Hi All, any idea on shareholding pattern - sudden drop in DII holding from Jun - Sep down from 20% to 5% and checking further LIC has sold 15% i.e full stake… and its bought by Public not FII’s or other DII’s , creating doubts near future… any comments please…

1 Like

just figured out , the LIC holding which was showing under DII’s actually now being shown as under Public , which i m nt sure why… but it is showing in screener.in… so i believe lic’s holding is intact still, public holding hasnt changed…so my above concern isnt valid as such…

I think it’s because LIC is preparing for IPO and the insurance business needs to be separated from the company balance sheet and the stock is being transferred from the insurance to investment co - That’s what I think … need to reconfirm

2 Likes

Long-term rating upgraded to [ICRA]AAA;

1 Like

1 Like

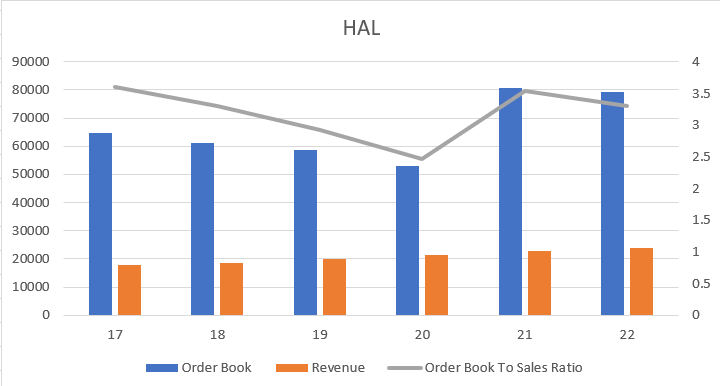

Is there historical data available on order book? One could look at the order book to sales ratio in the form of a chart and assess the present order book in that context.

Edit: Prepared this chart

Raw data:

| HAL | 17 | 18 | 19 | 20 | 21 | 22 |

|---|---|---|---|---|---|---|

| Order Book | 64613 | 61124 | 58588 | 52965 | 80639 | 79229 |

| Revenue | 17,950 | 18,520 | 20,008 | 21,445 | 22,755 | 24000 |

| Order Book To Sales Ratio | 3.599610028 | 3.300431965 | 2.928228709 | 2.469806482 | 3.543792573 | 3.301208333 |

Disc- no holdings as of now

Edit: Added a tracking position on 11 Apr 2022

2 Likes

In S2 , good wave structure -ssems to have a long runway.

No reco, just sharing the chart structure.

Hi All,

I have started understanding the business of HAL and have gone through this thread in detail.

Considering the large order book, and possibilities of export, stock price looks close to fair value or marginally overvalued. I am unable to decide P/E range for this PSU as of now.

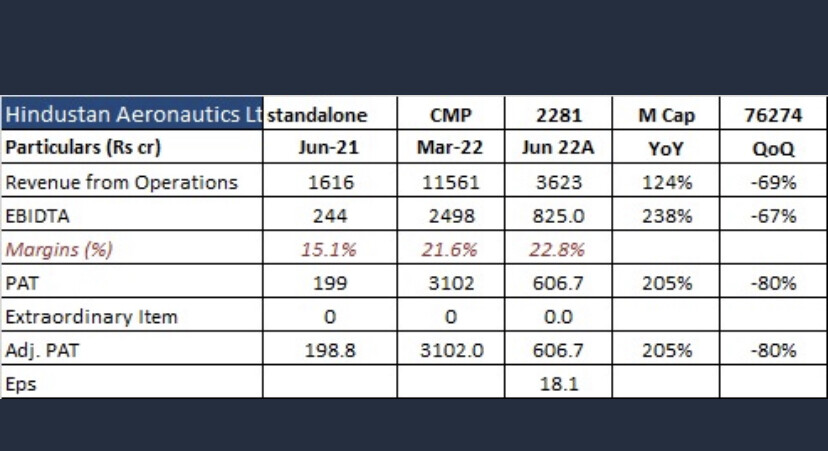

Also, I have not understood the reason for only 3% Tax in March 2022 (FY22). It would be good to hear from those who have already invested in this stock. Does this happen frequently that, tax fluctuates in this business or was it some one off reason.

