Hi Amil,

Thanks for the reply, with information I have gathered , I replied to your queries.

- This is the first company in India which introduce the Employee Stock options.

Major Equity dilution happened during the Simplot joint venture.

The company has been financing its growth mainly on issuance of equity.

During the Gujarat expansion the Company has tied up finances for the initial investment via a warrants issue, internal cash accruals and term loans of INR900 million from lenders

2.The company is planning to raise the loan from Foreign Funding with favourable LIBOR linked interest rates for payment of existing High interest Debt and Working capital and enhancement of business.

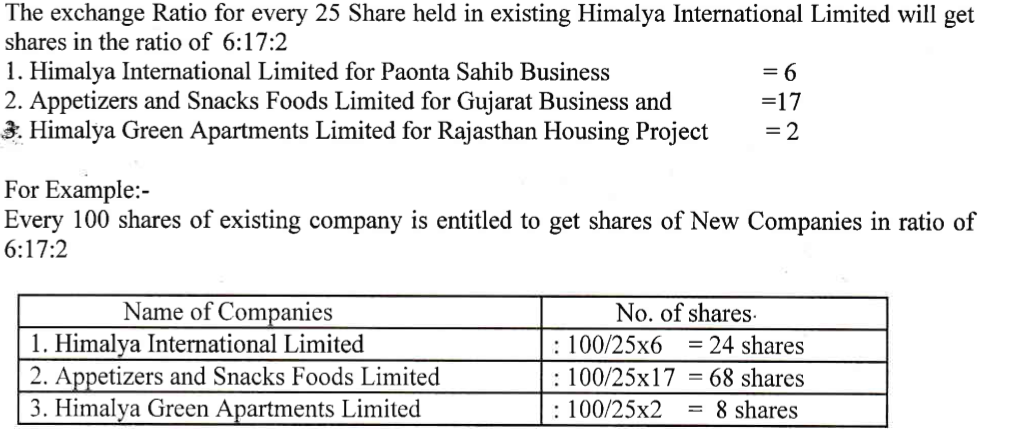

The surplus fund are proposed to be invested in Special Purpose Vehicles for French Units at Gujarat and for Project for EWS housing development by the company in Rajasthan , mentioned in AR2016

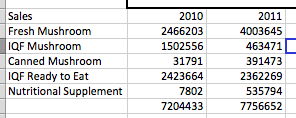

3.During the 2010 and 2011 Annual report they have provided the details. But after that I couldn’t find any details.

Sales in Kg.

4.The research report seem to be quite old which is for the year 2009 and 2010.

5.Yes agreed.

6.Yes they do have the ambitious plans. But If you see the corporate history which I have collected from various sources.

http://forum.valuepickr.com/uploads/default/original/2X/2/25d06f237ff143f533ace1ebce674efdc60da3c6.pdf

