this 11% div yield is very confusing

Above extract from my post porabably address your dividend yield issue.

1 Like

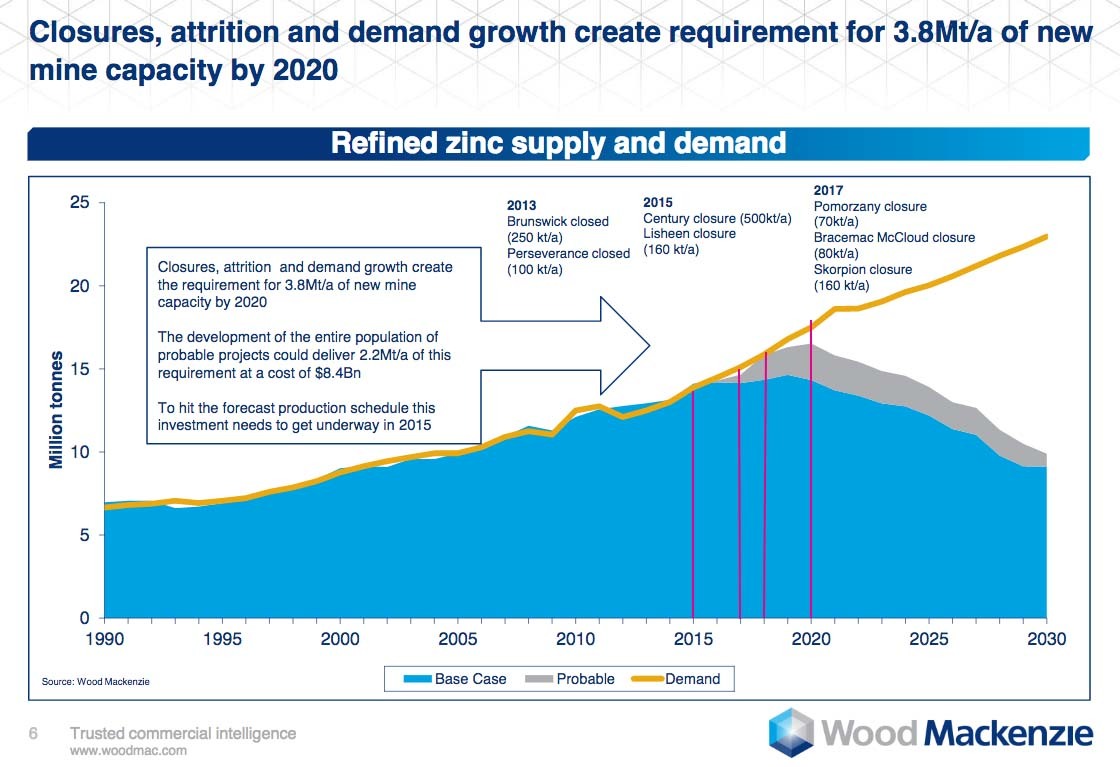

According to the report mentioned by @dd1474 after 2018 the demand for zinc will always be more than supply till 2030.

I am trying to find more this seems too comfortable to be true.

