About company -

- Started in 1988. Was single product manufacturer of Farex of Glaxo from plant in Goa

- Strategic alliance with Vanity Case group in 2013

- Vanity case engaged in contract manufacturing for last two decades

- Turned around Goa unit with better capacity utilisation

- Company’s financial position was strengthened with restructuring and equity infusion

- Building the contract manufacturing business

- Added clients such a Pepsico, Reckitt & Benckiser, HUL, Hush Puppies, Steve Madden, US Polo, Gabor

- Increased manufacturing to six plants making pest control products, detergents and packaging teas

- Company is ready with contract manufacturing solutions to suit any type or size of FMCG customer across diversified categories

Board of Directors -

- Shrinivas Dempo - Chairman

- Sameer Kothari - MD

- Over 20 yrs of manufacturing experience, promoter of Vanity Case, CA + MBA (Cornell)

- Took over as MD from Ganesh Argekar on 22nd May, 2017

- Ganesh Argekar - ED

- 22 yrs of work experience, BSc Chem + PGDMM (IIMM) - Head Supply Chain of Vanity Case

- Nikhil Vora - Non-executive director

- Founder, CEO of Sixth Sense Ventures - India’s first domestic consumer-centric venture fund

- Rajesh Dempo - Non-executive ED

- Honey Vazirani - Independent director

- Served as VP - Labels and International Business Division at Huhtamaki PPL

- Shashi Kalathil - Independent director

- Sudin Usgaonkar - Independent director - Senior advocate - Bombay High Court

Shareholding (as of June 2018)

- Promoter group

- Vanity case - 60.40%

- Sixth Sense - 14.95%

- Nikhil Vora - 4.23%

Managerial remuneration

- Total managerial remuneration ~ 17 lakhs ~ 3% of PAT

- Only ED gets salary of 12 lakhs - everybody else including MD gets sitting fees only

Statutory Auditors - MSKA Associates appointed on 27th Sep, 2017

Business strategy -

- FMCG companies are focusing on leveraging brand building and marketing to address growing demand and outsource manufacturing

- Development and manufacturing of FMCG products require significant capital investment and has high operating costs

- HFL has ability to offer unique and customised solutions to reduce overheads and risks associated with manufacturing

- Goal to become leader in contract manufacturing for FMCG

- Besides contract manufacturing, HFL plans to partner with pvt. labels and smaller brands to offer formulation, packaging, branding, marketing and distribution

Business models -

-

Contract manufacturing -

- Manufacturing units utilised for various companies with temporary contracts

- HFL can offer product and volume flexibility to clients and cater to long term and seasonal product manufacturing

- Advantages to client - cost reduction, sample production + testing, quality production, easy to scale up production, time saving

-

OEM model -

- Entire manufacturing facility dedicated to single product of FMCG player

- Contracts have longer tenure of 5-7 years

- Generally require huge capital expenditure - can either be set up as greenfield project under direction from client or acquired on going concern basis

- Post completion, company looks after end-to-end supply chain management

- Types -

- Dedicated manufacturing -

- All decisions after due approval from client

- Fixed returns for long period based on return on investment or cost plus basis

- Anchor tenant model -

- Anchor client has say in all matters but may share facility with some other clients

- Agreement on quote base or cost plus basis

- Dedicated manufacturing -

-

Private label model -

- End to end manufacturing including formulation, product design and packaging design for small players

- Cost effective way to produce product without investment into large manufacturing facilities, etc.

- HFL responsible for procurement of raw material, development to packaging and owns product formula for these private labels

-

Own brands - build own products that are sold under branded names

- UN:OR - leather brand with store launched in Goa in 2017

- ESTD 1977 - under leather product basket of G Shoe Export

- Saucery (proposed) - currently acquiring stake in this spreads/dips/sauces venture founded by Gayatri Bhatia