Due to this very low 3% tax in FY22, EPS has zoomed from 96.88 to 152.11 in FY22. This is about 57% PAT growth. PBT has not gone up that much. So mainly EPS growth has come from low tax payout. I might have missed the reason for this while reading the thread.

Disc : No investment.

Hi All,

I think, HAL has received tax refund for AY2010-11 and also for 2015-16 as per their letter to BSE & NSE dated 17th February 2022, hence the tax outgo seems to be only 3% in FY22.

Hence as an investor, one may have to consider this and adjust the EPS accordingly.

Disc : Under analysis. No investment.

2 Likes

HAL in drone business

HAL manufacturing

3 Likes

Tejas mark 2 - there are many business opportunities with this to HAL. Higher margins due to make in India equipment’s.

1 Like

1 Like

Good to see that, apart from BrahMos, which was acquired by Philippines, Tejas is also getting orders from various nations.

After the sad episode of 2000, where Ecuador grounded the Dhruv ALH and ended the contract with HAL, now in 2022, HAL is getting recognition and benefits of its R&D.

With increase in defense budget and also orders from Ministry of Defense, there are some tailwinds for HAL business.

Disc Under watch list. Being a PSU stock, looks fairly valued.

1 Like

Order Book position of leading Defence companies

Discl: Invested in some of these stocks as a part of my defence basket. I may be biased .please do your own assessment before investing

2 Likes

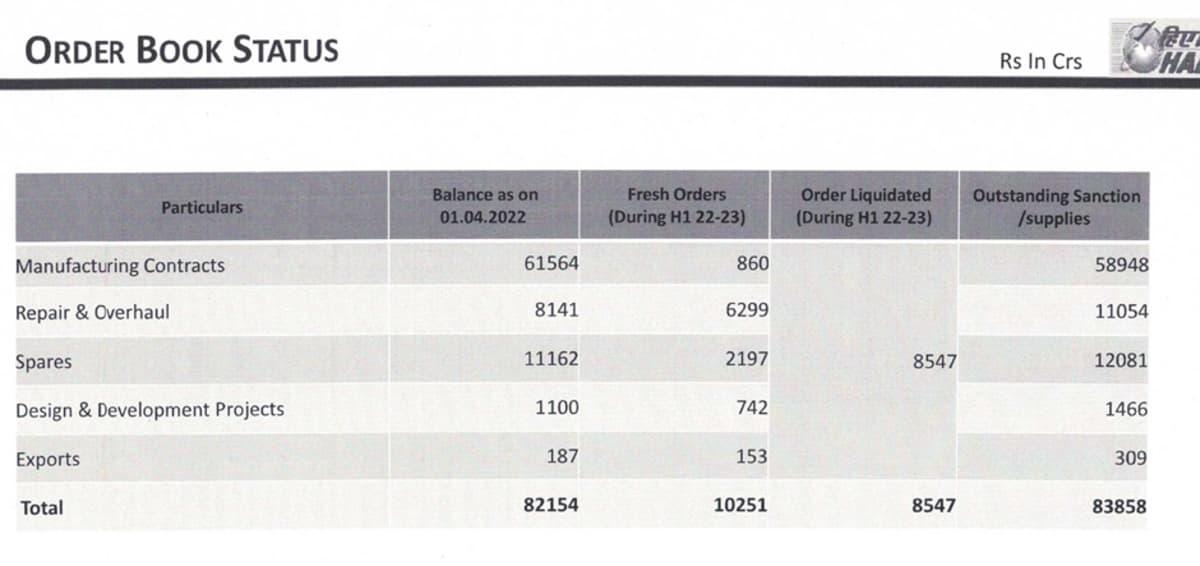

Watch Latest Interview with HAL CMD. Order book from 84000 Crore 1,20,000 crore within next one year!

