3 main subdivisions, existing ~200cr TTM (Goa, Jammu, Pondi, Chennai) + ~250cr from the new tea processing plant in Coimbatore (which has started contributing since Dec’18) + ~250 cr existing detergent business of Avalon (Hyderabad). I think the next leg of growth will come from the ~100cr investment (Convergent + Sixth Sense) in Hyderabad which will kick-start only once Avalon is merged in to HF. The investment will result in additional 750cr of revenue.

So Avalon’s merger will result in equity dilution of 50Lac + 27.27Lac (warrants)= 77.3L shares or 317crs and adding ~ 1000 crs to topline. I dont have any idea about the margins of the overall group.

IMHO HF is a chance to bet on a rapidly growing - equity diluting contract manufacturer but if the above materializes, future organic or inorganic expansion could get funded internally (High ROE + High Growth).

a) Do you guys know the current capacity utilization that this business operates at? For me that’s a key assumption.

b) Also any idea what are the assets turns of the biz? Current PP&E at 81 crores + 60 crores (cwip). So with 150 crores and assuming asset turns 5x for a 750 crore revenue. Assuming a 6-7% PAT margin 38 crores of revenue. In order to get to 1000 crore it would have to get to 8-9x asset turns.

c) To get to 2000 to 3000 crores of revenue it needs another 100 to 200 crores to finance growth. I possibly see them generating maybe 100 crores in the two years or so maybe they finance the rest through debt.

d) Roc’s: so with a 150 crore PP&E + working cap of 50 odd crores (assuming 25 days of sale). I get roc of 19%.

If this business can get to 2000 crores in years it’s a 19% CAGR. At 2000 crores at 5-6% PAT of 100-120 crores the business should trade at north of 15x (assuming growth trajectory at 15% and roc steady at 19%) which values equity at 1500-1800 crores.

Also since management (though they have a controlling position) doesn’t take any remuneration from the business the profit is a bit inflated.

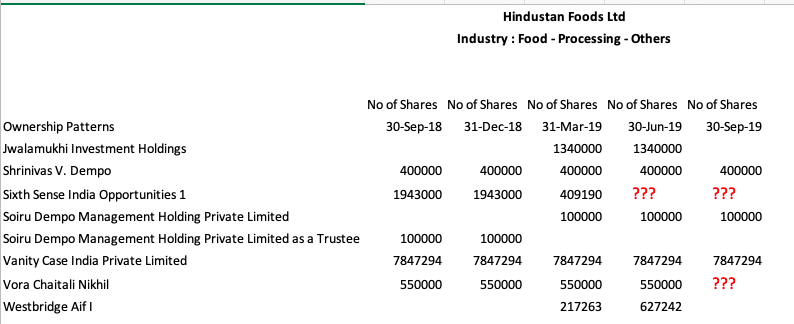

Sixth sense opportunity fund 1 exited but same quantity bought by Jwalamukhi/westbridge capital. But sixth sense opportunity fund 2 bought 8lac shares through warrants.

Hi Kanwal!

Just a quick question, have you ever written to the IR team of Hindustan Foods? Did they reply?

It’s been 2 weeks since I sent them a set of questions on their business performance and growth going forward, no reply yet (which I’m not sure how to feel about)…

Anyways, maybe you can help me answer these questions

Margins at the EBITDA level & subsequently PBT & PAT levels have declined year over year. I understand that an increase in depreciation expenses for Coimbatore & increased interest expenses resulted in PBT & PAT margin contraction, but could you further expand on the reason why at the EBITDA level margins have contracted? Was this a result of change in product mix? What should we pencil in as steady state EBITDA margins going ahead?

Once we are past the 1,000 crore revenue mark (hopefully soon) could you please guide us on management’s thinking on further diluting equity? I understand that contract manufacturing is a low margin business, and the 20% RoE on current business operations will only leave so much in the way of internal accruals, but that being said, what level of equity dilution should one expect in order to expand business to achieve the 2024 goal of 3,000 crores in top line? What would be the total capital needed & what % of that will be funded by taking on more debt?