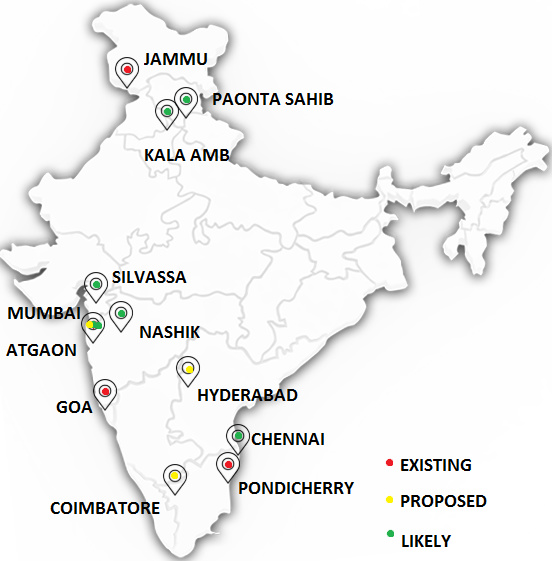

Plants -

-

Existing -

- Goa - Pepsico, Danone, HUL, Marico

- Expanded capacity from 3k to 6k tonnes in 2015

- Puducherry - leather products for Hush Puppies, Gabor, Richter, Jomos, Kenneth Cole, Steve Madden, TBS, Hidesign, Arrow, US Polo, Louis Philippe

- Acquired for HUL Ponds in FY17

- Integrated into leather processing by contracted tanneries

- Annual production of 5 lakh pairs of shoes and 7 lakh pairs of uppers

- J&K - pest control products (Mortein) for Reckitt Benckiser

- Acquired in end 2017 and started production on 2nd Jan 2018

- Claims to be the sole manufacturer of vaporizers and aerosols for Mortein in India

- Financing and operational performance -

- PPE cost ~ 27 crs, supported against term loan from Yes Bank ~ 24 crs @ 10.35%,

- Operations since 2nd Jan 2018: revenue - 35.49 crs, loss of 1.23 crs

- Expected annual revenue - 130 to 140 crs, profit ~ 3-4 crs, expected NPM ~ 2.85%

- Mumbai - leather footwear for Espirit, Saks 5th Avenue, Dune

- Acquisition of G Shoe Export to be completed in 2018

- Capacity of 3000 pairs of sandals and 1000 pairs of shoes per day

- Goa - Pepsico, Danone, HUL, Marico

-

Proposed -

- Coimbatore - tea, coffee, soaps for HUL

- Greenfield expansion to start operations in Q3 FY19

- Capacity of 20k and will be operational in two phases

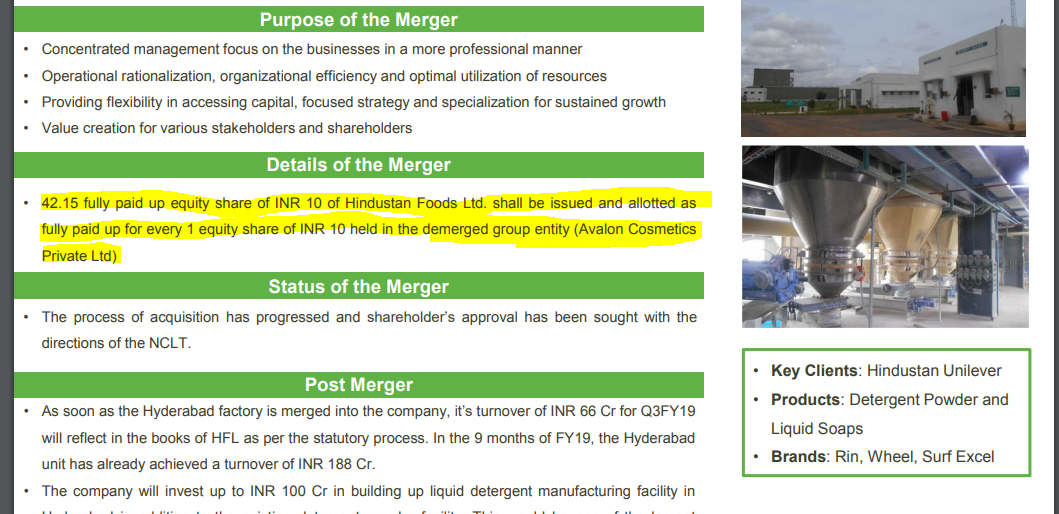

- Hyderabad - detergent powders for HUL

- Manufactures 75000 tonnes of powder - apparently only suffices Telangana state requirements

