Question 1 - Answer : Considering HFCL’s product offerings, its competitors can be classified based on the segments it operates in:

Telecommunications Equipment:

Sterlite Technologies Limited

Tejas Networks Limited

Tata Communications Limited

Bharti Airtel Limited

Vodafone Idea Limited

Optical Fiber Cable (OFC) and Optical Transmission Equipment:

Sterlite Technologies Limited

Aksh Optifibre Limited

Finolex Cables Limited

Vindhya Telelinks Limited

Defence Electronics:

Bharat Electronics Limited (BEL)

Larsen & Toubro Limited (L&T)

Rolta India Limited

Bharat Forge Limited

Railway Communication and Signaling Systems:

Siemens Limited

Bharat Heavy Electricals Limited (BHEL)

ABB India Limited

Alstom India Limited

These companies compete with HFCL in their respective product segments, offering similar products and solutions to cater to the telecommunications, defense, and railway sectors.

Question 2 - Answer:

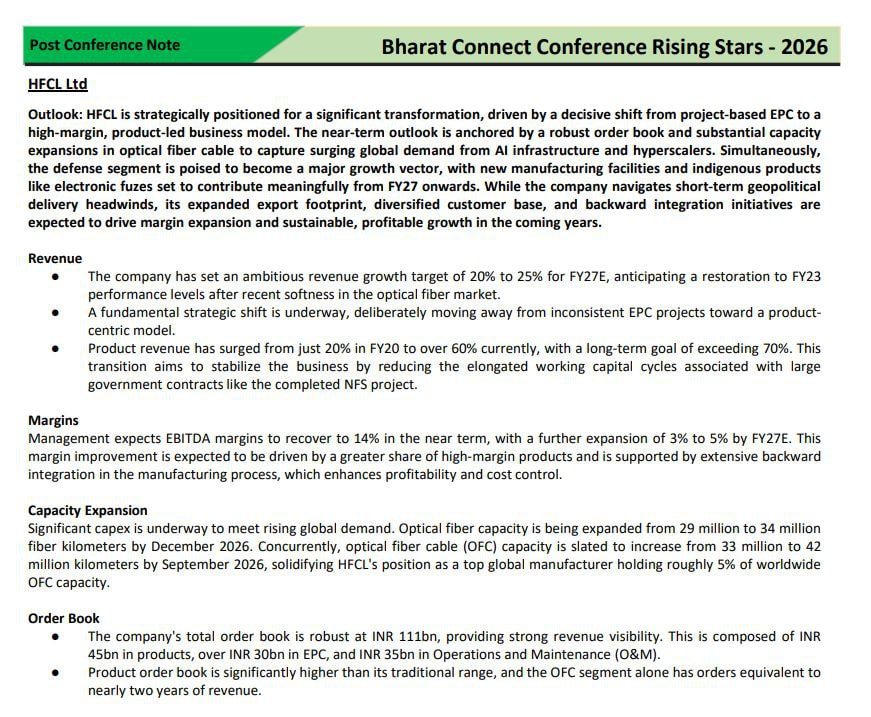

To analyze the trends and outlook for HFCL’s focus market segments (optical cables, 5G products, defense fuse, and defense optics) for the upcoming years, we need to consider various factors:

5G Products and Optical Cables:

Trends: The deployment of 5G networks is expected to accelerate globally, driving demand for related infrastructure such as optical cables, fiber optics, and network equipment.

Outlook: The demand for 5G products and optical cables is likely to continue growing as telecom operators expand their 5G networks to meet increasing data traffic demands. The adoption of 5G technology in various industries, including automotive, healthcare, and smart cities, will further drive demand for related products and services.

Opportunities: HFCL, as a manufacturer of optical fibers and cables, is well-positioned to benefit from the 5G rollout. The company can capitalize on the growing demand for high-speed, low-latency connectivity solutions.