What is management’s thinking about acquiring plants currently resting on the Vanity case group’s balance sheet, mainly the Chennai plant, the Silvasa plant & others. Is that the strategy going forward to incrementally acquire plants sitting on Vanity Case’s books and add it to Hindustan Foods?

What is the blended capacity utilization currently (ballpark)? And how much room do we have to incrementally increase asset turns going forward?

The above question is similar to a question someone else had over here) The main reason is that the Avg RoiC currently is less than WACC, unless asset turns go up growth is just going to destroy value, they cant earn less than their cost of capital, so that’s my reason for asking #4.

Thanks for starting this thread by the way, you presented the company and put forth your thoughts on it brilliantly.

Was going through this thread and this is a really good finding relevant from minority shareholder point of view.

I tried digging more on this but couldn’t find much information.

In September 2016, the preferential allotment had been proposed which got approved next month

“the consent of the members of the Company be and is hereby accorded to the Board and the Board be and is hereby authorized in its absolute discretion to create, offer, issue and allot, on preferential basis upto maximum of 80,00,000 (Eighty Lacs) equity shares of face value of Rs.10/- each at a price being not lower than the minimum price calculated in accordance with Regulation 76 of SEBI (ICDR) Regulations”

Here’s what SEBI (ICDR) Regulation 76 says:

“Pricing of equity shares.

76. (1) If the equity shares of the issuer have been listed on a recognised stock exchange for a period of six months or more as on the relevant date, the equity shares shall be allotted at a price not less than higher of the following:

(a) The average of the weekly high and low of the closing prices of the related equity shares quoted on the recognised stock exchange during the six months preceding the relevant date; or

(b) The average of the weekly high and low of the closing prices of the related equity shares quoted on a recognised stock exchange during the two weeks preceding the relevant date.” https://www.sebi.gov.in/acts/icdrreg09.pdf#page41

Now when the Preferential Issue price was set at Rs. 40 per share in December 2016, this prima facie appears to be a clear violation of SEBI rules.

But I’m not sure if any company can do something like this and get away easily.

Also strange no one else on the thread took this point seriously - so either there’s something very obvious which I’m missing or retail folks just believe “bhav bhagwan che” and don’t care about these things!

see - thanks for picking it - it is a clear violation. i was surprised no one picked on it. avg in 2016 was 80 to 90ish/share and they issued in dec 2016 at 40 bucks!

Thanks for sharing - this was the missing piece in the puzzle then!

However, as you mentioned the company should have provided the certificate / valuation report in terms corporate governance practices.

Anyway, I did some high level analysis of the valuation parameters mentioned by SEBI - book value, comparable trading multiples.

Firstly - let’s check whether this company can be classified under this category “Infrequently trade shares” or not?

Between 1 Nov - 7 Dec 2016 (date of preferential issue price announcement) the minimum shares traded on any single day were as low as 5 shares to a maximum of 5k shares. This results in turnover of Rs. 531 - Rs. 6.08 lacs on a per day basis. The promoters / non-promoters were looking to infuse 30 crores equity in the company.

So it’s a resounding yes to classify the company under “Infrequently traded shares”.

Now in terms of the issue price, at Rs. 40 - this is what the promoters / non-promoters paid in terms of the valuation of the company

Market Cap - 52 crores and below numbers adjusted for preferential issue in Dec 2016

FY16 Revenue - 24 cr

FY16 PAT - 1.45 cr

FY16 Book Value - Rs. 24 Price to Book - 2.17x P/E - 36x

H1FY17 Revenue - 9.6 cr

H1FY17 PAT - 0.34 lacs

H1FY17 Book Value - Rs. 26 Price to Book - 2x TTM P/E - 31x

Now looking at these numbers - Rs. 40 (~60% discount to market price) seems like very stretched valuations for such a small company doing revenues of less than 25 crores. Hence, it is safe to assume that those guys knew what they were doing and have managed to deliver from a business performance standpoint.

