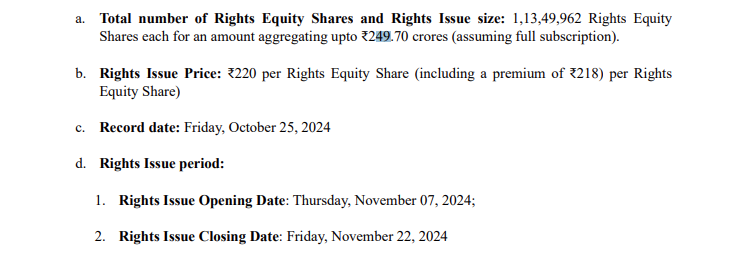

Any news on the proposed rights issue of 250 cr?

Expected ratio and price ?

Should the Slow downward grinding in price be a indication of unfavourable Rights price or ratio ?.

The stock price keep going southwards without any hope for any reversal. Any specific reason attributed for this drastic fall?

I could see LIC children’s MF has taken a position recently along with another FII despite not so good results.

Concall summary . Q2-2025. (nov 2024)

Rev/Ebidta/pbt

1…Bathware @360cr/35cr/3cr

2…pipe@ @187/13/-3

3…Consumer@ 83/-7/-16

1…BUILDING PRODUCTS

=Due to restructuring, sales are affected which is temporary

=We have underperformed in this period with the other competitors(cera) which has declared the results. I don’t think it’s a permanent kind of a loss. I think it’s a temporary blip .

=The reason behind

underperformance is our restructuring process. We deal with 400

distributors and these 400 distributors put the product in the market. The consumer demand from

the outlets remains very similar. However, because of the internal changes of restructuring which we have made, our primary dispatches to these customers have actually got impacted. I personally believe it

would basically be a recovery more sooner than later.

=By the end of the year, we should be very close to the numbers of the competitor in this

financial year

=Unfornunately, restructuring is happening when market condition is not good

=While overall demand remains subdued, we are encouraged by some positive momentum in the faucets category

=We’ve done lots of good work around a Six Sigma project, which basically

has increased what we call our first-time throughput. So first time right, basically, which was operating at about 76%. So if I’m casting 100 pieces, we were getting 76 pieces as the final

output. Now that number has moved from that to about 84-85, so basically 8-odd percentage

improvement.

2…PIPE

= TRUFLO continued strong

volume growth and reported 11% year-on-year increase in H1 FY25.

=We are also diversifying our product offerings, introducing premium high-value products to

meet our evolving customers’ needs. We have launched foam core products for underground

drainage applications this quarter and will introduce double wall corrugated pipes and fire

sprinkler systems in the coming FY25.

=Further, construction of our Roorkee facility is progressing on schedule with plans of its operation by the end of FY25, i.e. Q4FY25

=We had a volume growth of 11% for H1. But value-wise, we were flat because of the down prices of the raw materials

C…CONSUMER

=This business is also affected due to sluggish demand

=Elica’s numbers as well, which is in a similar category in kitchen, which was negative in quarter 2. So that has

impacted our overall margins there

=On a profitability side, we have 1 or 2 more quarters of stress, but we are

very sure that the business will come out good in terms of profitability as well as revenue growth.

=Profitability is our first focus for consumer business

= We have a very healthy margin in the kitchen business. We have a 42%, 43% gross margin in the kitchen business. And we believe that if we focus on that and try to get more

revenue out of that, it will also aid our profitability objective. So that’s where my focus is.

= I’m not going to be focusing on our seasonal businesses as much as I’m going to focus on my kitchen

business

=On a profitability side, we have 1 or 2 more quarters of stress, but we are

very sure that the business will come out good in terms of profitability as well as revenue growth

= So for us, the steps which we have taken is basically we have cut out a lot of our categories, and retail

SKUs where our margins are lower. We are cutting it out on a very aggressive basis

4…RESTRUCTURING

=In our Bathware business we’ve done a bit of restructuring. We have kind of merged our sanitary and faucet teams. And we have also done a bit of restructuring between our Consumer business and Bathware business, where our back-end operations have combined into a single operating

unit. S

=This will increase out profitability

Disc…invested since 3yrs

Seen huge volatility in results and stock price

4 Likes

“Hindware” was (and to an extend is) a very strong brand with deep penetration in Tier 2 and Tier 3 cities.

Sadly, company couldn’t scale up in its core business of Sanitaryware/Bathware. Sales head in verticals keep providing excuses in concalls Qtr after Qtr. They probably need new blood in marketing …revamp their product offerings with new innovative products. Marketing/advertisements strategy is also old style which needs complete revamp.