Defense Fuse and Optics:

Trends: Governments worldwide are focusing on strengthening their defense capabilities, leading to increased investments in defense modernization and indigenous manufacturing.

Outlook: The defense sector’s emphasis on self-reliance and indigenous production presents opportunities for companies like HFCL that offer defense-related products such as fuses and optics. With rising geopolitical tensions and security threats, governments are expected to prioritize defense spending, driving demand for advanced defense technologies.

Opportunities: HFCL can leverage its expertise in manufacturing defense-related components to cater to the growing demand from defense organizations. By focusing on innovation, quality, and timely delivery, the company can secure contracts and partnerships in the defense sector.

Overall Market Dynamics:

Trends: Rapid technological advancements, increasing connectivity needs, and evolving security challenges are shaping the market dynamics in HFCL’s focus segments.

Outlook: The outlook for HFCL’s focus market appears positive, with sustained demand expected in the coming years. However, the market is also competitive, requiring HFCL to continuously innovate, invest in R&D, and forge strategic partnerships to maintain its competitive edge.

Opportunities: HFCL can explore opportunities for diversification, expand its product portfolio, and enter emerging markets to drive growth. Additionally, the company can leverage government initiatives supporting domestic manufacturing and defense self-reliance to enhance its market presence.

Additionally as HFCL mentioned that Bharat- Net III and other global opportunities which they are always seeking does show that this sector will have tailwinds. We will have to see how it unravels.

News > (https://www.bseindia.com/xml-data/corpfiling/AttachLive/c02b4931-d172-44e9-983d-1f1cca067207.pdf)

Now it establishes HFCL UK Limited to manufacture and trade Optical Fiber, Optical Fiber Cables, Telecom and Networking Products, and related activities. They say this will help the company meet global demand and expand overseas. This aligns with the company’s strategy to increase export revenue, enhancing its presence and fostering growth opportunities.

What and how much is HFCL exporting to the UK at present?

Is this news just a “feel good” point, or does the company have any meaningful export business right now?

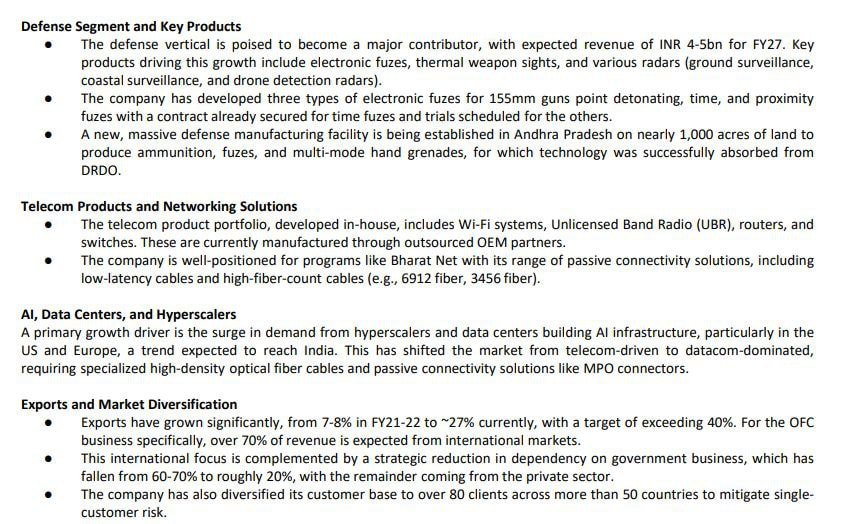

Developed 12-micron Ti-core based thermal weapon sights for defence forces.

Developed ,high accuracy, ground and coastal surveillance radars using Frequency Modulated Continuous Wave (FMCW) technology.

Shortlisted for upgrading BMP 2/2K armaments.

Question is how much is contribution these products are making to the revenue ? if these are not just PR and are yet to be ordered by india defence then it might have long way to go ?

Fiber Optics Demand: The company expects demand for fiber optics to pick up from Q4.

