Company Overview:

Hi Tech Pipes was incorporated in 1985 and is one of the leading steel processing company in India. The company has presence in steel pipes, hollow sections, tubes, cold rolled coils & strips, road crash barriers, solar mounting structure and a variety of other galvanized products. The company has three plants located in Sikandarabad, Sanand (Gujarat) and Hindupur (South) with the manufacturing capacity of 300,000 tonne per annum. The company has pan India presence with more than 200 distributors.

Current Capacity & Utilization:

• Two Manufacturing Plant in Sikandarabad with the total capacity of 1,80,000 TPA operating at 75%.

• Third Manufacturing plant in Sanand with the total installed capacity of 60,000. Out of this 30,000 tpa was commissioned in September 2016. The plant is running at more than 70% utilization since March 2017

• Fourth Manufacturing plant was commissioned in Hindpur, Bangalore in Jan 2017 and is running at more than 70% since March 2017.

• Optimum Utilization is ~80%

Revenue can grow at 35% CAGR led by foray into south and west market

Recently company has commissioned/stabilized the production at two new plants in South and West with the capacity of 60,000 MT each respectively. Both the plants are running at more than 70% utilization since March (optimum utilization of 80%). Demand dynamics in both the markets are good as a result of which company is able to sell full production. Based on this, company is expected to have sales volume of 225,000 MT (75% utilization of FY17 end capacity of 300,000), which would translate to the revenue of 820-840cr revenue in FY18 (YoY growth of 30%).

Further, company is in the process of doubling capacity at South and west plant with the marginal capex (due to brownfield expansion). Expansion in the West and south is expected to be completed by Oct 2017 and Feb 2018 respectively. Post expansion, capacity of both the plant would be 120,000 each and company’s total capacity would be 420,000 MT. Management is confident of achieving 75%-80% utilization on the capacity in FY19, which would translate into revenue of 1100-1150cr revenue in FY19 (35%-40% YoY growth).

So revenue is expected to increase to 1100-1150cr in FY19 as compared to ~640cr in FY17, at a CAGR of ~35%.

EBITDA can grow at 40% CAGR led by revenue growth and margin improvement

As per the company management, margins are expected to increase going forward on account of better realization in south market, Raw material cost saving (proximity to supplier) and economy of scale. This coupled with revenue growth is expected to help company in achieving EBITDA of 80cr+ as compared to 40cr EBITDA in FY17.

Profitability can grow manifold led by EBITDA growth and leverage

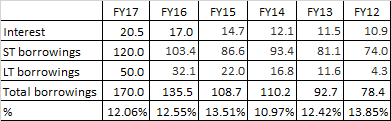

Interest outgo for the company is expected to remain flattish/increase marginally on account of 1) Major part of the Interest already got reflected in the income statement from H2FY17 onwards 2) Interest cost is expected to reduce by 1% due to reclassification of debt in State bank of India books instead of State Bank of Patiala 3) Debt of only 10-15cr for the 2nd phase of expansion. Further depreciation should also remain flattish going forward. This coupled with ~40% growth in EBITDA can help company in posting profit of atleast 20cr and 35cr in FY18 and FY19 respectively as compated to profit of ~10cr in FY17.

ROE to improve on account of increased utilization, margin improvement and operating leverage

Valuation:

On a Trailing Basis, the stock is trading at PE of ~15x vs APL Apollo tube PE of ~26x vs Rama Steel Tube PE of ~27x. Even on EV/Sales basis, the stock is trading at EV/Sales multiple of 0.5x vs sector average on 1x.

On forward basis, the stock is trading at the PE of ~7x FY18E and 4x FY19E earnings as compared to sector forward PE of 15-20x.

Key Risk:

• Delay in expansion

• Economy Slowdown

• Low liquidity in the Stock due to NSE SME exchange

Disclosure: Invested