Feb 2024 concall(hindware)

1…Performance

=Despite the challenging macro environment, our performance for the quarter and nine months

has been stable.

=While demand sentiment across categories and regions has been muted, the resilience of our business model and the strength of our brands have enabled us to continue

delivering value.

=We are confident that as the market improves, our performance will further strengthen.

B…pipe

=Despite challenges such as sluggish demand and fluctuating raw material prices on a downward

slide, our quarterly revenue reached at INR174 crores with INR531 crores in nine months FY24.

=Our Q3 EBITDA stood at INR13 crores with a margin of 7.7% and INR45 crores in nine months with a margin at 8.5%

C…Consumer

=Consumers businesses have been facing headwinds since at least last two quarters.

=Our growth was subdued due to muted consumer demand and inflationary concerns.

==============

FUTURE GROWTH

1…New products(bathware segment)

=Customer response to our new offerings continues to remain encouraging as reflected in the

increasing share of new products, which contribute to 24% to our sales in the first nine months for FY24.

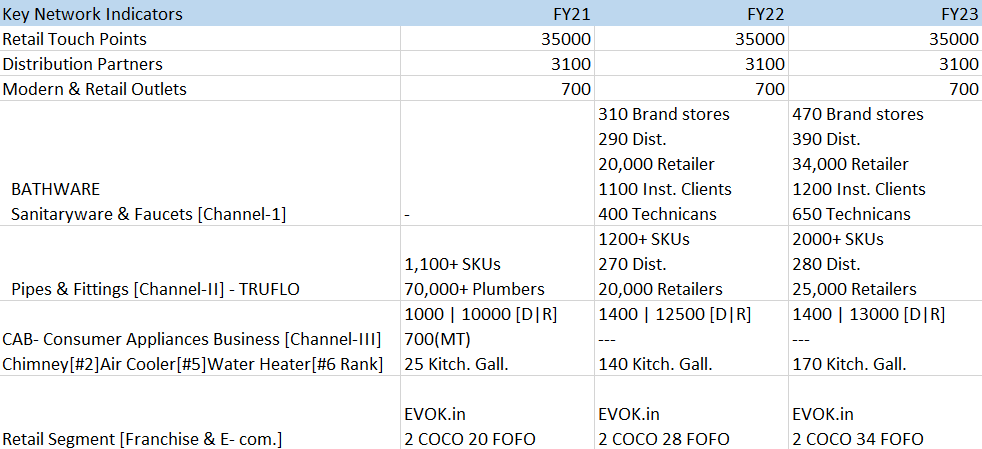

2…Distribution network

=We continue to penetrate new markets, recognize untapped potential in Tier 3 and Tier 4 cities.

=We’re actively expanding our distribution network to broaden our reach.

=Simultaneously, we’re investing in strengthening our presence in Tier 1 and Tier 2 cities by opening more brand stores.

3…Branding and advertising

=Our commitment to enhancing brand visibility remains steadfast.

=We advertised throughout all 48

matches in World Cup during quarter three with an overall expenditure of ~INR7 crores plus.

4…PIPE SEGMENT

A…Roorkee plant

=The construction of our new manufacturing plant in Roorkee, Uttarakhand, is underway, and we

anticipate its operational launch in December of FY24-25, marking a significant milestone in

our journey.

B…New products(pipe segment)

=We are diversifying our product portfolio with our introduction of high value-added items commencing with foam core, that is underground drainage, in Q1 FY25.

=We plan to manufacture double wall corrugated pipes and fittings and also fire sprinkler systems which will go till Q3 FY25.

=Our underground drainage machines have come, there will be

trials, we’ll apply for BIS licenses. And I think in the next Q1, we will be definitely able to sell

these products.

=And the other two categories which is double wall corrugated, the machines have been already

ordered. I think, almost around Q3 of FY 2025, we’ll be installing these machines, and we will

have a direct commercial production, and also fire sprinkler systems which are now gaining lot

of ground, if you have seen recently that the normal conversion from conventional GI piping

systems is now converting to CPVC piping.

=The categories like underground drainage, double wall corrugated, fire sprinklers, column pipe systems have come now on a very higher side from government space, that is huge, Jal Jeevan Mission project, which is going on, which is Prime Minister’s Modi Ji’s dream, Har Ghar Jal, and that’s all HDPE pipe.