Lets wait and see.

Disc: Invested.

3 Likes

this space is very much crowded, right from bathware(cera, parryware, jaquar, somanya, kohler, johnson, astral) pipe(astral, apollo, supreme, finolex, prince ashirvad) and many more local brands… its tough to maintain margins and always keep check on dealers… i feel its better to look for other business rather than crowded one’s like these

3 Likes

I think FIIs are continually reducing stake here and the volumes are not great in this counter. This is putting selling pressure on the stock

2 Likes

Meanwhile, the promoters are taking advantage of the recent decline in stock prices to increase their stake.

Acquisition of 125,000 equity shares worth Rs 229.32 lacs by promoter Sandeep Somani

4 Likes

In recent concall investors were seen extremely unhappy about company’s performance as co is losing market share in bathware segment which is its strong fort… One interesting part is Abbakus team hasn’t asked a single question which I found for 1st time in concalls…

5 Likes

this is a very small INR value of 2.29 crore for a company with market cap of 1763 cr of which promoters hold 50%. So it is 2.29/888 *100 = which is 0.25% of the company. I don’t think this is material and the company has 3 and 5 year sales CAGR of 16% and 11% only , with single digit OPM%. Not sure this is a good investment

2 Likes

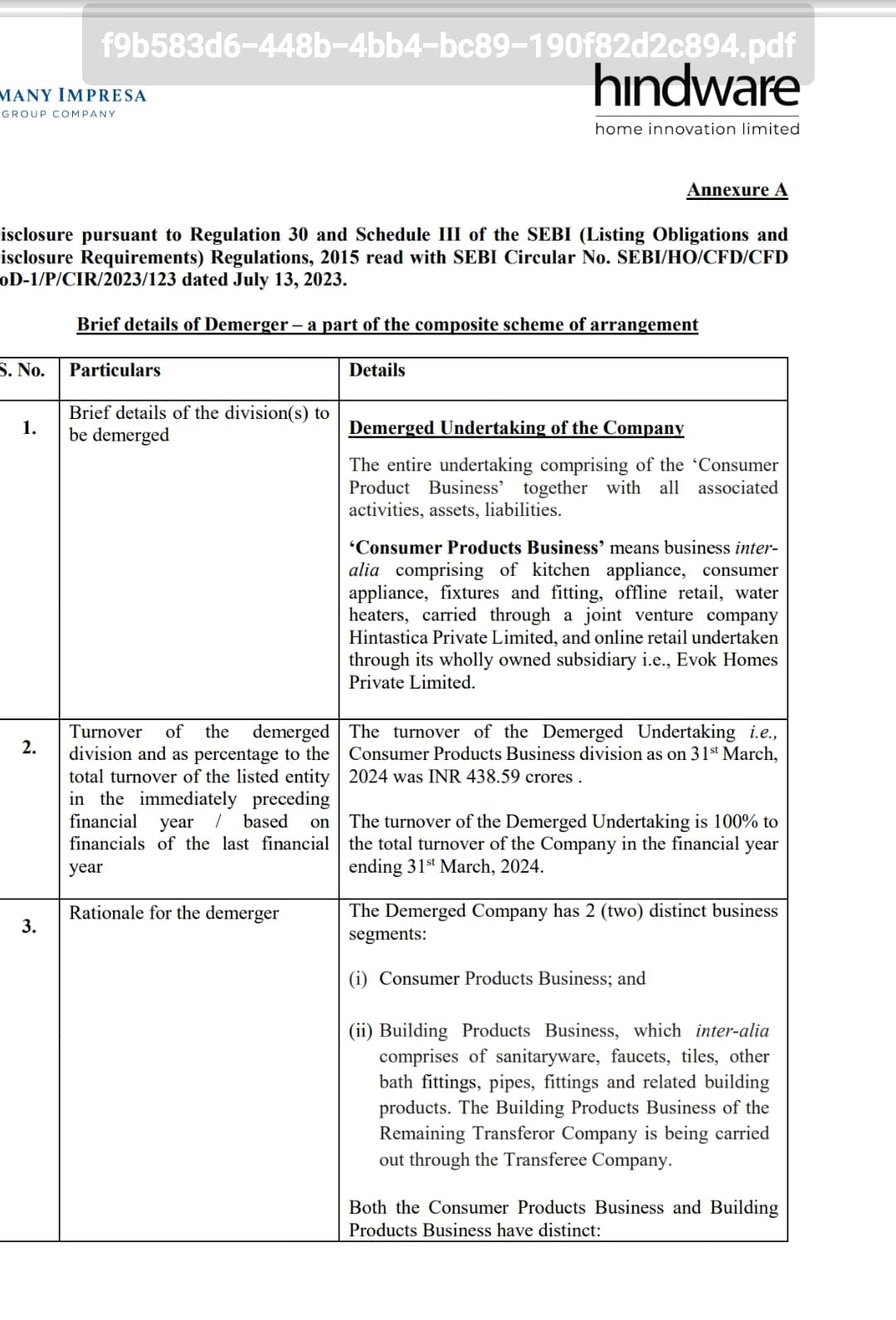

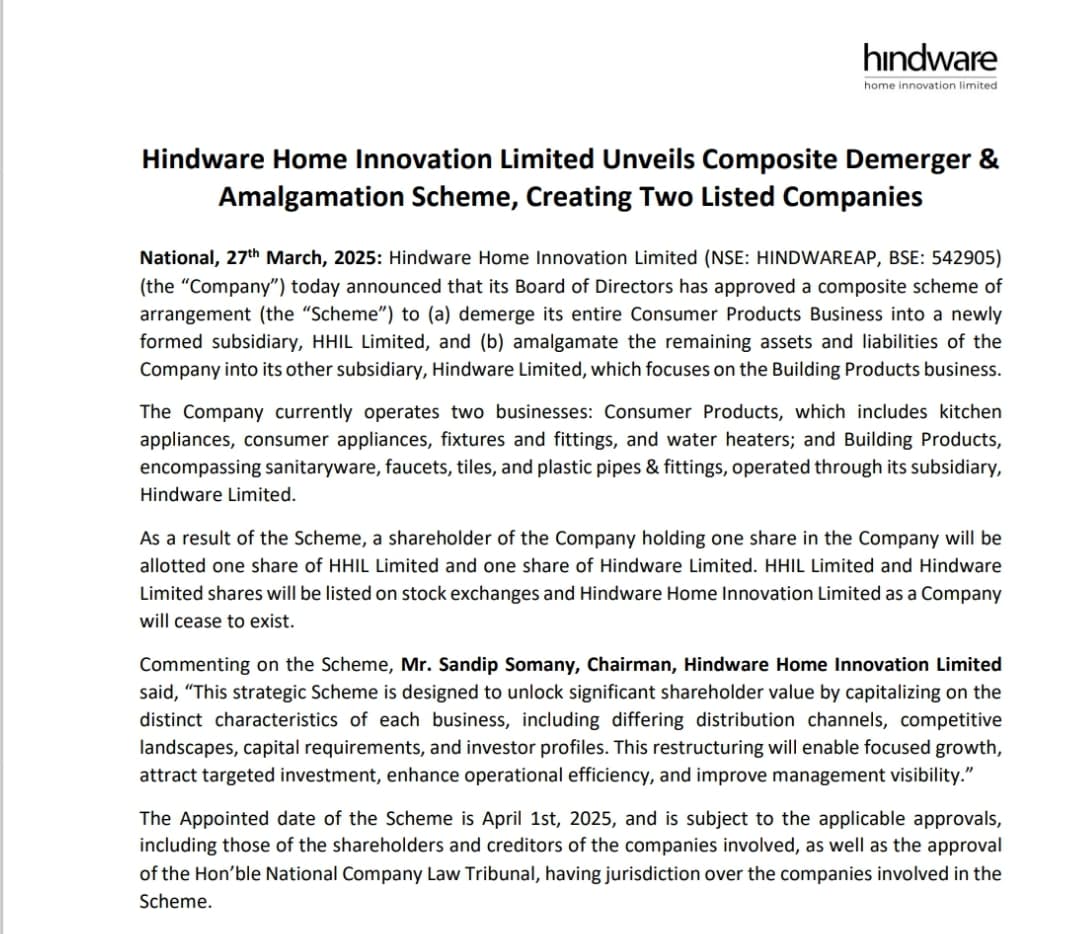

I don’t know how much things will change because of this demerger !

Last year also, they closed and liquidated retail division (evok) and claimed that post this restricting in March 2024, this will be on track and growth is in offing. But nothing like that happened (infact losses kept increasing). And now,batter one year we have another lolipop of demerger.

Actually, hindware has a fundamental problem of very poor and incompetent sales team.Simple talks and dip stick with sanitaryware stores will reveal and confirm the non serious sales team. btw: evok had great quality products at decent price points still they had to close the chain.

Any revival will happen only after deep surgery of their sales and marketing apparatus.

3 Likes