I like Hindustan zinc as an investment idea with medium term horizon of 2-3 years for following reasons:

1) Global favourable Demand supply balance:

April 2017 Forecast pdf file.

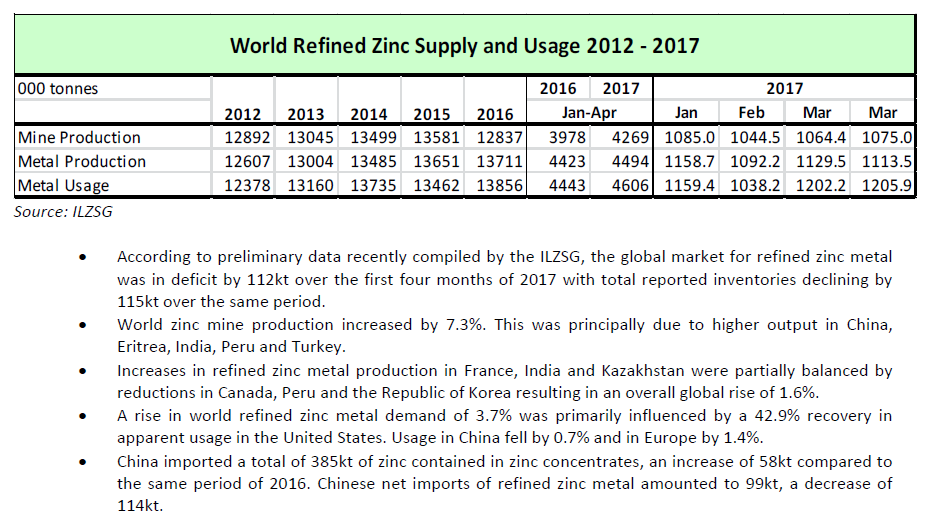

The revelant extract from Page 3 on global Zinc Demand supply

“Regarding the global market balance, despite the expected increase in zinc mine

supply the Group continues to anticipate that global demand for refined zinc metal

will comfortably exceed supply in 2017. The extent of the deficit is forecast at

226,000 tonnes.”

Global Lead Demand supply

World Refined Lead Metal Balance

“Having taken into account all of the information received from its member countries

in recent weeks, the Group anticipates that there will be a close balance between

global refined lead metal supply and demand in 2017 and that reported inventory

levels of refined lead metal will therefore remain at a level similar to their current

total.”

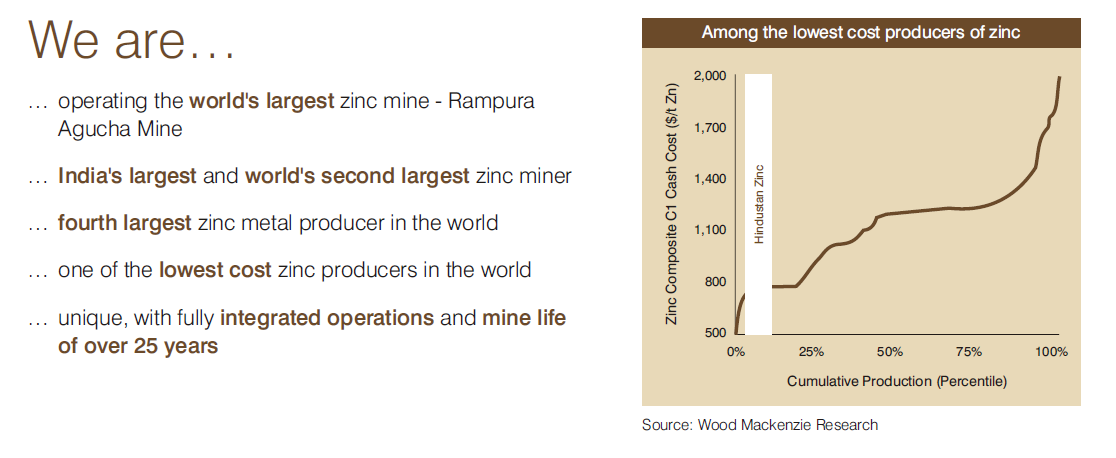

2) Cost competiive player with Global scale of operation, Captive largest mine with among best quality ore strengthening position

