Hi was studying Hindustan Zinc as a dividend play. Enclosing a ppt of the same. The key findings are summarised below:

HZL is one of the largest zinc-lead producers globally and largest in India. 10th largest silver producer globally. It enjoys strong free cash flows, is debt free, strong profitability and high ROEs. It is also amongst the lowest cost producers and has transitioned to underground mining from open cast mining.

Historically a PSU, but acquired in FY03 by the Vedanta group who subsequently expanded zinc capacity from 0.2 mtpa to 1 mtpa currently. Promoter holding is ~65%

It operates in a commodity business. Commodities are cyclical and dependent on demand-supply. Zinc (~75% of PBIT profits in FY19) is turning into surplus from 2022 (deficit in 2016). International zinc LME prices (USD per tonne) have softened by 35% to ~ USD 2,343 currently from the peak prices of USD 3606 in Jan 2018

Share returns since Jan 2011 have been impressive with aggregate returns of 550%; however, returns have been cyclical. Currently share price has fallen to Rs 215 per share from ~ Rs 325 in March 2018.

At current valuations, the stock is trading at mid-point of historical P/BV levels and higher range of EV/EBITDA valuations. Given that zinc prices are likely to remain volatile with a downward bias, further share price correction is possible.

HZL dividends have sharply risen since FY16 when its cash & cash equivalents were Rs 352.7 bn. Cash balances as on March 2019 are Rs 169.5 bn. Recent dividend payout in FY19 was Rs 20 per share or ~ 9% dividend yield.

Rationale for dividend payout in the past includes paying off debt to group parent companies (Vedanta Resources and Volcan Investments). This may continue in the future and provide dividend income to investors in the interim, but could come at a risk of initial investment in the medium term.

In my opinion, silver manufactured by Hind Iznc is kind of By product from

Lead, particularly from one mine(Zaver if my memory is correct). While value realisation for silver is high, production is also fraction of lead produced. Hence, key monitorable for Hind Zinc would be zinc and lead price followed by silver price in my view. In last 3-4 years, company has constantly trying to improve product mix in favour of silver which kind of work as negatively correlated to other metals. So in downturn, silver would contribute to slow down in decline in profit, but in upturn zinc and lead has to see price improvement for material jump in earning of HIndustan zinc in my limited understanding.

Discl: Hold token tracking position. Not a SEBI registered analyst, my view may be biased. Not recommending the investment in the company

In the event of COVID as the doctors prescribing more intake of zinc Vitamin -C &D supplement so based on this hypothesis the pharma usage of zinc may be rising . This will give push to price and Hindustan zinc margins will improve but at the same time the promotor group is not so ethical and is not minority friendly we have seen this happened in Vedanta . Both the views are contradicting so How one should be investing in this scrip ? Could some one help me to clear confusion …

Regards

I would consider increase share of silver in EBIT as against zinc and lead as a main factor for major price increase as against increased demand of zinc for medical purpose. The volume demand would hardly 100 tonn as against ~8,00,000 tonne which being total annual zinc production of HZL.

On second point about Vedanta Past conduct, market knows that since Sterlite delisting in 2000 To Cairn merger. So what would surprise market could be on positive price. We also need to notE that GOI is major equity holder and also have board representation. While in past GOI has not raised any major issue, but raising debt in HZL to fund delisting of Vedanata (as mentioned in media report) shall get major resistance from the non promoter holder including GOI. But I believe most likely way the deal would structure would to raise debt and pay dividend to shareholder. In my view, such deal shall be equally treating all stakeholder and hence shall be fine.

On long term, GOI divestment of residual holding would also trigger takeover code and hence purchase from other minority shareholder. One shall consider valuation and other business prospect at that time, if such opportunity arise.

On the Q1 con call, when question where asked for planned debt raising during FY21, management avoided that question. So everyone is concerned about bad corporate governance and I believe same in price. Now what market is looking at HZL as silver proxy till silver prices are reaching new high. HZL is India largest silver producer and sixth largest global player. During Q1, EBIT of silver was higher than zinc which was never being the case in company history.

Above are my understanding and it may be wrong. I am not an expert on Zinc or silver metal which is critical to evaluate HZL.

Discl: Have added small quantity in April for tracking. Not recommending investment. Not a sebi registered advisor,

Looks like the price movement in underlying commodity is not affecting the stock.

With high energy prices in Europe, we should see demand outstripping the production for Zinc for couple of years. The inventory levels at LME is at cyclical lows and we will witnesses frequent price spikes in the medium term.

Disc: HindZinc is c.4% of the portfolio and the views might be biased.

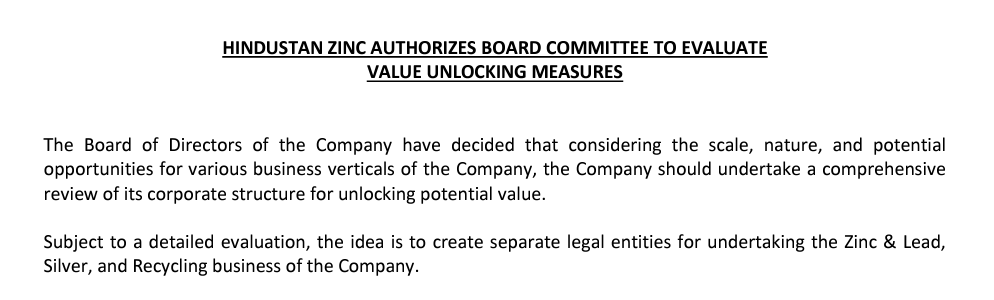

HZL notifies Stock Exchanges about potential demerger of core businesses. Will be interesting to see GoI’s take on restructuring considering that GoI did not approve the earlier intiative of acquisition of Vedanta’s overseas mines. This is different and may help ascribe loans to resepctive businessess , which is a key element in the entire Vedanta Group.

Demerger proposal was to be submitted for Board’s approval in Nov’23 which has not happened. A lackluster performance for the stock in this over charged bull market.

Decent production growth seen in Q3 which should get reflected in the results in Q3 & Q4 with zinc prices back on rise and silver holding the ground firmly for a takeoff soon.

Betting on its immense potentials for sustained growth for many years to come…

Q3 Results downplays the cash crunch company is going through thanks to the liberal dividends paid to benefit Vedanta.

Burgeoning interest cost and negative working capital combined with poor sentiments prevailing in metal prices will have more adverse impacts on the stock.

I don’t expect fancy dividends to continue in the near future until the cash position improves considerably.

Hindustan Zinc has now become the 3rd largest* silver producer globally as per the World Silver Survey 2024 conducted by ‘The Silver Institute’, USA. The company’s Sindesar Khurd Mine now stands as the world’s 2nd largest silver-producing mine moving up from last year’s 4th position.

Hopefully the results tomorrow will reflect silver uptick - both in quantity and market price