Himadri is a Kolkata based company mainly focusing on coal tar pitch and carbon black.

Product chain

Main Products

Coal tar pitch:

- used in the manufacture of aluminum, which is used in automobiles, airplanes, televisions, radio components, rockets, beverage cans, wires, cables, smartphones, furniture, foil wraps.

- finds downstream use in the manufacture of graphite electrodes in electric arc furnaces.

- specialized coal tar pitch, which is used in long war head missiles.

- manufactures coal tar-based thermoplastic polymeric coating, which is used as an anti-corrosive material in underground and offshore pipelines.

- Coal tar distillation capacity is 4 lakh MTPA.

- 70% market share

- Debottlenecking of capacity at 20cr planned to increase capacity

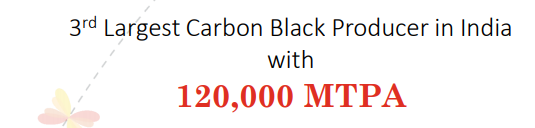

Carbon black:

- used for reinforcement of elastomeric materials. Carbon black is a critical raw material in tyre and other rubber industries, inks, plastics and paints.

- manufactures a range of specialty carbon black with specific applications in plastics, fibre, inks and food grade materials.

- Carbon black capacity - 1.2 lakh MTPA

- 17% market share

SNF:

- manufactures SNF (Sulphonated Naphthalene Formaldehyde), which enhances the performance of concrete for commercial and core infrastructure constructions.

- manufactures PCE (poly carboxylate ether) which is a performance chemical used in next-generation super-plasticisers to manufacture high-strength, high performance concrete.

- Dumping from China poses a threat

- SNF capacity - 68,000 MTPA - Largest capacity in India

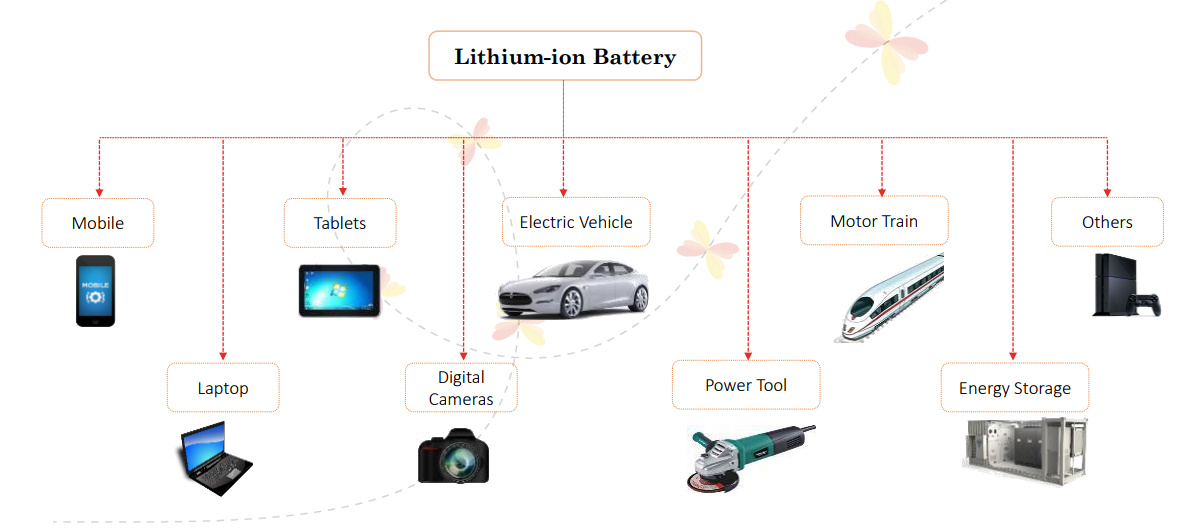

Advanced Carbon (Anode for Li-Ion batteries):

- manufactures advanced carbon used in the manufacture of lithium-ion batteries that power smartphones, electric vehicles and digital cameras as well as airplane brakes that make flying safer.

- The consumption pattern of anode materials are slowly shifting from natural to synthetic graphite. Himadri offers anode materials in both synthetic and natural varieties.

- Co is the only company in the world to have in-house access to raw material making its products superior in quality.

- Moved from batch processing to continuous processing.

- Current capacity is 5 MT/month. New capacity of 50 MT/month coming onstream from 15 Sep 2017.