- Long term contract of 7 years that started in 2015

- Expected to be merged with HFL this year following demerger from Vanity Case group

- Coimbatore - tea, coffee, soaps for HUL

From MD’s desk -

- Money raised from preferential issue was used to strengthen balance sheet and acquire 2 plants and set up Greenfield project for tea packaging

- Company very confident to achieve near term revenue target of 1000 crs by FY 20

- GST is slowly leading to decentralisation of manufacturing units

- A number of small start-ups are coming up to cater to niche product categories - see great demand from here

- Focus more on OEM model of business to enable longer customer retention

- FMCG companies will focus more on marketing, distribution, logistics - to get product at right time, quality and cost.

- Especially FMCG companies from developed countries will shift or outsource production

Financials

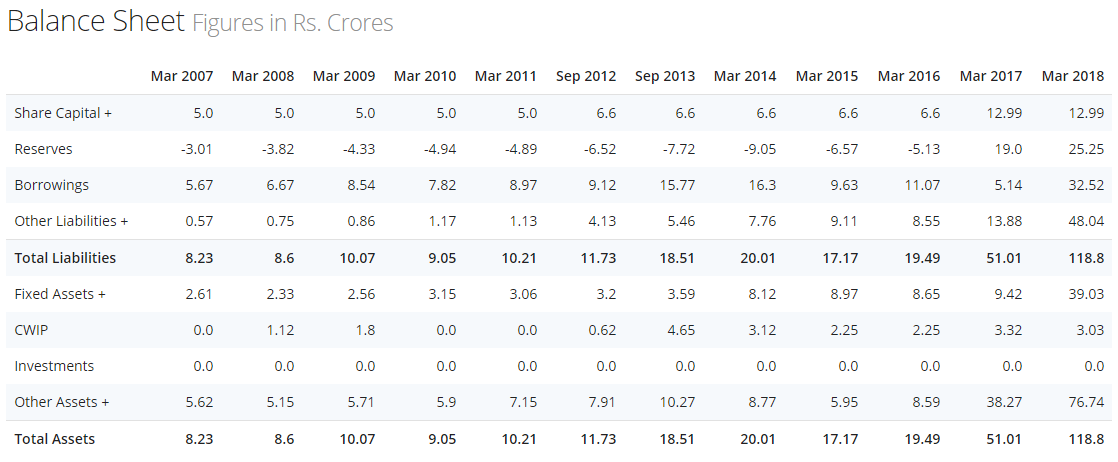

- Balance sheet

- Profit & Loss

- Cash flow statement

- Other financial parameters for FY18

- Fixed asset turnover - 3.6x

- Receivable days - 75, payable days - 108, invenotry days - 64: WC cycle - 31 days

- Debt to equity ~ 0.8

- NPM - 4.47%

- RoE ~ 16%

Investment rationale

- Industry structure, premiumisation of FMCG products + launches in more niche categories will lead to increased contract manufacturing

- Older FMCG players are likely to focus more on brand building and marketing and outsource the manufacturing function to contract manufacturers.

- Start-ups and newer FMCG players require manufacturing labs to test their products and develop brands

- Promoters’ experience in contract manufacturing (Vanity Case) across different FMCG product categories - in different geographical locations across many different clients

Key risks

- Key man risk - Singly handled by MD Sameer Kothari whose absence could seriously dent the company’s fortunes

- Client concentration - As per AR18, top 4 clients account for 75% of revenue. Any one-off event could dent operations. This is likely to go down as company diversifies across locations and bring more businesses under its wing from Vanity Case.

- Related party transactions - Although promoter has indicated that they will transfer all businesses to HFL, operations in similar lines of business and RPTs is a risk.

- Operational capability - MD has indicated very ambitious revenue targets - while most of this will come from transferring business from Vanity Case to HFL, the ability to have more long term OEM contracts in the pipeline will be the main challenge

- Negative CFO in the last couple of years due to expansion and increasing WC requirements

- Valuation risk - HFl trades at expensive PE of 75 based on current earnings, providing little margin of safety. If the investment thesis of exponential growth in revenue does not play out, the investment may not provide good returns.

Disc.: Invested, 3% of portfolio