With capacity expansion in place and clear visibility of gross block reaching Rs 18 bn by FY26

(from Rs 13.13 bn in 9MFY25), they can do

Sales : 26%

EBITDA : 30%

PAT : 33%

With capacity expansion in place and clear visibility of gross block reaching Rs 18 bn by FY26

(from Rs 13.13 bn in 9MFY25), they can do

Sales : 26%

EBITDA : 30%

PAT : 33%

Can you please share the link to the report?

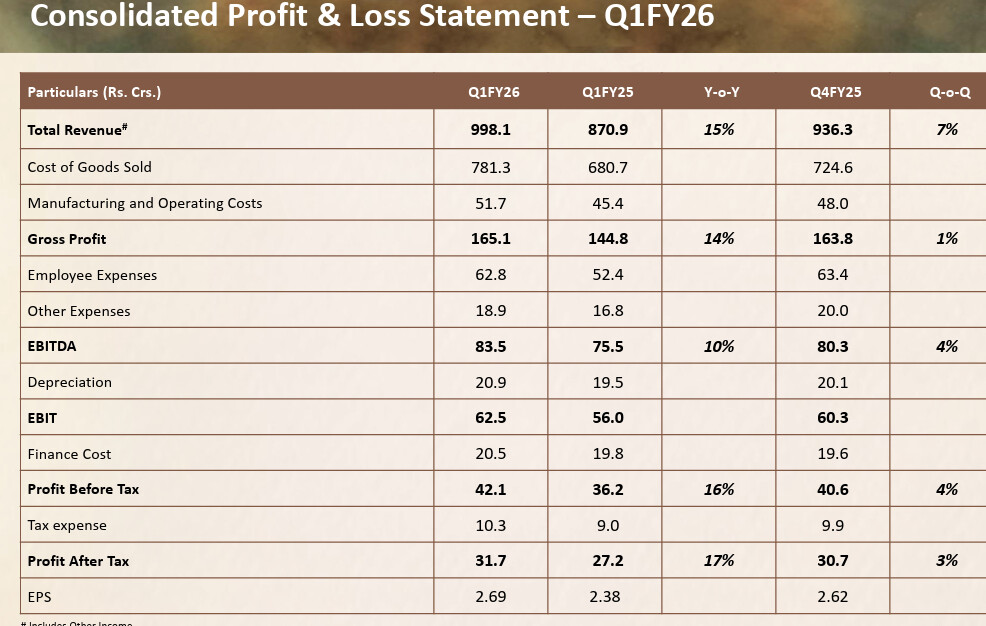

The divergence between the management comments and actual numbers continue. With Q1 being peak season for beverages and ice cream (despite the unseasonal rains, Q4 was < Q1 ), and with so many ‘ramping ups’, expansions and ‘highest-ever’ monthly production updates, its unfortunate to see a mere 1 Cr increase in Q on Q PBT. On top of this, there were one time costs last quarter towards employees in the shoe business. No way this can be a ‘satisfactory’ performance.