Hello Revisting Himadri Speciality Chemicals …

No updates n this company for a long time…

Any one following this company in the group …

Malolan…

Hello Revisting Himadri Speciality Chemicals …

No updates n this company for a long time…

Any one following this company in the group …

Malolan…

Himadri plans to set up Rs 4,800 crore LFP cathode manufacturing plant in Odisha (moneycontrol.com)

looks like a good plan, with EV going mainstream and sourcing it locally instead of China. Might even get some PLI subsidy too down the road.

Isn’t it a risky spell for himadri entering into this segment?

Cathode materials industry is predominantly led by Chinese players, with a total requirement of 1.4 million tonnes. Himadri emphasises its intention to sell these materials to original equipment manufacturers (OEMs). Contemporary Amperex Technology Co.Limited (CATL) a chinese battery manufacturer which holds majority share in LFP (lithium phosphate battery).

Major opportunity is there for this company but if any renown Indian brand comes into picture from the same serving segment as well it can be a major threat as well.

Well, you have to name the reknown brand and whether they have a plan for it. There’s Reliance trying with Sodium ion tech , and who else?

HBL power is one of them which already manufactures LFP as well as NMC batteries.

read this to understand other Indian companies capex.

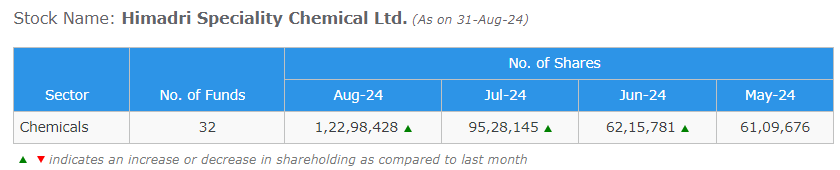

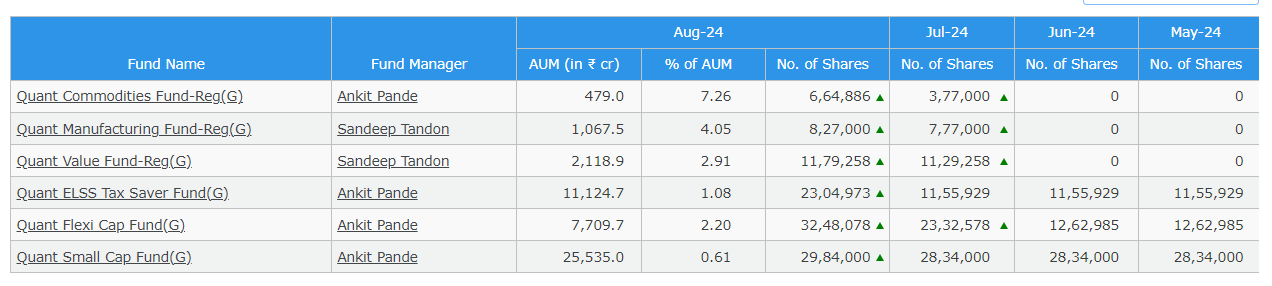

Additionally, Many Quant funds hold position in HSCL and all of them increased the stake in August.

Discl: Remain Invested. Invested @490 Levels.

Since the threat has been not active since long, I thought of putting up some summarised notes of my here, much of it derived from the links and discussions shared above and the investor ppts of HSCL.

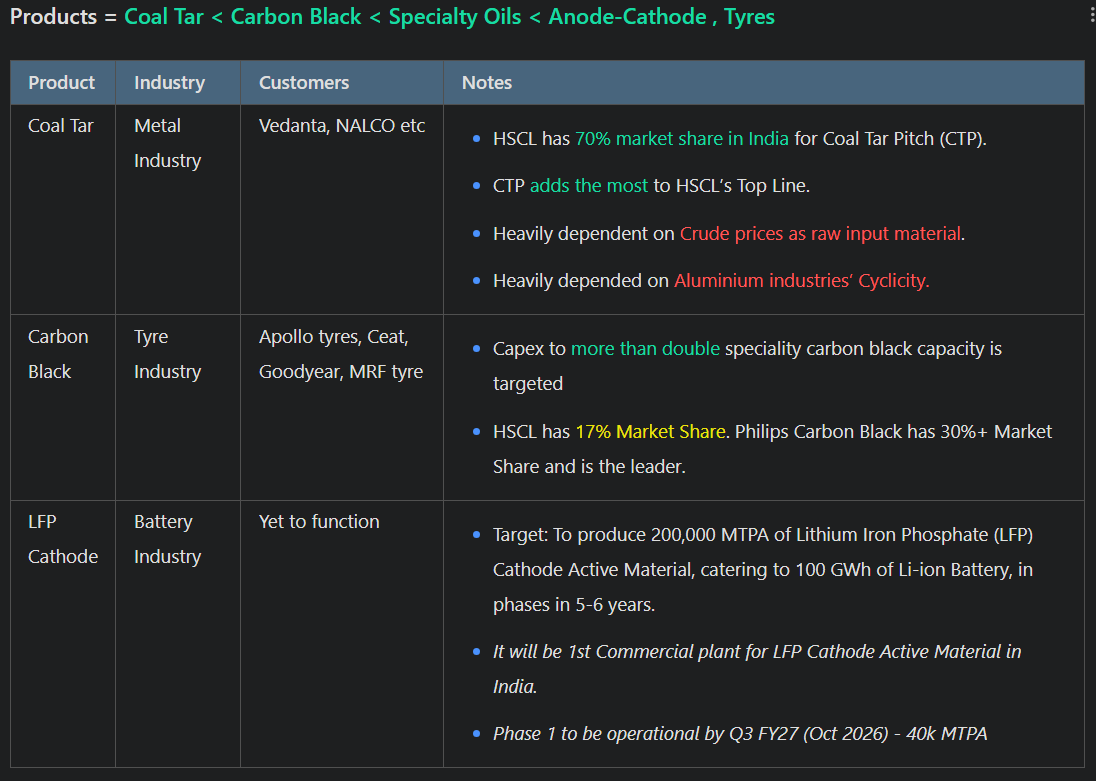

Products

Products Analysis

Peer Comparison

Management:

Shareholding Trends:

Thats it. I am looking forward to sharing more as I keep tracking the stock. I remain invested in the stock since a month or two at 490 Levels. Looking forward also to get more insights from fellow folks who are tracking it!

Thanks for reactivating the thread. Just wondering what was your rationale for investing?

Looking at the historical price chart of HSCL, it has seen significant price action since its post Covid recovery and even after an impressive 35% YoY increase in PAT for 9MFY25, its TTM PE is 52. I’m guessing when you entered at ~490, the PE was at similar levels.

Disc: Not invested