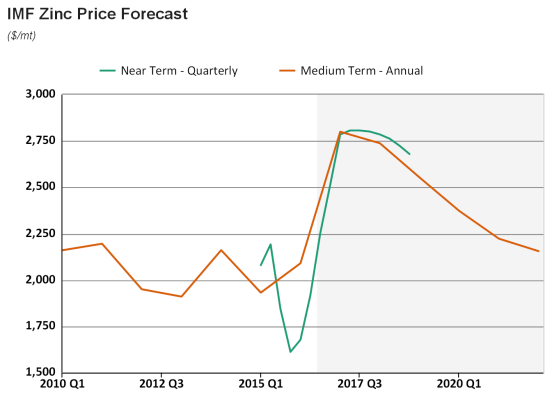

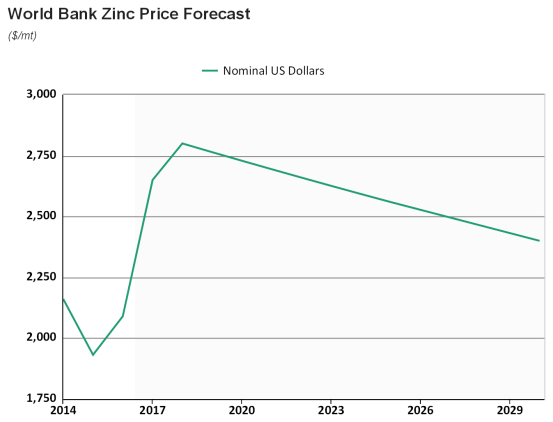

Here below we have Zinc price forecast by World Bank & IMF which in sharp contrast to the above report are predicting a downfall in prices over the long-term.

How can demand outstrip supply by wide margin and at the same time price fall?

3 Likes

Here’s another question to ask: Why would the global biggies (Glencore et al) close their mines and cut production if the demand is higher than supply? These were voluntary closures / production cuts to stem the Zinc price decline.

This report is from March 2015 prior to China market crash…and a terribly confusing one at that. Why would there be “restricted supply”, “lower capex” etc. if there’s “strong demand growth”? Are we running out of Zinc on Earth? Why wouldn’t supply grow to meet the demand?

One final question to ask is “What is the minimum price at which Zinc production would be viable for global miners in 2017? Are we above or below that price point?”

There’s no question that Hindustan Zinc is a great cash generating business. But I doubt Zinc metal prices will remain high for long.

1 Like

If you look at forecast of IMF and World Bank, very rarely they would project steep price movement, which is rarely the case. Anyway, it is a view of reputed interenational body and one shall give due respect to same. I am not saying that Wood Meckensie knows every thing. However, they are supposed to be expert in information compilation in this industry. If you look at Glencore, Hindustan Zinc or other international player, most of them represent Wood Mecknesie data on cost strucutre, scale of operation of smelter and mines.

Having said that, commodities are risky business and tendency to make expert an idiot time and again. Hence, I just presented data point with source mentioned. What would happen in future would be known only time unfold.

I see many positive factor for medium term, mainly limited cashflow of players, inferior quality of mines, reducing supply and cost and recovery in world economy growth, with declining inventory supply in world (during 2015 and 2016 also there was deficit but same was met from inventory stock due to which price movement was steep as per my understanding gained from various public domain information.). On negative/uncertain side is China factor, as in most of commodities. However, China has limited mine supply vis smelter in global market and quality of mine is also inferior which add significant comfort to zinc prospect in my opinion.

Finally, all these known to market and probable same be discounted in price as assumed in efficient market. So best is to do once homework and check risk profile and take final call.

1 Like

Glencore closure of capacity was due to lower price affecting viablity. However, in addition to Glencore, there were two significant mine in Australia and Ireland closed which were more kind of natural phenomena in my opinion. Glencore supply reduce by 4,50,000 tonnes while mine closure was also around 500,000 tonnes production per annum. Even Wood Mackenzie forecast consider Glencore increased supply at higher price as a major determent to spurt in price. So point well taken.