C…Growth

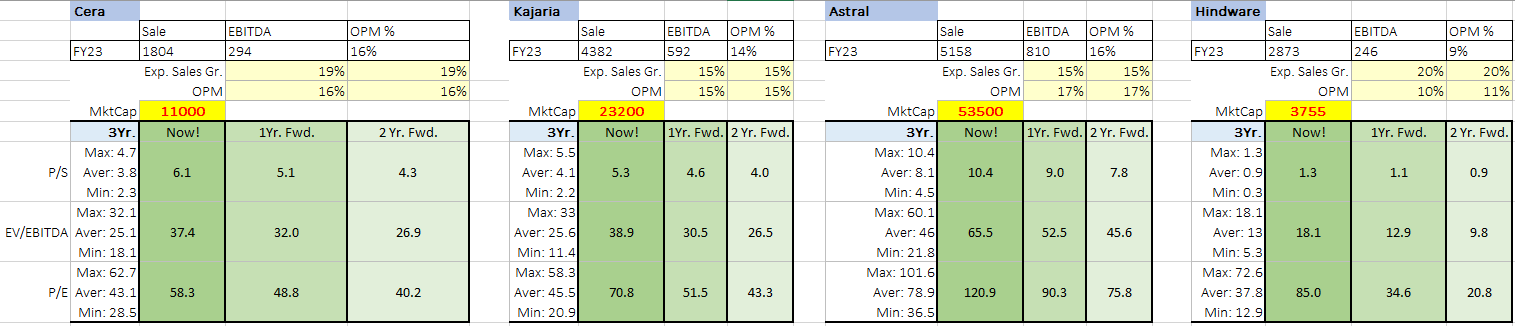

=If you see our YTD growth, that’s almost around more than 11%. This is similar to all the peers.

=We definitely assume a positive cadence of around 15% or more

in the next financial year from the volume growth.

D…Huge opportunity

= Piping sector is a very huge sector. There are around 11 categories of different products where companies are operating. So if we talk about Supreme and Astral, they are into all the 11 categories. We were there into four categories. And we will

be entering into three categories in year FY25. So we will be into seven categories.So pipe segment has huge space to grow.

=when we are talking that we will enter into different categories next year, there will be an

incremental growth which will come from those categories. And all those categories, since they

are new into the Indian market, if you understand because there will be only four or five players

who will be manufacturing, in fact only 3 players that is manufacturing in this category. So the GP margin of those products is on a higher side. We will definitely realize a better EBITDA in

future.

E…Cpvc

=Our market presence remains strong with CPVC pipes and fittings contributing over 40% to our

revenue

F…Network

=Currently, our network includes over 300 active distributors and approximately 30,000 retailers

5…CONSUMER SEGMENT

=Our Kitchen Appliance business remains resilient and continues to grow.

=Our chimneys continue

their dominance on both the online platforms, Flipkart and Amazon. We are number one on

Flipkart and number three, reducing the gap with number two, on Amazon.

=We are actively expanding our portfolio in Kitchen Appliances, adding more products doubling down on the

overall portfolio where we are doing well

Q=When do we see this business once again going to breakeven levels at EBITDA? We have seen a significant amount of time where the growth has also not come, and also the margins have sort of dwindled away.

I understand the overall demand environment, but can you give some estimates by when can we

see breakeven coming in this business? And what kind of growth do we expect in this business

in the next couple of years?

Ans=There are two themes that we are currently working on.

=The first one is our rationalization of the portfolio, where we are doubling down on the kitchen part where we are doing well.

=We’re also exiting some non-performing and low-performing categories so that we can focus the resources on the areas that we are doing well.

=And the second theme is to put the business hygiene in place

where cost, both product as well as operational, is under focus.

= These initiatives should lead

to us getting to the positive EBITDA in a couple of quarters.

6…BATHWARE SEGMENT

A…Competition

Q=In the Bathware segment, what we observed that the peers or even the smaller peers who has ventured out in this business are doing

far better in terms of the growth. And looking at the nine-month numbers, their growth rate is better than ours. So is there a market share shift we are seeing in the Bathware segment?

Ans=We have seen in the last 3-4 years, just about every tile company has got into Bathware segment

in a notional way.

=And to the best of our understanding, none of them have achieved any significant revenue as of now.

=The way the market is structured, we already have some network

and when you place your first product into the market, a primary dispatch happens and revenue

gets booked in the books.

=We have seen many companies, when you do initial revenues, you do it on zero volume, so your

growth look very high. But not many companies have been able to follow up on similar growth.

=So to answer your question, yes, the competition has intensified across sanitaryware and faucet

business because existing tile brands have come into this business.

=However, we don’t believe this business will be a building materials business. We believe this

business will be a consumer business wherein brands are very important and basis the brand consumer buys the product. So I’m sure that we will see consumers coming to the bigger brands over a long-term period.

=So to answer your question, yes, there is competition. We can’t stop competition from happening.