3) Superior quality of Ore

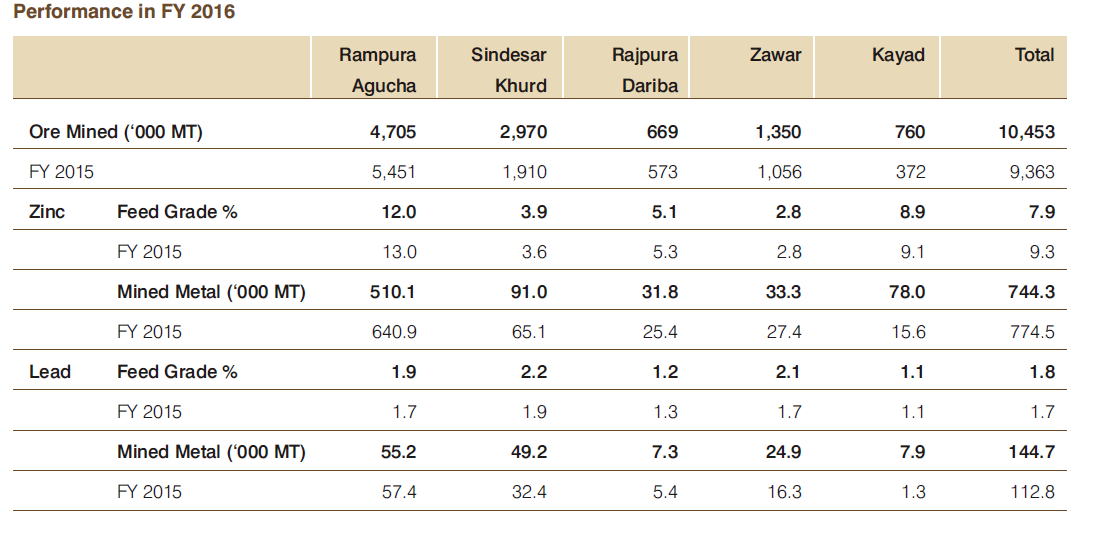

Hindustan Zinc Mine production data from FY16 annual report

Average Feed grade is 7.9% for Zinc during FY16.

However, same for peer being around 4.25% for Zinc over CY14-16 period as shown in slide 11 of enclosed persentation.

https://www.trevali.com/site/assets/files/2206/trevalipresentation.pdf

Please note that I am not mining expert and also possiblity of selective information bias in presented information. My access is limited to google search and it may be possible that there might some suprior peer with feed grade better than Hindustan Zinc.

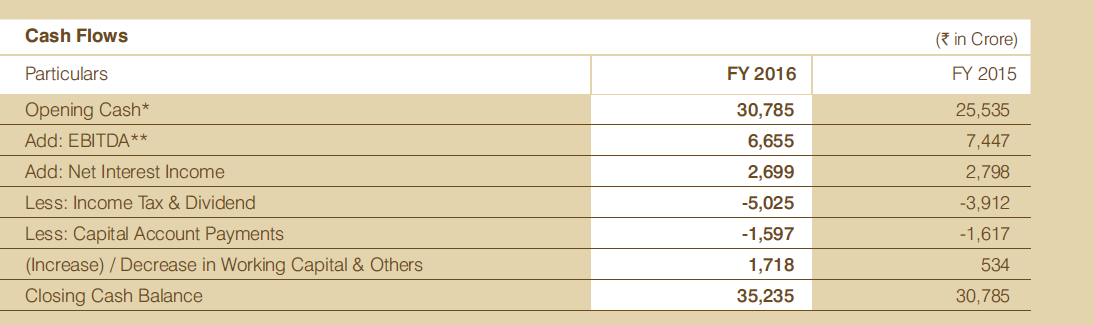

4) Superior Cashflow generating business:

The company can generate EBITDA of around Rs 7,000 Cr of with expected Capex of around Rs 2,500 Cr for proposed expansion, giving free cash flow of around Rs 4,500 Cr. This is without considering any benefit of capex and price increase in Zinc. Assuming same being distributed, the company can easily declare divided of Rs 10 per share (Equity capital of Rs 845 Cr with face value of Rs 2 per share). At current market price of around 240, same give dividend yield of ~4%. We are not taking into consideration Rs 16,000 Cr worth of liquid investment on company balance sheet as on March 31 2017.

Financial

Market Cap.: ₹ 98,175.29 Cr.

Current Price: ₹ 232.35

Book Value: ₹ 108.16

Stock P/E: 11.81

Dividend Yield: 11.96%

52 Week High/Low: ₹ 333.20 / ₹ 164.40

Return on capital employed preceding year: 66.47%

EVEBITDA: 8.03

http://www.screener.in/company/HINDZINC/

KEY RISKS

- Vedanta group holding the largest stake with around 65% stake with nearly 30% being held by Govt of India. Vedanta has first right of refusal when GOI decide to divest the balance stake in the company. In case GOI divest the stake, the company would be fully controlled by Vedanta group, which is past have not treated minority sharheolder fairly on various occassions. However, at the time of divestment, the minority shareholder also can expect open offer. Current management of the company is under control due to GOI representation on the Board.

- Decline in Zinc demand/price at LME and/or rupee appreication may signficantly affect cashflow generating ability of the company.

- High regional concentration of mines in Rajasthan State, Udaipur district. Most of Ore for zinc and lead is mined in Udaipur district. Any problem like earthquake, flood or riots in the region can majorly hurdle company performance

- Enviorment issue: The mining and smelting of zinc is not very environment friendly and hence may face issue from Ministry of enviorment in future.

Disclosure: The company is among my Top 6 holding. Investor are advised to do their own due diligence before making any investment. My view may be biased due to my investment and also limited understanding of sector and company.