I am finding it difficult to understand the future retail part starting from page 14 of the con call. Could you please explain it in simpler terms about the future retail part. Thank You.

Heritage Foods has a Profit Sharing agreement with Future Retail for their stake. If Heritage sells their stake in FRL for a profit, they have to share a percentage of the profits with Future Retail. This is being recorded as a Derivative Transaction in the accounts of Heritage Foods. The details of the agreement are given in my previous post.

In related news:

2 Likes

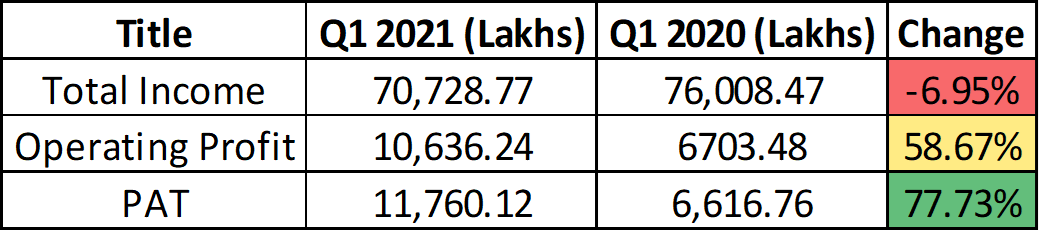

Quarterly Results

Very good Q1. The below numbers are excluding any gains / losses from the FRL hedge.

(Source: https://www.bseindia.com/xml-data/corpfiling/AttachLive/94401e45-0f85-4a3b-ae11-34f5ee01934d.pdf)

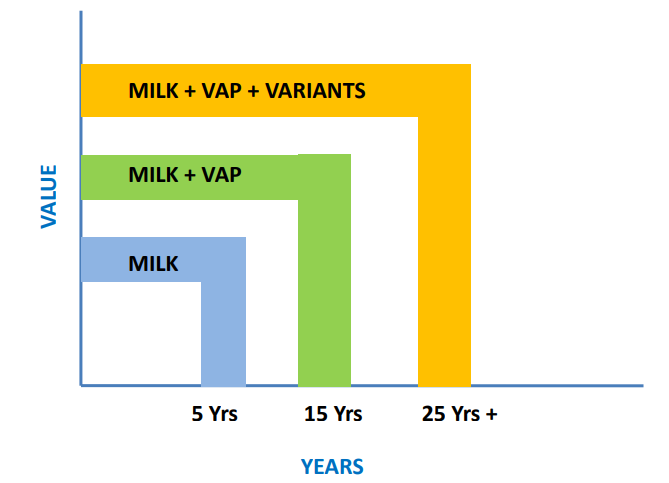

Investors Presentation

This simple graphic from the investors presentation showcases my investment thesis for Heritage very well. They will continue to derive value from Milk. But a bulk of the additional value created will come from VADP and other related products for the next decade.

(Source: https://www.bseindia.com/xml-data/corpfiling/AttachLive/fc810347-c742-4cc7-90fe-e65e57ea445c.pdf)

Digital Marketing

Also, I should appreciate Heritage’s digital marketing campaigns.

YouTube (4k subscribers): https://www.youtube.com/channel/UCPH0y1j4tFk5HJFhIknehow

Their ‘Heritage Bytes’ videos have crossed multiple lakhs of view each, with Episodes 9 and 10 having close to a million views. This is a very good way to introduce new products to the younger generation.

On top of this, they have been running campaigns on Twitter and Facebook with a lot of success (More success on Facebook than on Twitter).

Annual Report

Annual Report is also out, but I have not gone through it yet.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/aaf1fd77-69f6-4319-b656-5b7c766c6825.pdf

3 Likes

Some questions I am looking for answer

-

Why Heritage is not able to grow much in last two years while co-operatives like Amul are able to grow decently even on higher base. Is there any structural issues that are causing co-operatives to grow while private players are not able to grow.

-

What is the present financial status of recent acquisition of reliance dairy. Have they broke even? Why this acquisition is even not helping in increasing top line?

-

What is the present status of Maharastra plant. When are they going to start operations?