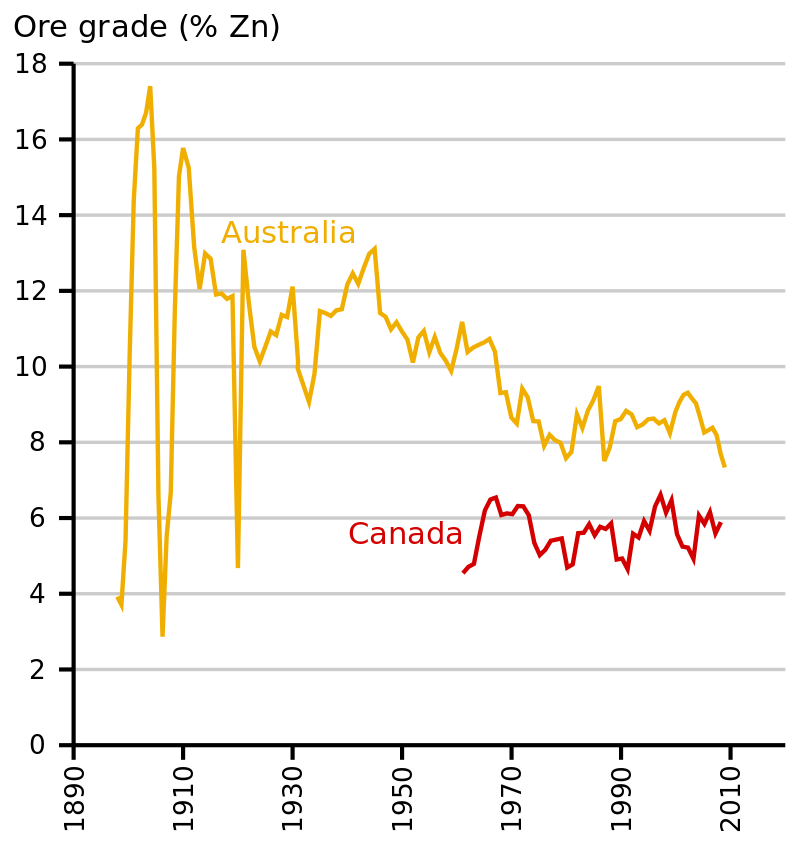

On second point, very limited authenticate information one can get from China. However, deteriorating quality of zinc ore is natural phenomea which happen across the commodities but most severe in Zinc among top 5 metals. Find enclosed graph of deteriroating quality of zinc mine ore from Australia and Canada.

Source: Zinc mining - Wikipedia

This is more strcutural change and would impact higher cost and hence increase equlilibirum price then resulting in year to year flcutuation in the price.

