Good results.

Impressive QoQ and YoY increase in revenue, ebitda, and pat.

~2.5x YOY growth in PAT - value addition gaining traction.

Good results.

Impressive QoQ and YoY increase in revenue, ebitda, and pat.

~2.5x YOY growth in PAT - value addition gaining traction.

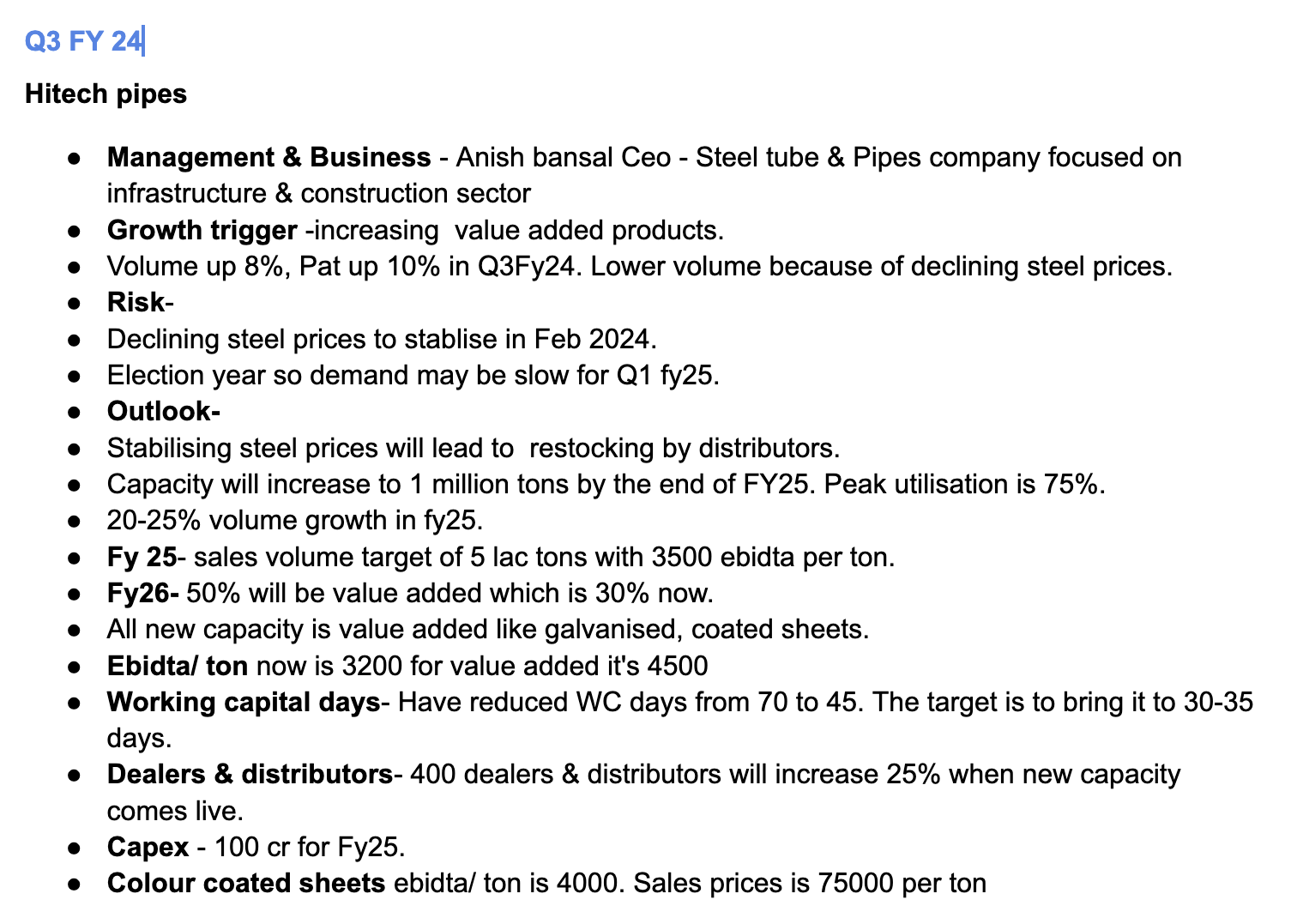

To anyone tracking this company. When the company mentions value added to be increased to 50%. Exactly what does this value add comprise of? Is this the new application in construction business that does 5000 odd ebitda/ton. Or just higher grade core business products. Company never expands on this side.

Have highlighted below the products which would give higher EBITDA/ ton. There is a lot of scope for improvement, if you compare with APL, and they are on the right track.

Volatility in steel prices could play spoil sport so suggest watching out for the same.

Hi-Tech Pipes Limited reported results for Q2FY25:

• Sales Performance:

• Profitability:

EBITDA increasing 58% YoY

EBITDA per tonne was Rs 3,429, up 29% YoY

Adjusted profit after tax (PAT) grew 72% YoY

Strong volume growth offset by lower realizations

Operational efficiency gains helped maintain EBITDA margins despite falling HRC prices

Company demonstrated resilience in managing inventory losses - Can fellow VP members shed light on how Hi-Tech pipes managed lower inventory losses than APL APollo?

Capacity upto 1 million tons

HRC prices have increased by 5-6 rs in spot market

Great volumes

Looks like a turnaround in making

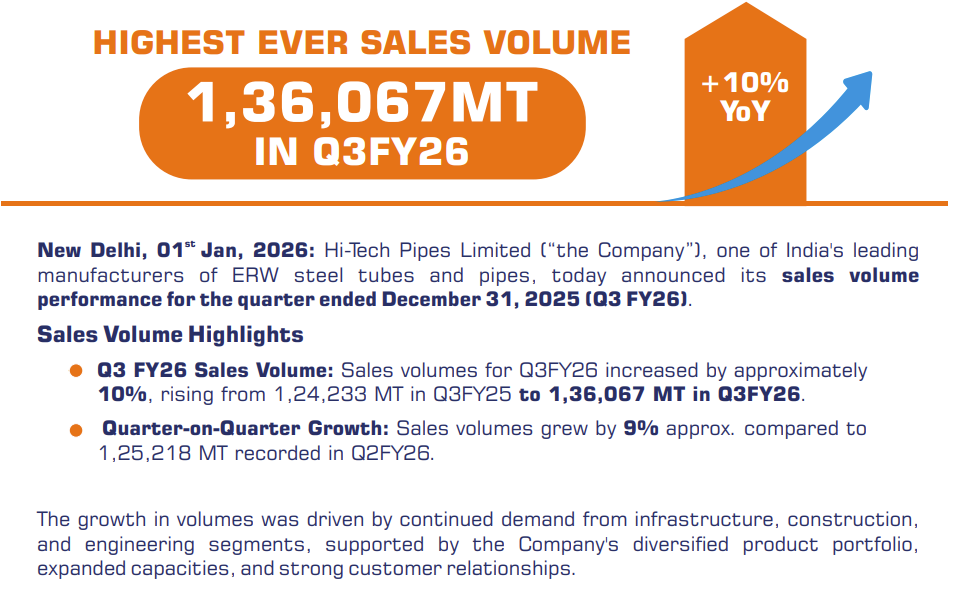

Highest ever sales volume. 9% QoQ growth in volume. Deepening value added portfolio.

Capacity expansion - 850K MTPA; on track to achieve 1M MTPA.

HRC prices most likely to go up - India has imposed a three-year safeguard duty of 12% on steel imports.

Might have some inventory gain in Q3

Available at PE of < 25; market cap/ sales at 0.6;

Bandhan picked up >6% stake around 90rs in Q2/ Q3.

Disc. Invested