Video appears just after head lines paragraph

VIDEO: ‘Make in India’ push in defence sector, HAL’s order book to grow from current Rs 84,000 crore

https://s.tnn.in/1PzQdkdLSxApPCY37

2 Likes

- Overall revenues are expected to grow 7-8% and ROH revenues to grow 10-12% in the next 2-3 years.

- EBITDA Margins are expected to be 26-27% for FY23.

- Signed MOU for opening an office in Malaysia.

- Targets 10% revenue from exports.

- Additional orderbook of Rs. 50000 crores seen in the next 6 months to 1 year which are for manufacturing of aircrafts, helicopters & engines.

- Cash balance likely to sustain at healthy level of Rs140-150bn by FY23-end mainly due to the receipt of milestone-based payments.

- Order book position at Rs.83858 crores.

3 Likes

I have been holding HAL for about 2 years, my entry thesis was very crude- stock was trading at around 10X PE , order for Tejas Mk1A was imminent and its primary customer (IAF) desperately needed aircrafts. The stock since has almost trebled , still showing tremendous strength on the charts coupled with euphoric frenzy for defence stocks. This was a good time to review my holding which at the face of it still looked fairly valued at 16X PE, order book almost equal to the MCap and around 16,738 Cr cash in bank. As we will soon find out, these simplistic valuation metrics often flatter to deceive.

How does HAL make money?

One can break the total revenue for HAL into following segments

- Manufacturing

- Repair and Overhaul (ROH)

- Design and Development

Let’s look at each of it separately to forecast the total revenue

Manufacturing

HAL mainly manufactures fixed winged aircraft, rotary aircrafts (helicopters) and engines. They have some UAV programs in developments but it will take more than a decade to get into production.

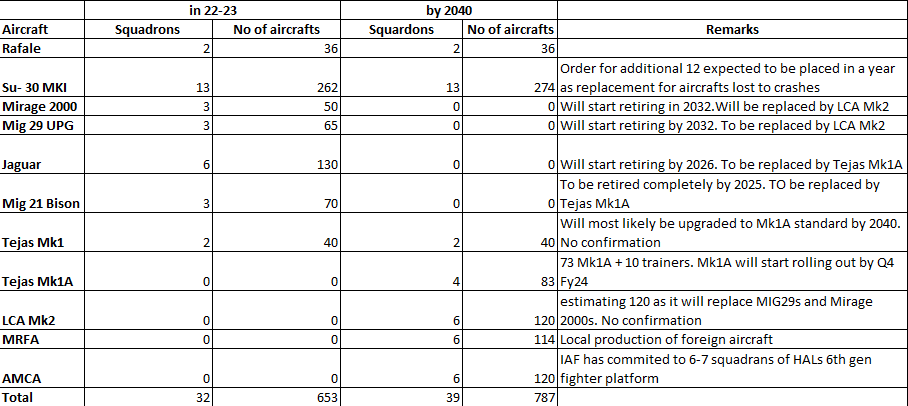

Before delving into the demand scenario for its platforms, let’s first look at the status of the main platforms on offer from HAL.

Mature platforms- Platforms with an active production line that are currently being manufactured or manufacturing has been paused for lack of orders.

- Su 30 MKI- Licensed production of the Russian twinjet multirole fighter. Only 12 more to be produced over the next couple of years to replace aircrafts lost to crashes.

- Light Combat Aircraft (LCA) MK1- IOC and FOC variants of the Tejas aircraft which was indigenously designed and developed by HAL.

- Advanced Light Helicopter (ALH)- 5.5 class twin engine multi role helicopter indigenously developed and manufactured by HAL . ALH Dhruv is a transport helicopter while ALH Rudra is its attack variant. There is also a Naval versions of Dhruv for Navy and Cost Guard.

- Dornier 228- Twin Turboprop utility aircraft mainly used for naval reconnaissance and transport. Manufactured under license by HAL

New Platforms- These platforms have LSPs/ flying prototypes ready. Orders for these platforms have been placed and HAL has shared their production timeline.