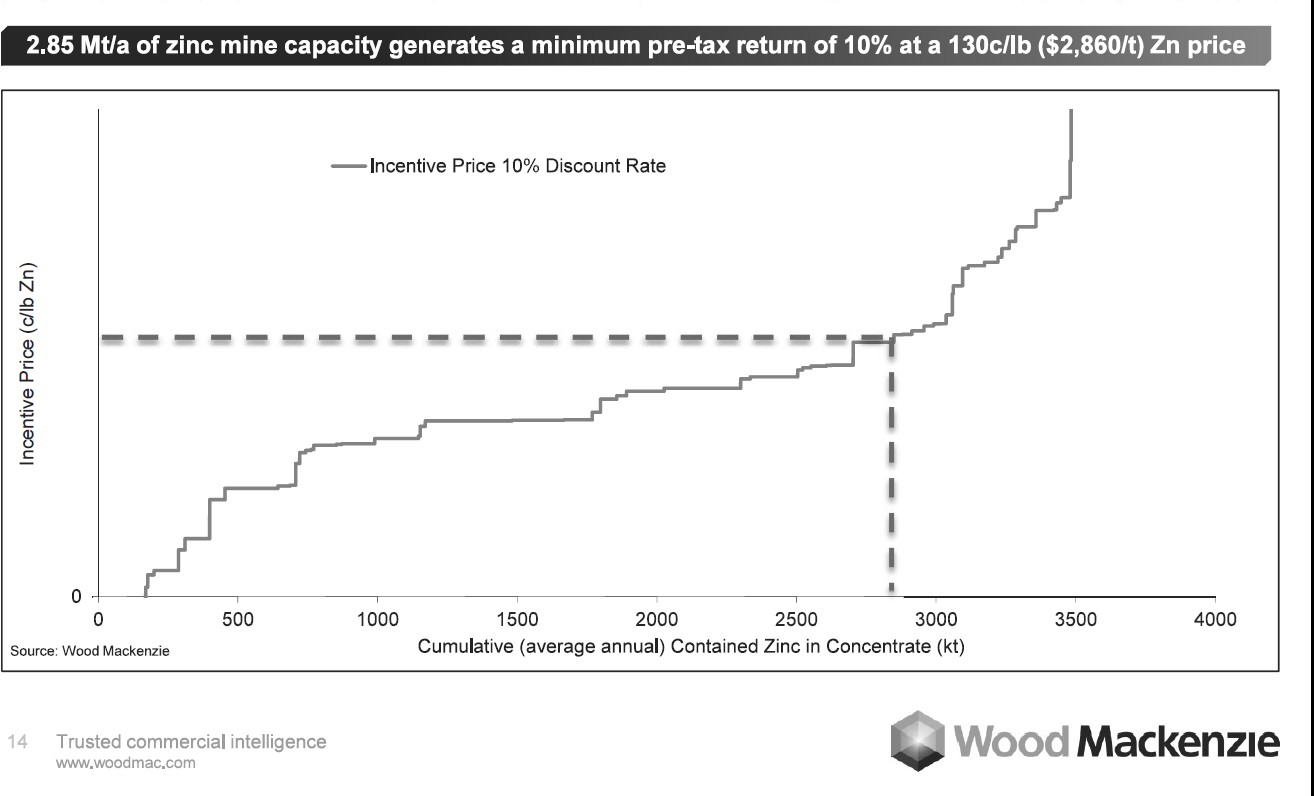

Wood Mecknzie attempting to answer your query with following slide 14 with 10% discount rate. Whether the long term return for Zinc shall be 10%, 5% or 25% and what are basis for assumption are still not answered.

Thanks for you valuable input.

2 Likes

Can you please provide details about free cashflow of Rs 32350 Cr. I belive what you are refering to is cash and liquid invesment which have been accumulated from the company profit over the period. I have given my working of free cashflow as enclosed.[quote=“dd1474, post:15, topic:5003”]

The company can generate EBITDA of around Rs 7,000 Cr of with expected Capex of around Rs 2,500 Cr for proposed expansion, giving free cash flow of around Rs 4,500 Cr. This is without considering any benefit of capex and price increase in Zinc. Assuming same being distributed, the company can easily declare divided of Rs 10 per share (Equity capital of Rs 845 Cr with face value of Rs 2 per share). At current market price of around 240, same give dividend yield of ~4%. We are not taking into consideration Rs 16,000 Cr worth of liquid investment on company balance sheet as on March 31 2017

[/quote]

@dd1474 You have simply discarded World Bank & IMF prediction. So be it, for the time being.