Capacity Utilization: Anticipates increasing capacity utilization to 80%, up from the current 40%.

Defense Sector Revenue: Revenue from the defense sector is expected to start contributing from Q1 next year.

U.S. Projects Participation: Participating in both BEAD (Broadband Equity, Access, and Deployment) and non-BEAD projects in the USA, with non-BEAD projects being significantly larger than BEAD projects.

Telecom Products Revenue Guidance: Expects telecom products revenue to reach ₹2,000 crore this year. With a current order book of ₹900 crore and around ₹1,000 crore already recorded as revenue, the company is confident of meeting this target.

Long-Term Revenue Guidance: Maintained a revenue guidance of ₹10,000 crore over the next three years, implying a CAGR of 25-30%. This growth is expected to reflect in EPS from next year onward.

Revenue Ratio Target: Aiming for a 2:1 revenue ratio between Telecom and Defense sectors by the end of three years.

BharatNet Contract: Expects the BharatNet contract to be allocated by Q1 next year.

Increase in Finance and Employee Costs: Addressed the reasons for the increase in finance and employee costs from H1 FY24 to H1 FY25. Due to a change in the debt profile and new hiring since Q3 FY24, these costs are trending upward.

Operations & Maintenance (O&M) Revenue: Current O&M revenue is ₹25 crore, expected to increase to ₹300-400 crore by FY27-28.

HFCL an Advance Work Order (AWO) worth approximately ₹2,501.30 crore from Bharat Sanchar Nigam Limited (BSNL).

Project Details: Design, supply, construction, installation, upgradation, operation, and maintenance of the middle-mile network for BharatNet Phase III in Punjab Telecom Circle under a Design-Build-Operate-Maintain (DBOM) model.

Contract Value: ₹1,244.61 crore for capex and ₹1,256.70 crore for operational expenses over 10 years.

Timeline: 3 years for construction and 10 years for maintenance.

Company is raising 555crs by issuance of up to 7,50,00,000 warrants, each convertible into one equity share of the Company, to the Promoters/Promoter Group of the Company at an issue price of ₹74/- per equity share

last month stltech did this and now HFCL something is cooking guys.

company is raising for

Backward integration into preform manufacturing, a critical step towards improving margins and supply chain strengthening.

Scaling up of the defence business, which is emerging as a high-growth and high-impact segment.

Augmenting long-term working capital resources duly aligned with the expansion programmes and incremental revenue.

@Aman_Jain3 So during the making of OFC, the glass used in it is heated to over 2,000°C. For the fiber to maintain its structural integrity and optical clarity, it must be cooled rapidly and uniformly before it is spooled.

And Helium has exceptionally high thermal conductivity. It can whisk heat away from the glass much faster than air or nitrogen.

There is currently no other gas that cools fiber as efficiently and cleanly as helium. If manufacturers can’t use helium, they have to slow down their production lines significantly to allow for slower cooling, which reduces supply.

@Aman_Jain3 So if you switch to a cheaper gas like nitrogen, it cools the glass many times slower. To keep the glass at the right temperature for coating, they have to slow the machine down to a crawl. This creates a massive supply shortage because the factory is now producing 80% less cable than before.

But for certain high-performance cables like HFCL makes for DC and underwater Internet cables, a slow-down isn’t enough.

If the cable doesn’t meet the strict zero-loss standards required for long-distance internet, they might simply shut down the line rather than produce trash cable that no one would buy.

So Overall we have to track the next con call, but simply put

Because helium is a byproduct of natural gas and cannot be made in a lab, when supply drops, the cost of the remaining helium spikes. Then they have to pay 5x–10x more for the gas just to keep their machines running at half-speed. They then pass those costs directly to the telecom companies and DC, who then pass them to us.

Is there a new technology for cooling the cables as soon much new technology is coming up in DC space for cooling DC so there can be new technology or atleast some R&D must be going on.