- LCA Mk1A- Advanced version of Tejas Mk1. Orders placed for 73 Mk1As and 10 trainers by IAF. Delivery will start from Q4 FY24

- Light Utility Helicopter (LUH)- New 3 tonne class single engine Helicopter, indigenously developed by HAL. MoD has placed order for 12 LUH under Limited Series Production (LSP) of which 6 are for the Airforce and 6 for Army. 6 LUH are ready to be delivered and after user trials of about 1 year IAF and Army will place order for about 160 LUH.

- Light Combat Helicopter (LCH)- Attack Helicopter indigenously developed by HAL. MoD has placed 15 LSPs ordered for Army and Airforce, 4 of them derived the remaining to be delivered in 6 months. Around 160 to be ordered after user trials.

- HTT 40- Turbo prop trainer aircraft indigenously developed by HAL. Orders for 70 aircrafts have been placed with an indication of 38 follow up orders. Deliveries will start from FY25.

Platforms under development- These platforms are in fairly early stages of development. None of them have a prototype ready

- Tejas Mk2- Twin Engine variant of Tejas. CCS has approved Rs 6500 Cr for prototypes. Rollout expected by 2024 followed by development flight trials. Production expected to commence by 2030.

- Advanced Medium Combat Aircraft (AMCA)- Twin Engine Medium weight 5th Gen fighter aircraft being developed by HAL. CCS approval for prototype expected by end of this FY. Production expected to commence by 2034-35

- Twin Engine Deck Based Fighter (TEDBF)- 4.5 Gen Naval fighter being developed for the Indian Navy. Production expected to commence by 2032-33.

- IMRH- Medium Lift aircraft being indigenously developed as a replacement to Mi-17. First flight expected by 2026, might be production ready by 2030

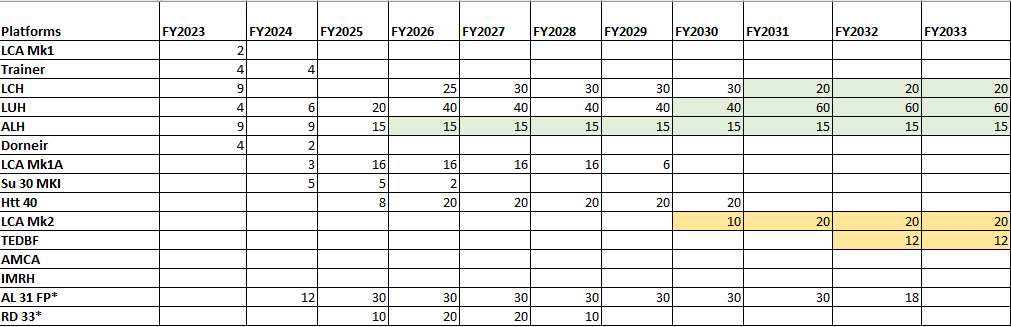

IAF is the primary customer of HAL. To estimate HALs production rate we can start off by understanding IAFs requirement for fixed winged fighters.

IAF has a sanctioned squadron strength of 42 squadrons- we are currently operating at a deficit.

Apart from this, there is a requirement of 60 naval fighter aircrafts for which TEDBF is currently being developed

On the Helicopter front, around 187 Chetaks and 200 Cheetahs are currently in use by the three services. They will start retiring by 2025 and will be replaced by LUH.

Additionally, Army , Navy and Cost guard keeps ordering batches of its workhorse- the ALH.

IAF and Army together need around 170 attack helis which will be fulfilled by ALH.

So, in all India will have to produce around 500 fighters and around 600 Helis in the next 15-20 years in addition to Engines, UAVs and transport aircrafts.

So far so good!

From the concalls, management commentaries and order wins it is fairly simple to find the cost of a platform and estimate the revenue it will generate. I have tried to estimate 10 years production schedule with this data.