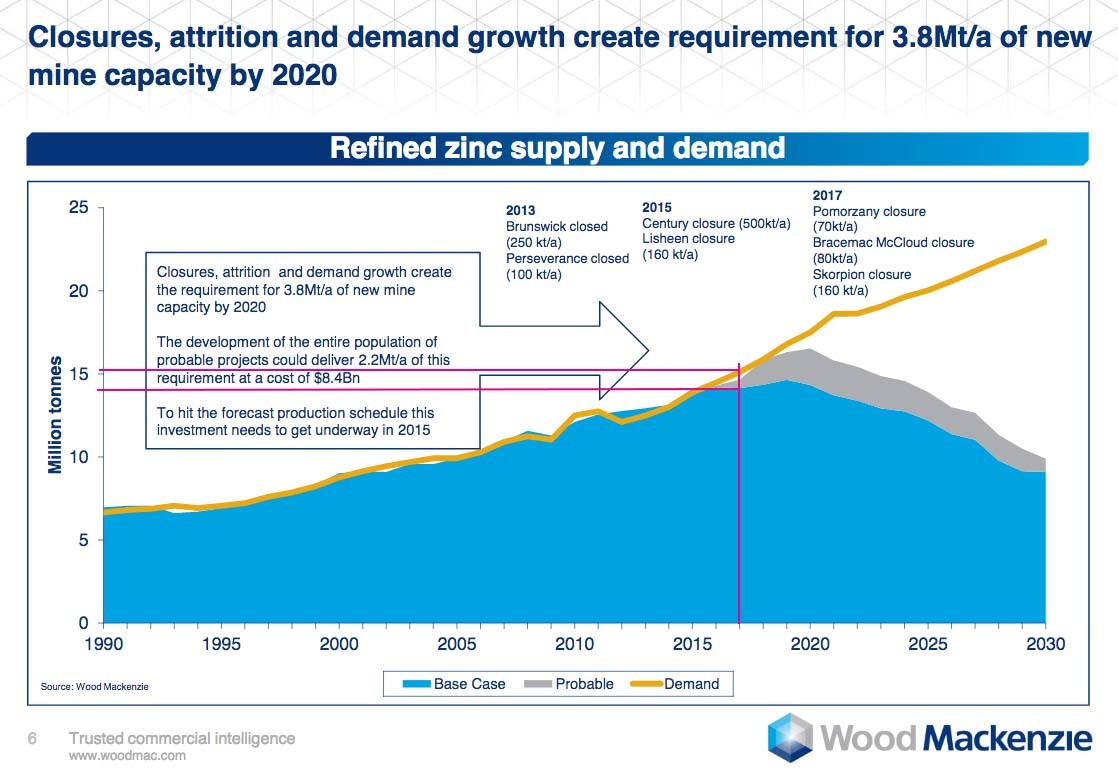

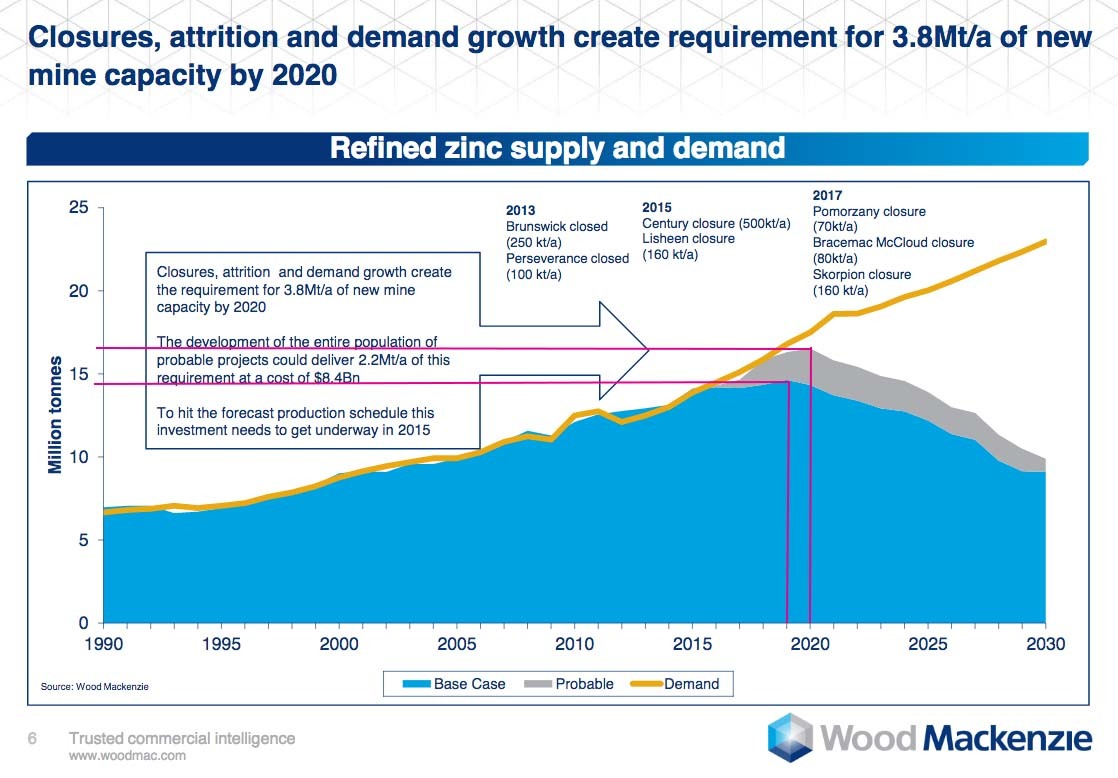

According to above graph the shortfall for 2017 for refined zinc should be around 1 million ton.