=But yes, have they made a dent? Yes, initially they would have, but we don’t believe in a larger scheme of things, with larger competition in mind, we have lost any share. We have actually

performed better than all the other listed peers as well if you look at their last quarter results or

you know even over the last 8 to 10 quarters, the answers is evident

7…Capex

=Capex in pipe business

Hyderabad plant@350 cr

Uttarakhand plant@100cr(2024)

=We intend to spend INR100 crores of investment in Uttarakhand

because we will be commercially operating this pipe plant by end of December next year.

=So we will be operating with a higher capacity of around 12,500 metric tons per annum. This will again add

up to the sale.

=At the moment what is happening is, pipes only for the agricultural or SWR pipes, we’re not able to sell in these market. We’re only able to sell the other products, because we didn’t have a manufacturing facility. And as the freight part in pipes is so high, you cannot transfer pipes at a larger volume to these places. So once this plant is operational, I’ll come back

to your question, we definitely have a chance to score better than our competitors.

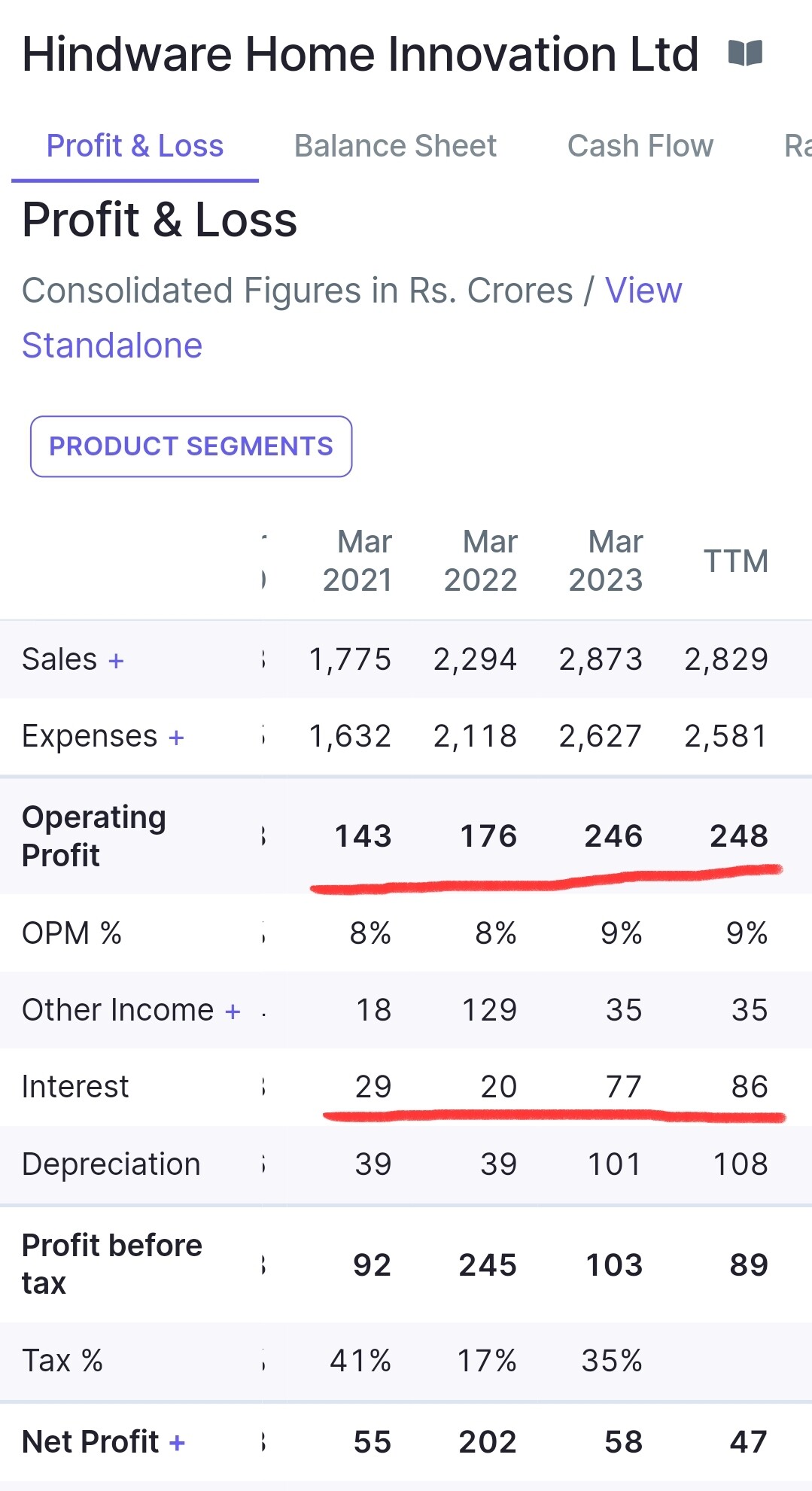

8…Margin

=We have absolutely no issue and I would also like to bring to your notice that for the nine-month period, our EBITDA margins improved by 200 basis points from 13.4% to