*AL 31 FP is Su 30 MKI engine while RD 33 is Mig 29 engine. The price of AL 31 was confirmed in a concall, I have roughly estimated price of RD 33 to be 60 Cr as it is smaller than AL 31 (50KN vs 85 KN). LCA MK2 and TEDBF prices are estimates based on cost of similar aircrafts sold internationally in the same category.

Highlighted in green are expected follow on orders (which is just my assumption) HAL can scale up its Heli production to 90-100 units per year, I am assuming they will push for follow-up orders or crack some export orders to keep the production line running at capacity. Haven’t considered IMRH as HAL has shared very little details on its production. If it is indeed ready by 2030 we might see IMRH being produced instead of ALH. IMRH will be around 3 times the cost of ALH.

Su 30MKI orders have been delayed due to Russia-Ukraine conflict. I am assuming it will come through by FY2024.

Tejas MK1A can get follow up orders (to make up for the 3 squadron deficit to the sanctioned squadron strength) or crack an export deal (aggressively being pursued by HAL) to keep the production line running.

Tejas MK2 project director has stated that long term production rate of fighter aircrafts will be 48 units/year. I assume this will be the rate when AMCA, Tejas MK2 and TEDBF will be produced together.

Highlighted in yellow are platforms which are still under development. These may get delayed

The timing of production of these platforms might differ a bit to these estimates but there is very little scope to add more platforms or produce more number of these.

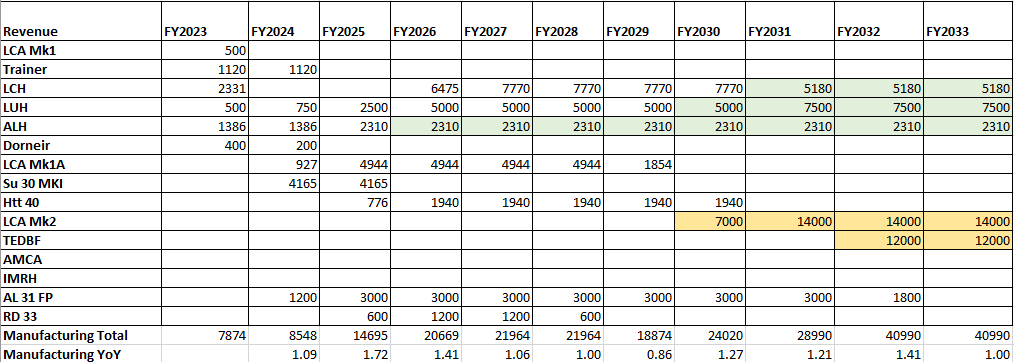

Repair and Overhaul

Repair and overhaul revenue is the revenue generated by HAL for maintaining/upgrading an aircraft. Full repair and overhaul happens once every 10 years or after 2000 Hrs of flying

For FY 23 Management has guided ROH revenue of around Rs 13000 Cr with 12%-15% growth in the next 3 years. For FY 23, the split between ROH and Manufacturing will be 60:40 , once manufacturing orders starts getting executed the long term split of 50:50 has been guided. Margins for ROH are higher compared to manufacturing.

ROH revenues are fungible in the sense, whenever manufacturing drops the company can do more ROH and maintain overall revenue growth. With most of the current platforms being upgraded to fly till 2035 and the pending Super Sukhoi upgrades, there will be no dearth of ROH orders.

Design and Development

Design and development revenues are from platform under development. They are recognised when development milestone on a particular platform is achieved. It’s based on budget allocation and CCS sanction, hence a bit lumpy. Management has guided for Rs 1600Cr to Rs 1700 Cr of development revenue for the next few years.

