This is my opinion if someone knows this company very well then only venture in it. Otherwise you can make handsome returns from the well known stories.

The stock has shown upward movement today by almost 10%.

I think integrity of management is probably not the best but its a fact they have grow from a single product company to reasonable portfolio in 10 years and I am not sure why they cant do it again.

Also during these period stock price also had grown substantially.

Hi

management never said that they will produce Li Ion batteries . Never mentioned in previous AR. However ACM and SCB have been core strategy to move into value added products and hence improve GM of the company.

what happened with LiIon battery thing is market rumor mills in my opinion.

Further , plan for 60,000 Tons capacity of SCB is done and production has started already in Q32021.

if you see the accounting note you will read a statement to that effect.

However, i was not aware of this related party transaction either… + this claim of 41cr is not very clear as well.

In Q32021, Company wrote of 75Cr + another 52Cr due to bad biz decisions of venturing into China.

Capex allocation has not been very prudent going by above examples.

I have invested at 2020 lows due to ACM in particular and the fact the SCB has started improving margins per ton of production already in FY20 itself. ACM will show lot more improvement into GM however they postponed the project in 2020 due to Covid and I am not sure if they restarted or not.

I also noticed that company recently (last 10 days) issued commercial papers for 60Cr Rs. this can not be working capital alone (way too high for that) , so I expect some Capex out of this.

Disc: Invested . With recent events, does not trust management fully anymore. there is lack of communication from the company.

1 Like

Just one clarification as my post might be bit misleading.

Company already produces ACM - however not with enough capacity that it can make a significant contribution to top line. Same with Specialty carbon black - 4 grades are being produced with 20lTons of capacity. Company announced that they will expand capacity of ACM to 20k Tons and SCM by 60k Tons. out of which SCM was still continuing and ACM plan was postponed…

Check the Q3 investor presentation here

Sorry could not find any details of the sort mentioned in the post in the attached presentation. Could you post a screenshot showing the same? Thanks!

SCB = Specialty Carbon Black

ACM = Advanced Carbon Materials

Disc: not invested

I think I was not clear in my earlier post. I meant the management talked a lot about ACM and its future growth on the basis of Li ion batteries/EV industry which is projected to be a very high growth industry. The company has not released info on the projected capex plan on ACM capacity or current capacity to gauge company’s progress.

The issues with its China subsidiaries were mentioned in the 2020 AR as well.

1 Like

The AR 2020 states the SCB capacity already at 60k MTPA.

The PPT you shared doesn’t have any capacity info. Can you share a screenshot of what you were refering to?

Disc: Not invested

Does the company ever respond to the queries?

I have been sending them multiple mails to conduct concalls and/ or provide response to the queries. I havent received any response

Disc: Invested at 89.00 and still holding.

company responded saying they always update investors via SEBI disclosures and other material updated in their website…  Did not answer my specific query about the ACM capacity expansion project.

Did not answer my specific query about the ACM capacity expansion project.

However, got information from an employee that

a. ACM biz group is developing customers for MP Coke (used in Anode)

b, company is also manufacturing anodes for battery in trial phase. no launch yet.

Disc: Invested from lower levels.

2 Likes

HSCL is not entering battery vehicles. its a sister company that has no financial linkage to HSCL. Barring good updates by management, this bits and pieces of information only confuses us all.

For their sister concern , Motovolt mobility, they have said that they are importing battery cells from china. But they have also made statements that they are exporting anode material in small quantities to China/Korea. So, the complete LiON battery manufacturing is not in scope. Inputs/ingredients to LiON batteries like anode material is the only growth prospect.

1 Like

This is the problem with this management, the communication process is close to Zero with investors. We all are in the dark as to what the company is going to do over the next 2-3 years or so and what sought of capital allocation they are going on make in the ACM segment.

Wish I could connect to the management in some way.

1 Like

100% agree with you. IR team replied to my enquiry and talked about Management sharing information already… i dont find it anywhere.

