Vedanta has shown interest in acquiring Hind Copper as per newspaper reports

Mint: Vedanta eyes buying govt stake in Hindustan Copper.

2 Likes

5 Likes

HCL’s physical performance:

| FY20 | FY21 | |

|---|---|---|

| Revenue (Rs. Cr) | 832 | 1787 |

| Volume sold (tonnes) | 18408 | 32997 |

| Realization per tonne of MIC | 4,51,977 | 5,41,564 |

| Ore produced (lakh tonnes) | 39.68 | 32.73 |

| Metal-in-concentrate sold (tonnes) | 26502 | 23866 |

| Yield | 0.67% | 0.73% |

- Current price of copper is Rs. 811,000 per tonne.

- The avg realization for Q3FY22 was Rs. 7,15,000 which is ~33% higher than FY21 avg realization, and despite that HCL’s EBITDA margins didn’t improve much (from 22% to 24%).

- For a mining company, the increase in EBITDA should be disproportinate with increase in realization, but that’s not the case for HCL which I think is a dampener.

1 Like

One simple doubt…Why it is valued at a price to sale ratio of 10 ??

1 Like

Anyone tracking the company, I read somewhere in invester presenation that they are increasing mining capacity to 4x, can someone provide some colour on their capex plans, structurally copper demand is very high even though world marks are in slowdown due to its inherent use in green energy and absence of any substitutes, I dont know if valuations are high because market is factoring the capex that the company has done, would be really helpful if someone could provide information related to it.