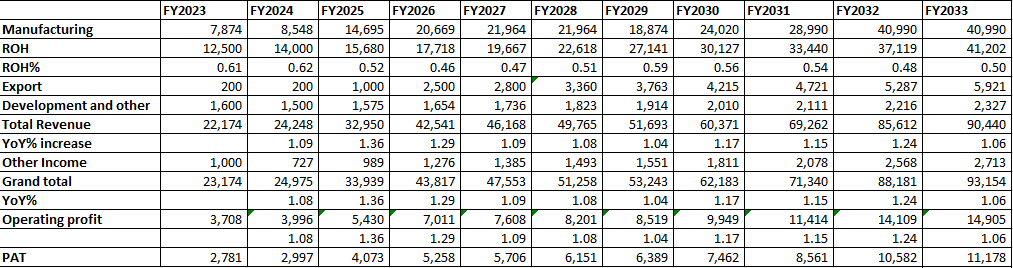

The narrative till now seems all very rosy. Let’s try to put these numbers on a spreadsheet to estimate FY33 PAT

PAT Forecasting

Below is the revenue estimates from the production schedule shared earlier

For FY23 and FY24, management has guided for 8% revenue growth. FY25 onwards management has guided for a double digit growth but they haven’t given an indicative number. Based on the production schedule FY25 growth for manufacturing revenue seems to be around 72% post which it is quite lumpy. Over a 10 year period the revenue growth in manufacturing should be around 18% CAGR

Combining manufacturing revenues with other segments

For ROH & Manufacturing, management has guided around 60:40 split for FY23 and FY24 post which they have guided for a 50:50 split. For some years where the manufacturing revenue growth is low, I have taken the liberty to take the ROH contribution up to 60% (similar to what they are doing this FY)

Management has kept a target of Rs 2500 Crs for exports from FY25-26. I have estimated a constant 10% growth in export revenue from FY26

For Development revenue I have estimated a 5% growth from FY24 ( no real basis for this)

Other income is typically interest earned, fair value adjustment and foreign currency gain. Keeping it at 3% of revenue

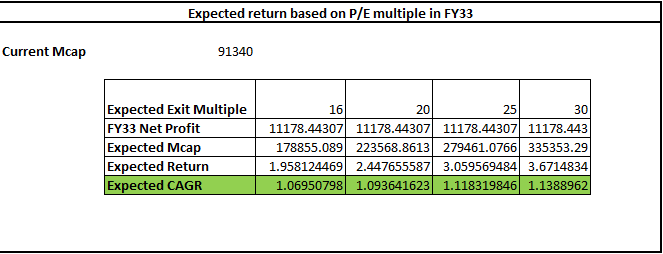

Management has guided for long term operating margin of around 16%-17%. I have considered 16% operating margin and assumed 25% tax rate to arrive at PAT. The CAGR on PAT for 10 years period of FY24 to FY33 is 14%

Closing thoughts

Even at an optimistic exit multiple of 30, the CAGR return would be just around 14%. For a more realistic 20-25 exit multiple the CAGR return will be 10%-12%. For a decade (India’s decade as some are calling) where everyone is trying to find companies growing at 20% CAGR, this rate seems low.

HAL will have 2-3 instances when its revenues would spurt up. First around FY25 when full scale manufacturing of MK1A, LCH and LUH commences and the second around FY32-FY35 when full scale production of its underdevelopment projects like AMCA, TEDBF, Tejas MK2 and IMRH begins. However, these ambitious projects are in early stages of development with high probability of delays and some probability of failure as well. Right now, markets in its euphoria for defence stocks seems to be discounting the production of even these projects.

A prudent investor would rather check in from time to time between 2025-30 to look at the milestones achieved by these underdevelopment platforms and accordingly take a call when the sector is out of favour.

I love HAL and for the sake of our nation I wish it succeeds in all its projects and delivers world class platforms. If someone can point out a flaw in this piece or provide a rationale that materially changes the projections, I would be happy to hold on to this stock. For now, I have however made my mind to completely exit from this position next week.

I have separately done a FCFE valuation which gives a fair value significantly less than the CMP. For the assumptions used and adjustments done, explaining the model would require another post so not adding it here.

Disclaimer: I am not a part of this industry nor am I an industry expert. All of this is based on secondary research of publicly available information. Do your own due diligence before making an investing decision. Feel free to point out gaps/mistakes in this piece.

Disclosure- Holding HAL from around 980. Currently around 14% of my portfolio. Completely exiting from it in the coming week.

Edit: Exited completely.

17 Likes