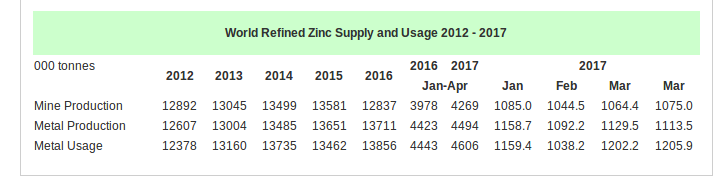

The latest data available from ILZSG infact points to a shortfall in refined zinc but to the tune of 112k ton for Jan-Apr (4 month peroid) which translates to a 2017 shortfall of 336k ton way short than prediction.

Source - International Lead and Zinc Study Group

Also, I am also surprised by sharp demand-supply mismatch predicted by 2019 at 14.5 million ton or 16.5 million ton in 2020 (refined zinc) and subsequent downfall continuous downfall in refined zinc production shown below

How can we corroborate such prediction with data?

1 Like

I have never said that discard World bank and IMF Projections. What I am saying is that their projection generally have tendancy to be range bound and ignore steep price movement which is generally a nature of commodity business. For instnace, World Bank latest June 2017 forecast Zinc CY2017 price is around USD 2,750 and CY 2018 is USD 2,600 per tonne. Please note that there is no supporting demand supply projection which are most critical for price projection in my understanding. Wood Mackenzie Data, whaterver it may say, at least provide infromation about likely demand and supply with some player major action about new capacity and closure of capacity. That is the reason to I find easier to work with Wood Mackensie Data.

Second part of demand shortfall of 1 mn tonne, I believe is based on base case. In case we add probable case, demand supply gap would be in line with ISG study (this figure are also provisional which would undergo change). Also, please note that the projecton were done in 2015 and data is old. The latest information would be paid service and I am not subscribing. I am taking decision in that constraint which I am aware.

On last part of major shortfall in supply in long term, over a period, with increase in price, we would see market would also react with using substitute wherever possible. Further, these all model assume China demand to continue to grow at 6-7% p.a. even at $ 4,000 per tonne price. There would be definitely resistance and subsitution and also increase recylcing which shall take care of very long term demand supply situation.

Having said that, there would always be uncertaininty and contradicting data points in market. One need to understand all data points/information and take his/her own investment decision. For all we know, there is all of sudden major financial problem in China and whole projection undergo drastic change with surplus zinc supply vis deficit which we are projecting in Second half 2017 itself.

I am not all expert and do not want anyone to believe and invest based on my feel. I find Hinudstan Zinc a good opprotunity to invest for me and not necessarily good for every one.

About how we corrborate such prediction with data, one has to take his/her own call and develop conviction to buy/sale or ignore. I do not have any answer to that question as even I am searching for answer to this question.

1 Like

The Zinc grade mined is a function of in-situ grade and price. We can not look at ore grades in isolation without looking at the costs and prices. For example, in respect of Gold, a price forecast of 1200$/Oz may force the miner to set the cut-off grade at 4grams/ton and a 1800$/Oz forecast gold price may lower the cut-off grade to 2.5G/T. It is all a function of economics.

Also, we must remember that we can not be sure that higher grade ores can not be found in the future. Exploration activities pick up when prices rule high and higher grade resources could be found in the process.

2 Likes

@reddygvsb

Thanks for your input. However the mute point is to

Have higher price which shall make sense and increase interest for miner as well as smelter to invest in the company. Please refer to wood Meckensie presentation which does indicate some price level which would make business attractive. Also limited free cashflow for decade before 2007 were the main reason for limited activity. If price increase which are attractive to even for low quality ore, that is more attractive for Hindutann zinc. About the prospect of future of good quality mine, definitely possible but currently nothing can be said. Anyway in order to get supply in 2018, it required at least 3-4 years. Hence, in next 2-4 years, probabilty of deficit situation has high chance vis balance in my opinion.