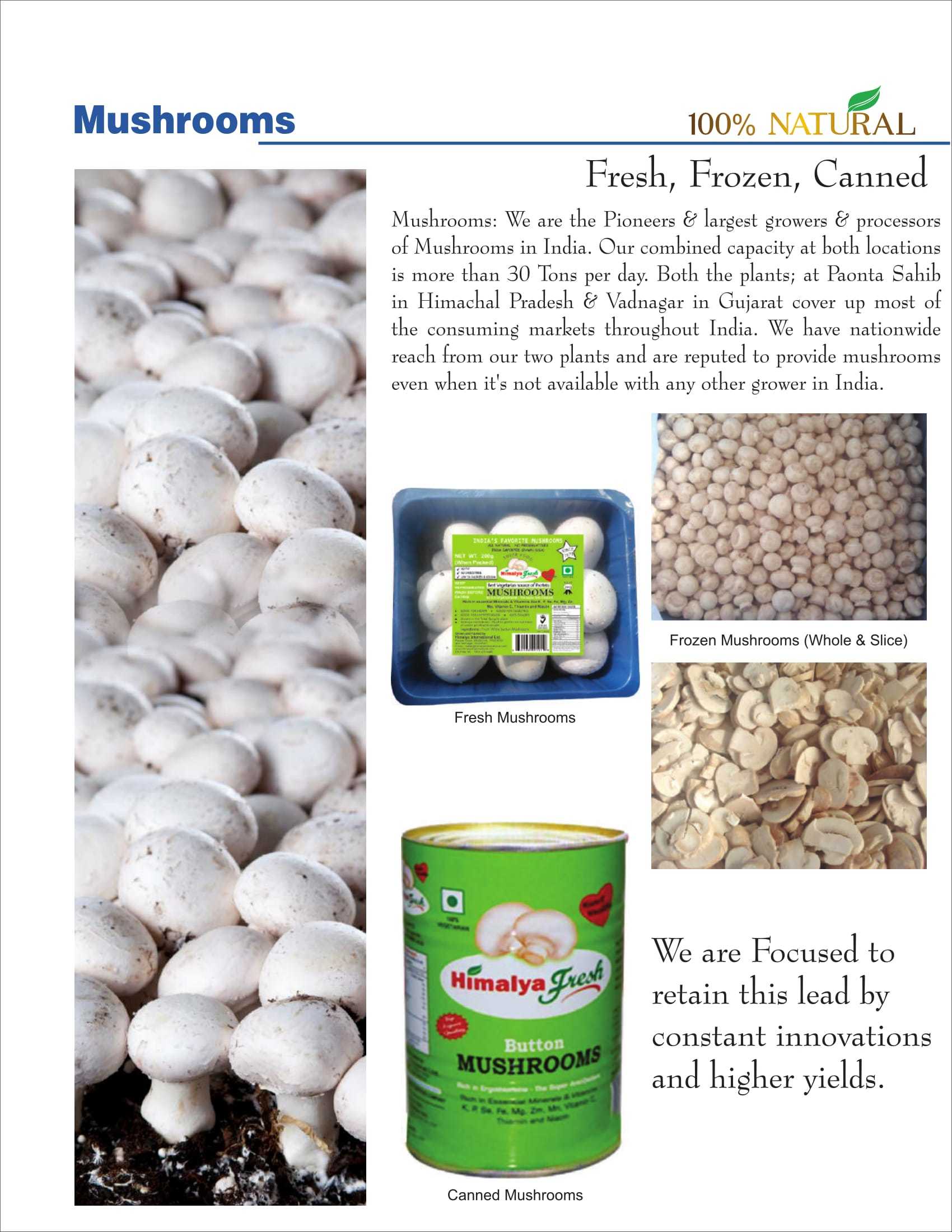

Himalya is the first company to introduce and export of PortoBello Mushrooms and also the first company to export Mozzrella cheese from India.

They are first company in the world to manufacture Fresh Mozzarella di Bufala outside of Italy. Later Italian Giuseppe Mozzillo and Flander Diary started its operation after seeing it success.

First time in India it introduced Fruit based blended Yoghurt.

During the initial stage there were limited markets for Mushroom and they have to struggle , because there is no sufficient cold storage availability and they couldn’t sell the products in the Indian Market. At the time Indian markets were not much mature enough to consume that much quantity of Mushrooms and other Frozen items.

7 .Not sure!

8.They have filed the case against Simplot to recover those damages, court case tends to take time so not sure.

For the Warehouse case 750,000 dollars amount is already settled.

9.I have earlier mentioned in my previous queries,

Reason for Joint Venture:

The reason behind the JV with JR Simplot is to market Himalya products in India and South East Asia.

And it aims at sales of $50 million in India and South East Asia markets within the next three years. Besides marketing, JR Simplot will provide technological expertise in potato farming and in production of french fries.

Old interview in Money control - Himalaya International forms JV with JR Simplot

10.From the year 2010 to 2012 they have heavily invested the Gujarat plant, expecting revenue sales of $50 million in India and South East Asia with JV with Simplot

For the past 3 years after the breakup , the company has negative revenues, they couldn’t operate the Gujarat units because of the Court case and exclusive agreements . Which erodes the revenues.

Now after terminating the agreement and winning the court case in Singapore ,the revenues has been increased which is reflecting in the past 3 quarters.