1 Like

But, now it looks like industry dynamics are changing

CTP prices up more than 30%

Graphite Electrode prices up more than 20%

Should augur well for our subject company.

The company has recently raised monies aggregating to Rs.60.00 crores as per BSE filings, which I have a gut feeling that they are going into business operations in view of improved business conditions.

Please note that company has lower utilization of its cash credit limit too, such type of raising monies means, they are running short of capital with improved business conditions.

Expect bumper results in next 2-3 quarters. I think a business bottom is in place.

Believe me, once the business prospects improve, the management will start conducting con calls.

2 Likes

e3544e5e-230d-4567-8111-99b13a324992.pdf (bseindia.com)

The year end numbers are just about the same as FY20 or less. Don’t see any extraordinary pick up as there seems to no new launches or client signings.

Have a small tracking position on this

For a company to be able to say that they deal with Advanced Carbon, they should walk the talk and show investment in R&D rather than repeating “R&D” in their annual report. There are no patents to show for their so called specialty. Hence till the time the company / management walks the talk and shows some technology that actually deals with advanced carbon, they will be an ordinary coal tar pitch player where margins are low.

Second , there is another issue about related party transaction - I mean why does the company have to deal with an interested party to begin with to construct key places like factories etc. Not that there is a dearth of people who provide these run of the mill services such as construction.

Third, they are in a state where there are major labour problems only a few of which come to fore and only if one knows where to look for.

Till they take care of these issues, in my view, this company will be in the doldrums and the market rightly reflects it in the stock price.

Rechecked again. This is not spam and nor am I promoting anything.

7 Likes

Very Strange, the FII and DII have added or increased their position. Though the company refused any work around lithium ion battery swapping technology.