Rest, I have already given my disclaimer in previous message that what is good for me may not be best for everyone. Thanks once again for bringing another perspective on the thread

2 Likes

2 Likes

@dd1474 Do you know any global investors (not just analysts) bullish on Zinc metal? Any funds piling into Hindustan Zinc or global Zinc companies of late? I know Zinc rallied on funds’ buying in 2016. I am trying to find out if there’s anybody with lots of money that continues to buy, agreeing with our assessment of declining supply of Zinc.

(For example, Mark Mobius thinks that iron ore fundamentals and prices are diverging. That gives me some reassurance that I am not alone when buying NMDC.)

The inventory situation definitely supports the shortfall thesis in the near term. What happens if Glencore / China mines suddenly start pumping more Zinc? I am always comfortable investing when current commodity prices aren’t viable for producers…but hesitate to invest based on future shortfall scenarios. Stories of world running out of non-recyclable (oil) and recyclable commodities (metals) aren’t new.

4 Likes

Appreciate your view point and generally I try to develop my conviction and invest and like counterpoint for unbiased friends like you to confirm the hypothesis. So I have neither any idea of fund/investor nor I consider it material to my investment decision making process.

I appreciate your view on point about not investing future shortfall based forecast. However, I have different apporach to same. I am not saying that Zinc would run out of ore very soon. My limited point is current demand supply situation, limited cashflow of existing players (inferred from Wood Mecknsie presentation), increase action from new player then old players in expansion, and declining inventory across from chain/across the region give me comfort about expected increase in Zinc price in 12-18 months. Further, superior scale and cost comeptitiveness of Hind Zinc along with unique requirement of two large shareholders for distribution of cash as dividend, fits my check list of investment for 18-24 months. Please note that in case I see major increase in Chinease supply or decline in demand, I may immediate change my view and sell my holding.

Thanks for making these discussion more interesting and providing valid counterpoints. Do look forward to more such meaningful counter argument against my hypothesis of higher zinc price.

5 Likes

thanks for explaining

At the higher level, I have just added the (CFO - Capex) for approx last 10 years, to get an idea as to how much cash the company was able to generate long term solely based on operations. Investments and Dividends have not been considered.

Does this answer your question?

I am invested in Hindustan Zinc since 160-170 levels. Its very tough to build conviction in commodity based stocks for someone like me who has limited knowledge about commodity markets.

My view is Hindustan Zinc is a long term hold and you will have to ignore the short term zinc price movements. 2 major reasons why its a good hold for long term -

-

Hind Zinc is one of the cheapest zinc producer , this basically means in case zinc prices come down , Hind Zinc mines will still be feasible cost wise. This is a big positive

-

Hind Zinc has been a cash cow. Even if you may not see great CAGR , its generating good cash and dividends will keep coming in. So dont expect multibagger kind of returns , but with good cash in the books problems like high debt will never come along.

To sum it up , try to hold it for a time period of 7-10 years. You may actually get to hold it for free given the good dividends that come.