Happy to give the green light on this transaction then from a minority shareholder perspective.

Do note that in Sept 2016 - total issued shares were 50 lakhs. So at 40 bucks issue price, mcap would have been 20 crores then.

In Dec 2016 - post-issuance of new share - the total share count rose to 1.3 cr approx.

this is the power of valuepickr - building on each others’ analysis!

The 20 crores calculation would be correct if I buy out the entire company at that valuation with the company’s existing equity base.

With regards to the 2016 preferential issue - do remember that the promoters / non-promoters were not buying out minority shareholders - they were expanding the equity base by issuing 80 lac shares on top of the 50 lac shares resulting in total equity shares of 1.3 crore.

Hence market cap at Rs. 40 becomes = 40*1.3cr shares = 52 crores.

But you do have a point - I’ve not taken the last major equity dilution in 2019 in my calculation above which is why the difference in 84 crores market cap (previously calculated) and 52 crores coming out now. The promoters/non-promoters knew they’re getting their stake in the company for overall market cap of 52 crores post the preferential issue.

Even then for a company with barely any significant revenue (<25 crores) to pay 30-35x earnings multiple sounds like the promoters knew the future of the company very well. So cannot really blame them that Rs. 40 pref issue is too low.

Also updated the numbers in my post above. Thanks for switching the light bulb

to clarify - the 52 cr market cap we are considering here is the value of the company with FY16 revenues of 24 cr + 32 cr newly injected cash from pref share issuance.

And another interesting development from the investor presentation:

Company expects to get final order of NCLT in September 2021, approving the scheme of arrangement for merger of Malt Beverages making plant in Coimbatore for Hindustan Unilever.

I’m assuming this would have something to do with Horlicks/Boost.

