As per the article : Hindustan Copper Ltd. is the only producer of copper concentrate in India. Under this MoU, around 60 per cent (copper content) of HCL’s current copper concentrate production will be utilised by Hindalco in the manufacture of refined copper.

3 Likes

How about playing the EV shift through the graphite industry.Batteries need graphite anodes.Other forms of EVs like fuel cells or organic batteries wont be commercially viable atleast for next 10 years.So what are your views on the impact of EV boom on the graphite industry?

From an exchange with Carlo Juan Zuleta on twitter @jczuleta [Lithium Economics Analyst].

·

Dec 20… Thanks for your kind comment. #Graphene could only be used as coating in the anode of some #lithium metal batteries. Due to its large surface area, high electronic conductivity and high electrochemical stability, it could also be utilized in the cathode of Metal-Oxygen batteries.

T/2 In principle, the metal batteries are the cutting edge tech today. Just need to define them properly. Regarding graphene, yes, its use will probably not be as extensive as many analysts suppose nowadays.

A response : by Peter Lattimore @peterjlattimore

Graphene, not really for the anodes… Silicon coated Spherical graphite, yes, but graphene more for structural purposes I believe.

Glasenberg warned that with population growth and the move toward a low carbon future with the electrification of energy supply, the world will require enormous amounts of energy metals, and directed participants on the call to look at a graphic in his slide-deck illustrating how much demand will grow for copper, nickel, cobalt, and zinc.

Pointing out that the world consumes 29.6 million tonnes of copper annually, Glasenberg noted that miners will have to produce 60 million tonnes of the red metal annually by the year 2050, to meet demand. Global nickel production will have to grow from the 2.5 million tonnes consumed a year currently to 9.2 million tonnes by mid-century; while cobalt supply will have to grow from 129,000 tonnes a year to 507,000 tonnes, and zinc production will have to more than double from 13.9 million tonnes per year consumed currently to 28.8 million tonnes.

…

Turning specifically to copper, he noted that mining companies are going to have to go farther afield to find it. “There’s limited shovel-ready projects around the world for new copper mines,” he said. “The world has a challenging task to meet this new demand and it’s going to have to go to new geographies, it’s going to have to go to new locations where they lack infrastructure, and you don’t have the mining expertise in those new areas.”

For more details:

2 Likes

Excellent results

3 Likes

#Copper #HindCopper

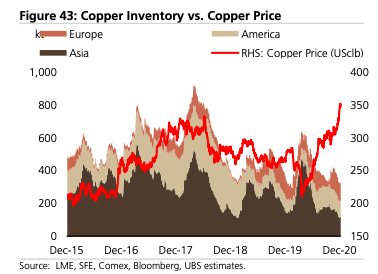

Copper has outperformed other base metals such as aluminium and zinc amid a broad rally in commodities.

The bellwether industrial metal rose above $9,000 a metric ton for the first time in nine years, taking a step closer to an all-time high set in 2011.

That, according to a Bloomberg report, was boosted by rapidly tightening physical markets, prospects for rebounding economic growth and hopes that multi-year low inflation in key economies may be ending.

According to Rakesh Arora, managing partner at Go India Advisors, the only company that benefits from this rally is Hindustan Copper, given a $1,000-per-tonne increase in copper price would mean higher operational profits.

A surge in copper price boosts the top and bottom line of Hindustan Copper. For every $100 increase/decrease in the LME price of the red metal, the turnover and profit margin of the company varies by Rs 18-20 crore, a company official told BloombergQuint.

PS: Holding in portfolio from lower levels

4 Likes

1 Like

Corporate Presentation

6 Likes

Thanks for Sharing

Wonderful presentation

Positive Point to be noted that one of its mining will be staring production soon

Hopefully company will achieve the indicated timelines for expansion.

Thanks for sharing the March 21 Investor presentation.

But frankly this and in fact all such companies presentations are positively biased.

It looks like this company is having lots of tail winds.

But to remain unbiased, what all negatives are for this company.

I personally think 2/3 things

- Being a PSU, difficult to understand government’s role in future

- Pure commodity play. So will depend upon Internmational copper prices

- Debt is on higher side

- For new mines to come on stream will take years due to various ministries clearances.

Please do share your views.

Have taken a tracking position at 150 in last 2 days

Regards,

Vikas

2 Likes

I think there is something cooking here - either privatization or expansion, I feel. Even otherwise, we are looking at quite a profitable year for the company. Quarterly profits could go up to 175-200 crores, in the best case scenario, at the current production levels.

I don’t understand price movements that well. But personally, I think there are more legs to this ongoing rally if copper prices don’t fall suddenly. That said, there is a lot of operator driven action going on over the last few days. Strange intra-day stock price movements - rather interesting to observe actually.

3 Likes

6 Likes

News on Copper, Added it to Commodity forum

2 Likes

@Rakesh_Arora

Sir your views on Hind copper

Recent reports suggest the price hike expected in future.

The company has shown profit after long wait.

Is there any update on its completion of capex and starting new capacity in near term.

Thanks

2 Likes

3 Likes

Results are out. Any comments from experts on these results especially on the exceptional expenses.d92d06bb-2818-410b-8232-15789c8a5e8f (1).pdf (1.1 MB)

Copper seems like the mega trend of the decade yet many seem to be skeptical of the stock Hindustan Copper because it’s a PSU.

Seldom we come across a product which is enjoying both supply side and demand side tailwinds

Supply tailwinds - constricted worldwide supplies…huge entry barriers in terms of new site discovery and new plant set up…decline in world copper production due to a host of environmental and geopolitical issues (India’s production got curtailed by 50% due to closure of Vedantas Tuticorin plant)

Demand tailwinds - EVs and Clean Energy are part of a probably the biggest defining trend for the foreseeable future - The Green Industrial Revolution which is gaining ground steadily in Europe and other developed parts of the world …copper used in a EV is about 60kg/car vs 24k/car for old school ICE - do a more than 100% jump just from the tech auto sector.

From the Indian perspective, copper utensils and bottles have picked up a lot of traction due to rising health consciousness accelerated by the pandemic

There is simply no alternative to the green metal when it’s pros are compared to its peers like aluminium, nickel and zinc. So substitution risks are reduced by a good extent.

Now, Gsachs has called Copper as the bew Oil and so have commodity analysts and experts world over!

Hindustan Copper - being a monopoly in mining copper in India seems to be well poised to encash this mega story

10 Likes

The only thing im skeptical about is the entry barriers.

The government is very much in favour of privatisation of the mining sector and may auction of some mines.

Also Vedanta has filed for reopening of Tuticorin plant

1 Like