- Expected CAGR of 40%; no need to have firm contracts as demand is huge

- Realizations are 6 lakhs - 7 lakhs / MT for the finished product.

Plants:

Himadri has seven manufacturing units across India – four in West Bengal and one each in Andhra Pradesh, Gujarat, Chhattisgarh – and is now setting up its eighth unit in Odisha. The Company exports products to more than 10 countries.

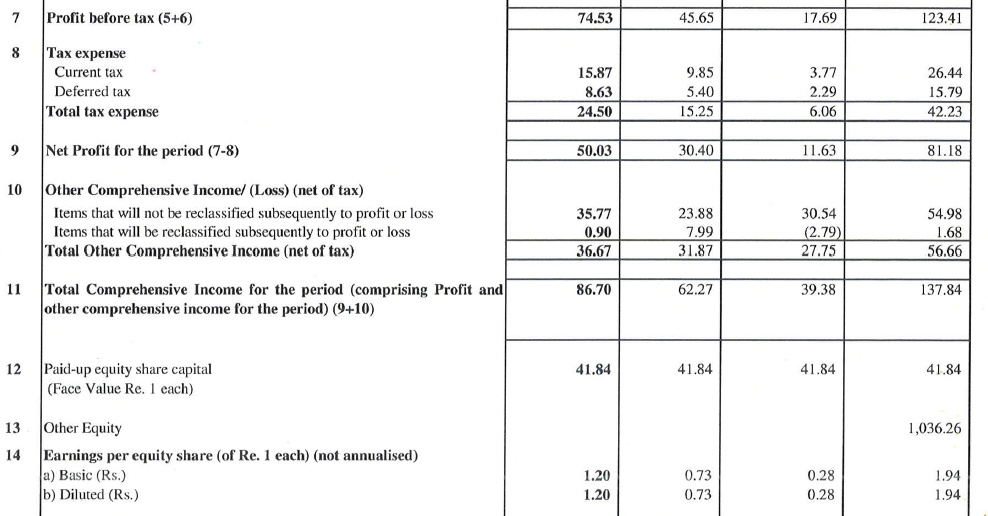

The Company had been incurring losses during the last three years, even though at the operational level, they reported profitability. Primarily, the losses that the Company incurred were due to a depreciation of the INR and inventory losses on account of fall in the price of crude oil. The inventory pileup continued during the first two quarters of 2016.

The co took measures to reinforce operational efficiencies; appointed a consultant with global expertise to help us incorporate best-in-class practices.

The business model is unique and fully integrated to manufacture speciality chemicals. Use coal tar as the raw material and distill it to produce naphthalene, oils of various grades and coal tar pitch. The naphthalene produced is used in-house to manufacture SNF and refined naphthalene of the highest purity. Heavy creosote oil is sold to customers for specialised applications while other oils are used for making carbon black. We also produce

clean and green power. The power generated is used to power the entire complex while the balance is sold to the State Grid.

Inelastic Demand:

Aluminum smelters cannot moderate consumption during a downturn without having to shut down one (or some) of their manufacturing units. The cost of shutting down and starting afresh is too high. This means that coal tar pitch manufacturers are assured of regular offtake in even the most challenging

of markets. The strong offtake across the last two years, when aluminum and graphite industries were going through their worst phase, stands testimony.

Reason for decline in the Company’s earnings in the last 3 years:

- INR depreciation

- inventory losses due to fall in crude

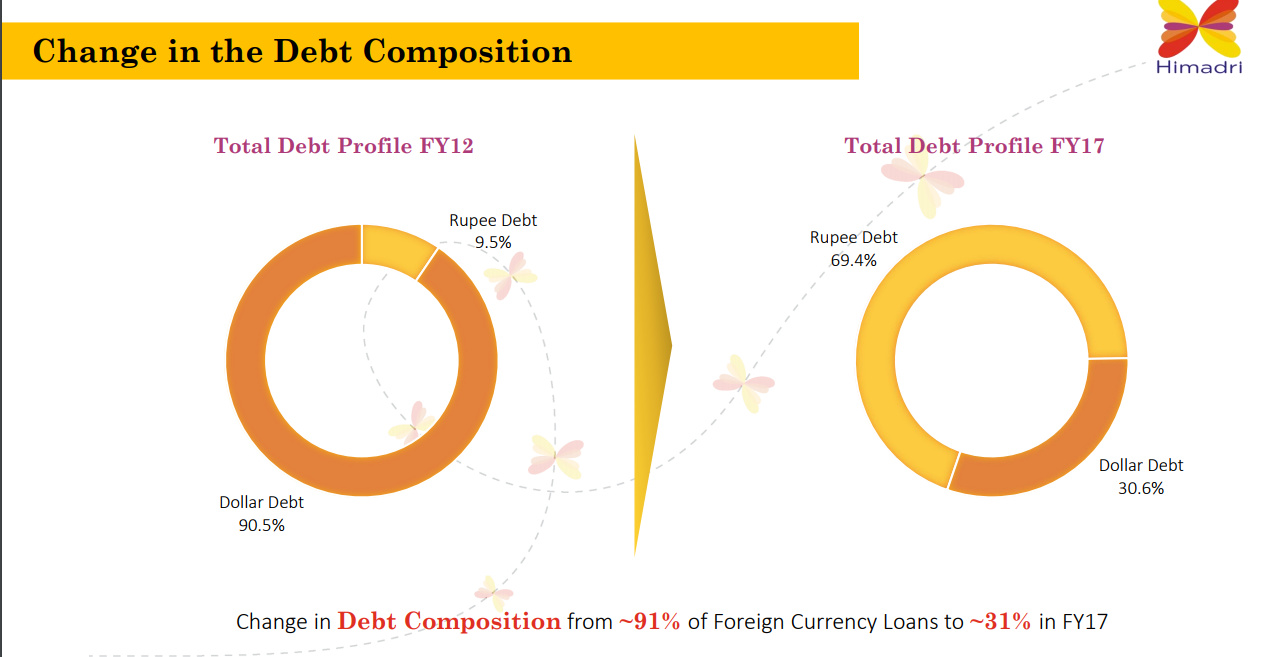

What has changed:

- reduced its exposure to foreign currency loans

- debt reduction

- net debt of the company reduced by 225 Crores during 2015- 16, including the repayment of long-term debt of 122 Crores, even as the financials appeared stressed.

- LT debt reduced from 414 cr in 31-Mar-17 to 310 cr on 30-Jun-17, reduction of 104 cr.

Non-promoter holding:

- Bain Capital

- Vallabh Bhansali

RISKS

- The profitability of the company is susceptible to volatility in raw-material prices (forming 85% of total cost of sales) as the prices of raw-material are volatile in nature due to linkage with crude oil prices and global demand and supply.

- The company is also exposed to foreign exchange fluctuation risks due to high dependency on imported raw-material, foreign currency term loan and no fixed hedging policy.

- HSCL’s operations are working capital intensive due to requirement of high level of inventory on the back of lead time involved in import of few raw-materials (imported pitch and carbon black feedstock) and high credit period offered to its customers.

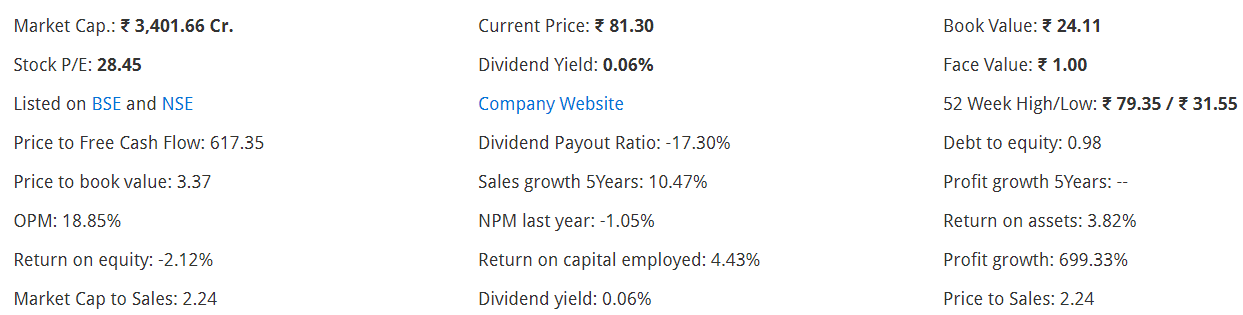

Financial Ratios from Screener

Disclosure: Not currently invested.