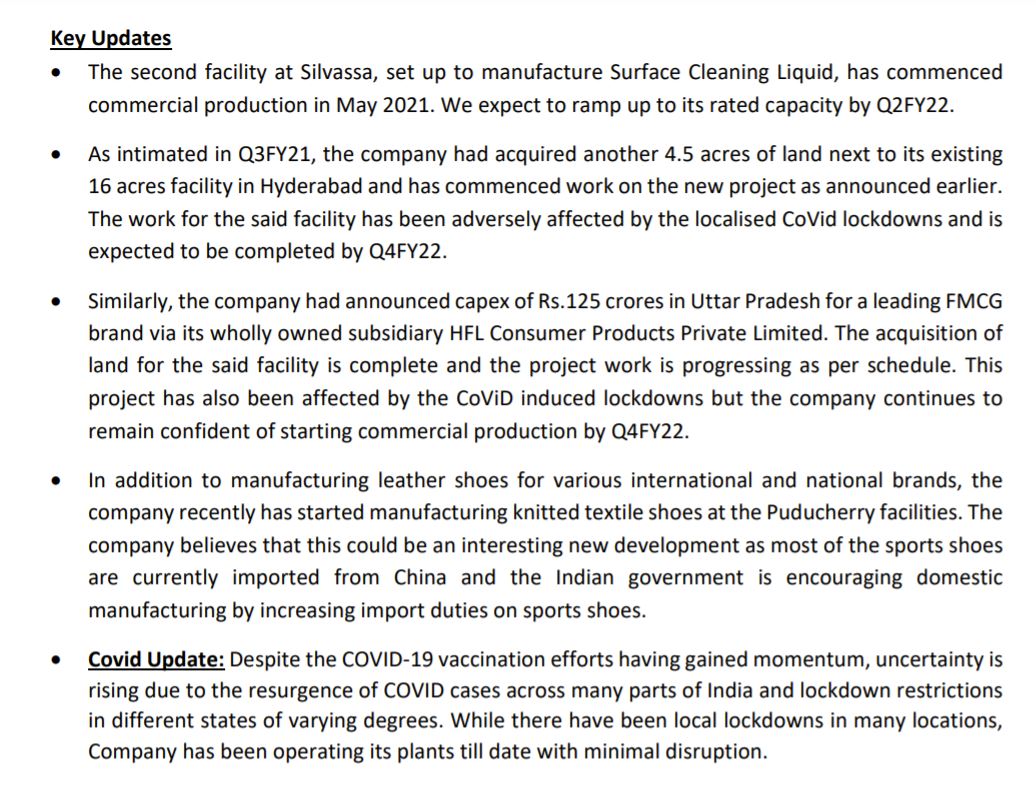

Both plants at Silvassa have commenced operations, expected to ramp up this quarter (Q1FY22).

New projects in UP / Hyderabad hit by local lockdowns affecting completion deadlines. No effect on existing operations due to covid. (Although they later said the beverage season was a wash due to covid, so I don’t believe this claim.)

Strong operating cash flows, up 4 times due to better working capital management.

Will invest another 200 crores (roughly 50% of their net block after current capex) for home care / food and beverage.

EBITDA margins will be in the range of 5.5% to 6.5% going forward.

Merging all Vanity Case business into HFL over the next two years.

Q/A Highlights:

On Capital Allocation Framework:

If it is a dedicated site, which has a take-or-pay contract, we have no limitation on the capital that we will allocate to such a project and that’s visible from the investments that we have done which are upwards of a couple of hundred crores in one particular site.

If it’s a shared facility where we believe that there is a lot of potential, but there is a possibility of us going wrong like we did in the shoe factory or like we did in the Mysuru beverage factory, the Board as well as the management has decided to restrict this capital allocation to around INR10 crores to INR15 crores.

In case of shared facilities where we believe that the operating leverage is very high, we will fund this capital using equity while in case of the dedicated site, we will be using a judicious mix of debt as well as equity because we have a take-or-pay contract.

This reads like a textbook game theory/utility maximisation framework.

Benefits from PLI scheme:

PLI rules have come in recently. […] Making representation to the government for it, will post updates to the exchanges when outcome is known.

As a contract manufacturer, it’s going to be an interesting tug of war between how much percentage of the benefit will be passed on to the customer versus how much will be retained by the contract manufacturer. This balance is present across the sectors. Too early to say anything right now.

Make in India:

The government has imposed substantial import duties on import of finished goods such as finished shoes from China. So all the international brands are definitely looking at Make in India, which is an evolving phenomena. We have just gotten into the category now (knitted sports shoes).

On in-house manufacturing vs contract manufacturing

Shared facilities:

[Big FMCG companies would use contract manufacturing when…] New product launches where they don’t want to invest money in setting up facilities. For this product, they would look at contract manufacturing.

Due to covid, handwash, cleaning product demands went through the roof. There is a lag between market demand and generating capacity. (This is only true if in-house capacities are at 100%…)

Dedicated facilities:

Used for more mature products with years of performance history, confident of performance over next ten years. Our facilities are for large FMCG brands, and have long term contracts in place.

On environmental sustainability:

There is zero discharge policies in most of the states. In Hyderabad, our largest facility, we are trying to take zero water from the ground. The government is also helping and pushing in achieving this.

Since most of our customers are multinational companies, they have their own requirement in terms of social compliances, environmental compliances which we are required to adhere to.

On ambition:

[For example,] In the color cosmetics area the contract manufacturers (six companies in Italy) now define and decide the agenda for brands. It would be a great achievement if we can get to that kind of a level, where if a brand wanted to launch an environmently friendly home cleaner or personal wash that they would come to Hindustan Foods because we would be the technological leader in terms of providing that solution.

Currently are product agnostic, will grow topline and later decide whether specialisation makes sense.