5 Likes

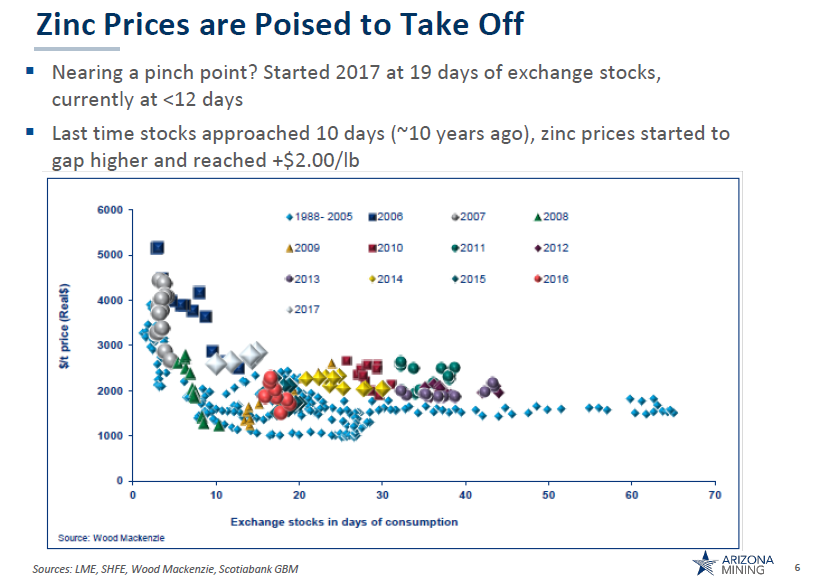

Find enclosed another useful presenation by a miner in July 2017.

https://www.arizonamining.com/_resources/presentations/Arizona-Mining-Corporate-Presentation.pdf

Refer to Slide 42 onwards for latest demand supply forecast and sector view.

In Slide 43, it interesting provide details of minewise new addition and closure. The projection include decline in supply from Ramapura Agucha mine while increase supply from Zawar and Sindesar Khud. However, as per Hindustan Zinc management view, they are likely to report stable production of Ramapura Agucha Mine as per my understanding. At least to extent this projection has conflicting for Hindustan Zinc. Further, if Hindustan Zinc continue supply, what happen to price projection would need to be consider. In that scenario, mostly price would be lower than projected, unless there is major unexpected decline from other existing facility.

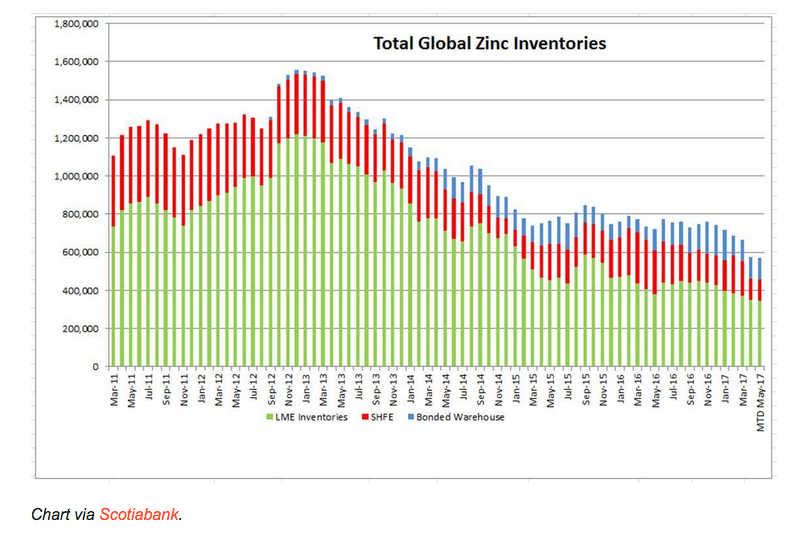

Refer to Slide 6 about invetory and price relationship over the years and graph. I find this very useful.

{kind=link}

Nevertheless, very interesting insight on sector and likely profatibility of new mine.

Discl: My view may be biased due to my holding in Hindustan Zinc.

4 Likes

Recent May 2017 release from Internationl Leand and Zinc Supply group give positive news for Zinc and lead sector:

http://www.ilzsg.org/generic/pages/file.aspx?file_id=2066 (Open ILSG July2017. pdf file)

Also came accross another article about research on zinc recyclable batteries. Not sure whether same is commrcially viable at current stage. However, if successfully developed, could be major end use for Zinc going forward

Details of the company working and mentioned in above article

http://fluidicenergy.com/technology/zinc-air-technology

1 Like

There is this negative view too. Refers to ILZSG view also. http://www.mining.com/bear-case-zinc-price/

2 Likes