15.4%

=But on a nine-month basis, even after doing this extra spend in this quarter, we are 200 basis

point higher. So there is no adverse product mix. There is no margin pressure, in fact, we’re on

track for our localization initiative as well, which is bound to give us further gains as we go forward

=Safe to assume that the 16%, run rate would continue from the coming quarters for Hindware

9…DEBT

Q=Sir, just one last question, especially for Sandeep ji. Sir, we look at now the nine- month

net debt numbers, we are now closing INR1,000 crores, and we were planning to bring this debt

levels down. Definitely, it has gone the other way. So any realistic number in terms of when do

we see this debt level or any sizable correction in this debt numbers because even on the working

capital part as well, we are not seeing any major improvement across categories?

Sandeep Sikka: We had given a sort of a statement at the start of the year that we should be able to run off the

debt by about odd INR100 crores with the profits which we are earning.

=The whole market

momentum has not moved the way we have planned the growth numbers are muted. But in terms

of our EBITDA margin protection, I think we have been able to demonstrate it on the Bathware

side.

= I think give us another two quarters, we should be able to demonstrate on what we talked about

because there is no other exit of the money. Whatever is Hindware earning, actually its being deployed towards reduction of the debt only.

=What I think our investors should bear with us for another quarter or so. Once the market momentum starts growing, the inventory liquidation will

also start happening fast.

=Definitely, there has been some increase in the debt on account of the incremental capex, which

is relating to the pipes because it’s very critical.

=We are looking at a very

aggressive pipe business doing almost INR2,000 crores plus in the next five years for which we

will require some sort of an investment because it’s not a business wherein outsourcing can

happen. Rajesh has spoken about entering into newer categories around the core product. We feel, give us one or two quarters, I think some level of debt should come down, but most of the debt which we are now contracting is for a long-term growth. Had we not taken Roorkee plant, then that quantum of money would have definitely come down also.

10…Negative ebidta in pipe and consumer business

Q=In the first nine months, on a consolidated basis, we’ve done INR91 crores PBT in the Bathware business, but overall consol

PBT is INR 30 crores.

=Actually, we’re losing some INR 31 crores in the other businesses. So I

guess the question was, we had around INR32 crores loss in the Consumer Appliance business

also in the nine months.

= So any internal guidance or aim you have, what kind of ideal EBITDA

margins and net margins you are aiming for in the, one, pipe business, and two, in the consumer

appliances?

=Because as a shareholder, if I look at it on a INR2,000 crores revenue, our net margin is only 1.5%. So how do we move up this goal of EBITDA margin and net margin going forward?

Ans=

A…Pipe

=The fixed cost structure for pipes is still high. And as the volume builds up,this fixed cost wull come down.

=There, we have already given a

double-digit 10% to 12% EBITDA coming through in the next 18, 24 months with all the investments which we are doing.

B…Consumer

=We are doubling down on the kitchen part where we are doing well.

=We’re also exiting some non-performing and low-performing categories so that we can focus the resources on the areas that we are doing well.

=On the consumer side, I feel another two or three quarters will be required in terms of rationalizing the whole things, and we should be back to the market the way we were around 1.5

years back.

= Right now, this business is facing an extreme headwind not only for us, when you see the competitors and the peers also, a similar sort of numbers are coming from there also.

=But good part is that we have a core kitchen business today, which is now the focus area. And we

are working on a strategy. given the fact that we are in this business for almost eight years now

and we are charting the path that in next three quarters ,we should make it a profitable business

11…Growth and ebidta guidance

= I think from our side, we have built a robust business model. We have the first-mover advantage. The rest of the players are now experimenting in the

market in terms of expanding the horizon for the brand.

=We feel that we should be able to

continue our growth trajectory somewhere in the range of 15% to 17%. And what I’m talking is not immediate quarters, but I’m talking a trajectory of say 2 to 3 years CAGR.

=If you see it on a combined basis over the next 24 months, our ebidta should be in the range of around 13% to 14%…

12… your kitchen appliances business contribute what percentage of total Consumer Appliance business?

Salil Kappoor: 60% to 65%.

13…if you look at its segment-wise, we’ve also seen a huge buoyancy also in the upper part of the segment.

14…As per management, they see an extremely positive market sentiment as we go forward, be it on the top line, be it on the way the margins are structured right now.

Disc…invested