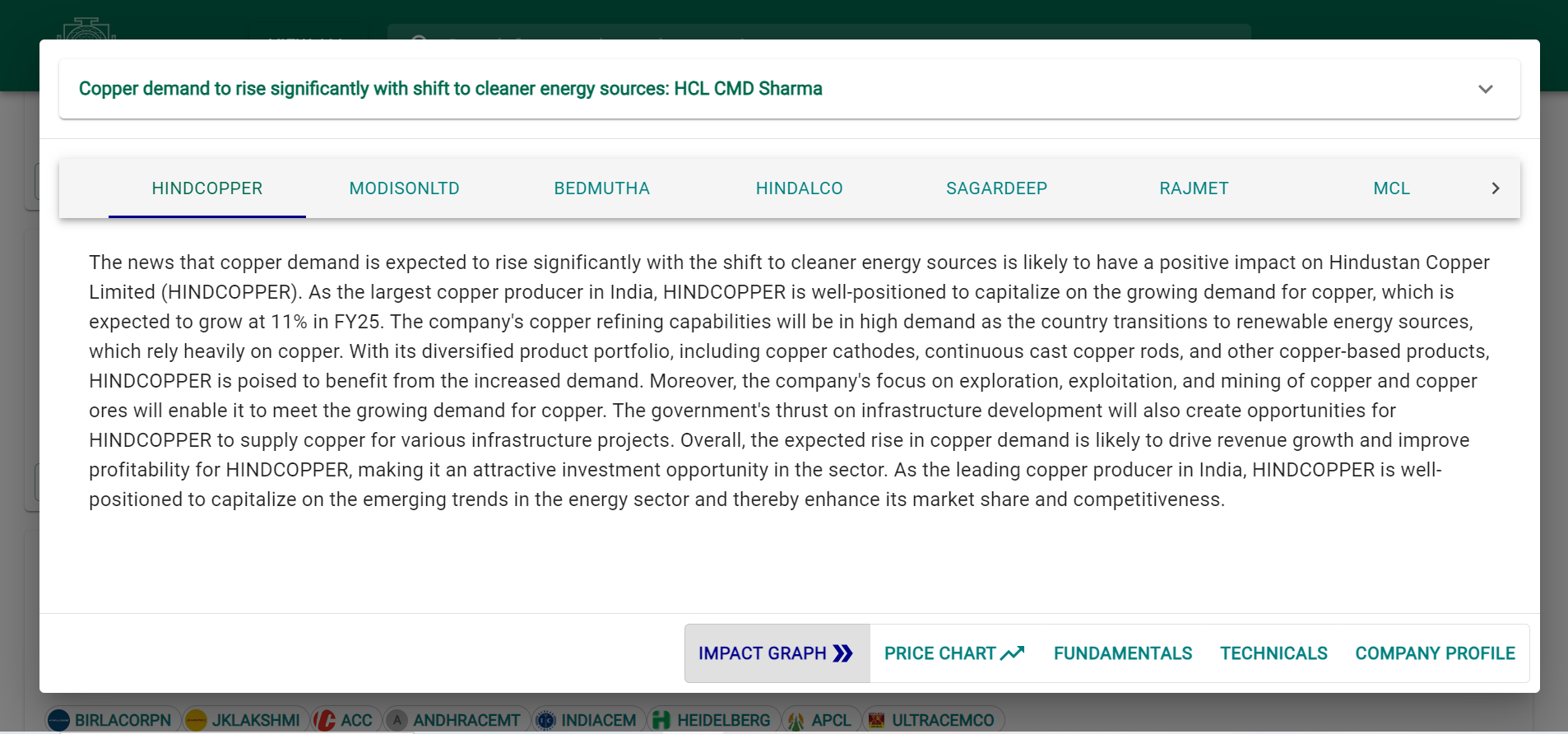

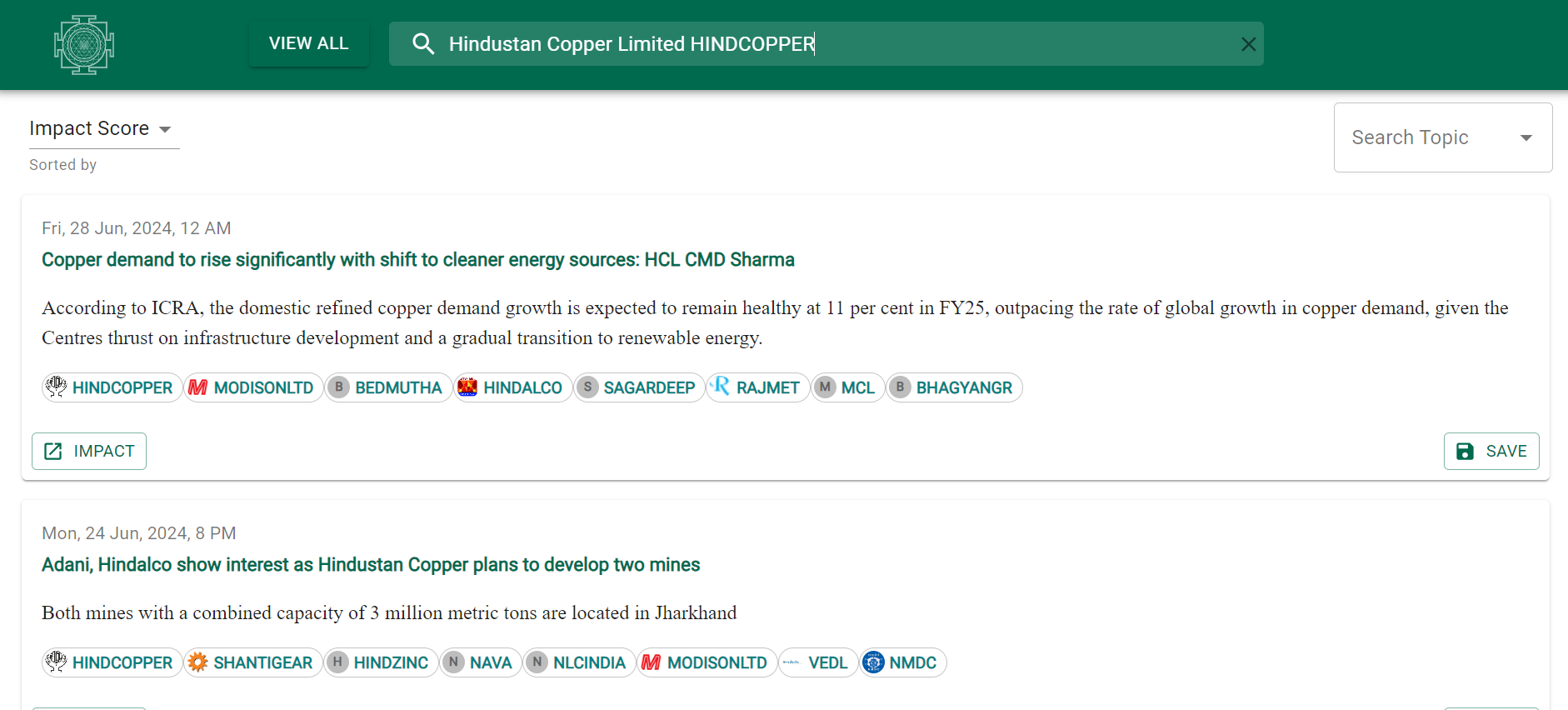

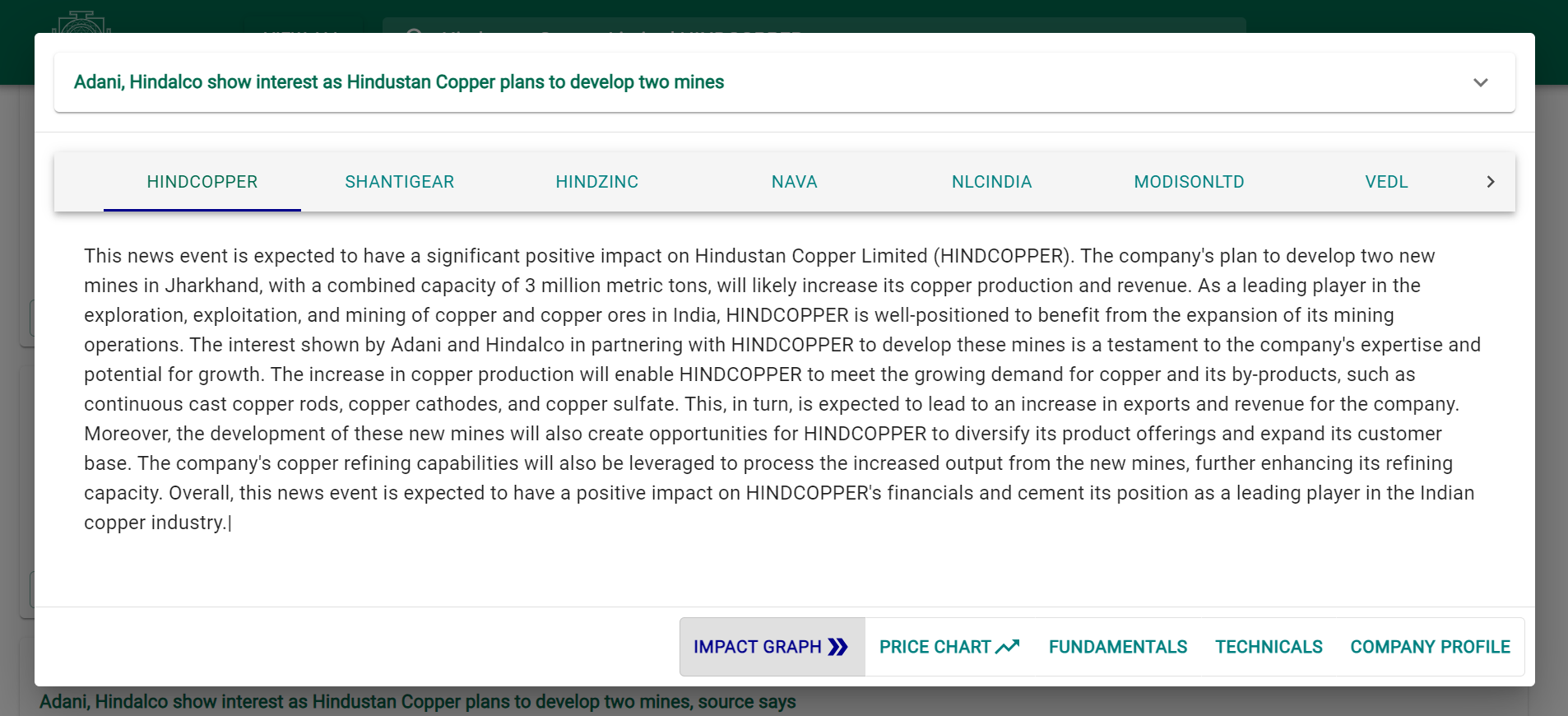

Hindustan Copper is likely to benefit from the shift toward green energy. Copper is also used in making EV components. The company has shown good profit growth. The price is not currently at its all time high. Adani and Hindalco are making investment.

2 Likes

Cyclical stocks, which are those whose performance is closely tied to the economic cycle (e.g., consumer discretionary, industrials, and materials sectors), are often valued using the price-to-sales (P/S) ratio

3 Likes

5 Likes

Copper prices trade off 9-month highs as Trump’s shifting trade policies raise uncertainty on economic growth

1 Like

Hind Copper has entered structural bull run and it has done multiple cup & handle breakouts at various levels starting at 350, then 390, 420, and so on

Once it crosses 610 on weekly time frame then it’s heading towards 1200 levels

5 Likes

hind copper has already rallied 140% since august, can we expect a consolidation phase or will the copper rally extend hind coppers run even more?

3 Likes

LME Copper Extends Surge Above $14000 for first time

Good interview. the 2030 estimates are conservative, rare earth optionality is not included, copper price assumed to be at 9k-10k$ and usd-inr at 93