1 Like

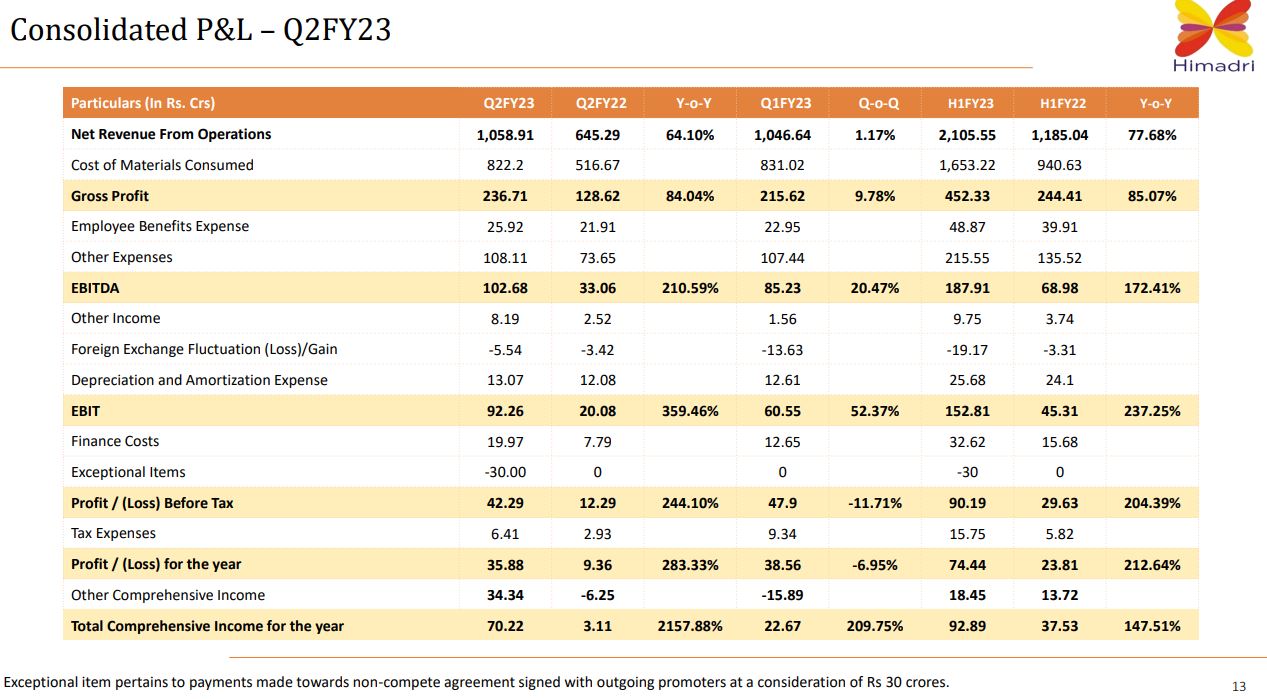

decent numbers… dimmed by forex losses and one time exceptional items…

"Exceptional item pertains to payments made towards non-compete agreement signed with outgoing promoters at a consideration of Rs 30 crores. "

Invested recently

2 Likes

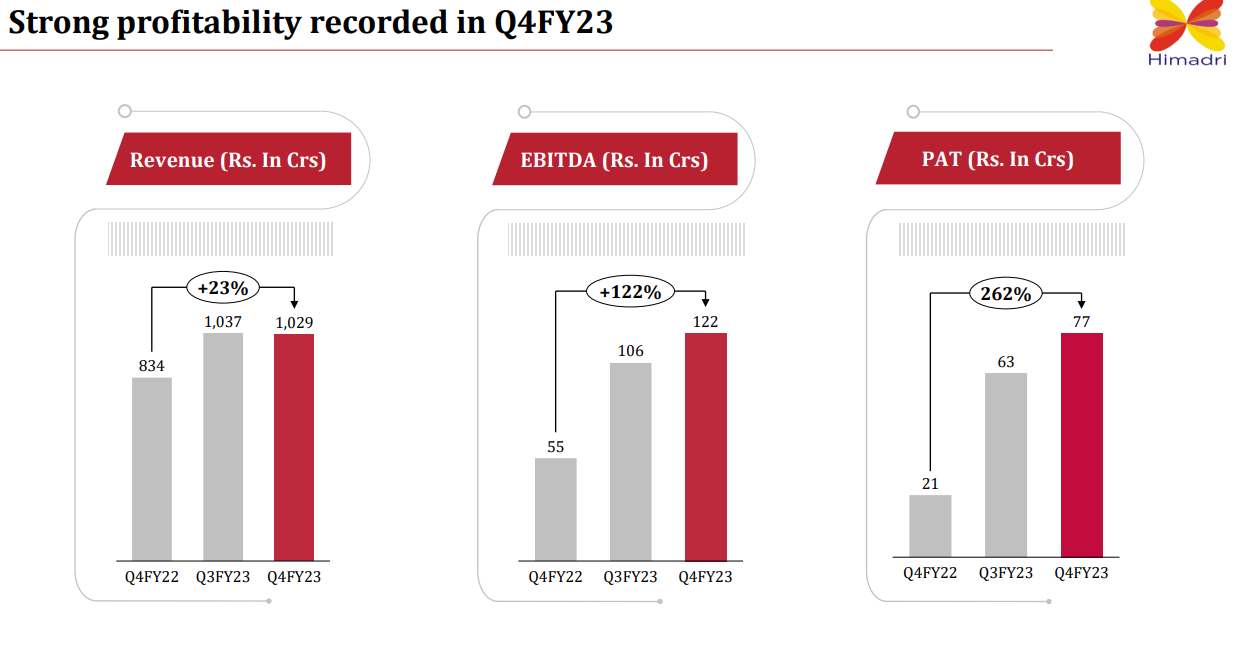

resuts keep getting better and better…margin expasion like the past upcycle…

an year before election & ifrastructure will be the theme…

Invested 5% of portfolio