-

How are the digital promotions are helping to increase presence?. Though it is good way to increase the brand visibility but there are no signs of contribution in sales so far.

-

Is there any collaboration with reliance retail and future retail to have exclusive brand promotion (they had connections with future retail after selling heritage fresh and with reliance after acquiring reliance dairy) Big bazar is used to promote Heritage milk with exclusive offers. As reliance retail is expanding with Jio mart, will it help heritage in any way?

I am yet to go through Q1 concall transcript and annual report.

Disclosure: Invested

The difference is that Heritage was purely into Milk and more so only in 1-2 regions, which had a glut scenario in 2 out of the last 3 years. The diversification into VADP couldn’t have come at a better time.

I remember in the concall, they said they will not be able to give separate numbers anymore because it is all integrated (Or maybe they didn’t want to give it out due to competitive reasons - I forget exactly).

Last year, construction was delayed due to heavy rains. Target was pushed back to July 2021. But I am guessing it is still not done because of COVID19.

This is a very new thing - just 1 year or so into the better campaigns. We will see the impact only after a good 2-3 years.

Good question. But we may have to wait for the answer.

1 Like

Heritage to sell stake in Future Retail and Praxis Home Retail.

Sound decision in my opinion. Now the management can focus on the core business. Hopefully they’ll utilize the proceeds to fund further Capex or reduce Debt.

1 Like

AGM was uploaded in YouTube this time. Pretty good if they’re going to keep this up.

1 Like

Did d sell take place of future retail or ist still pending

Or is d selling of stake over or not sir as of now…

Most likely over. We have to wait until the next Balance Sheet update to be completely sure.

In one of the past concalls, the management said “net benefit of converting to milk powder minus the losses from fat is something that will always remain negative normally”

Does that indicate, fat based products (ghee, butter) are loss making to the company ?

Why does the company then produce fat ? Is it only to support farmers in case of surplus milk supply

How do u c company going fwd as it’s stuck in a narrow range …and u feel dey will sell d whole stake dey had in future retail shares as that selling also will be bought by retail retail as dey have taken over d company now.

I think currently all VAD Products are making losses or very little profits. The aim was always to get to a 40% Sales mix and then maybe they will consider trying to get the Margins back.

If you’re asking about the share price, then I have no idea. I am poor in Technical Analysis.

I know they have sold the FRL stake. The official confirmation is already out. We can verify the claim by seeing the next release of the Balance Sheet.

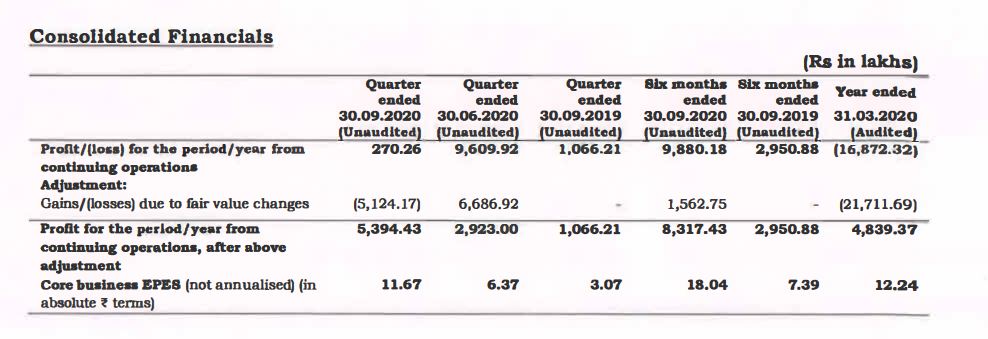

Wat a fabulous set of no’s. on margins front.

I have excluded losses due to sale of FRL STAKE which has impacted overall no’s

Rev down 10% - 610crs

Ebitda - 89.35crs vs 25.23crs

Ebitda % - 14.65% vs 3.71%

PAT - 54crs vs 14.29crs

EPS - 11.67 vs 3.07

Although these margins doesn’t look sustainable at all. Improved GM might be due to extremely subdued raw mat prices.

@dineshssairam your views on the results? as u might be actively tracking it.

1 Like

Actual Core Margins are closer to 9-10% and it’s mostly been due to the reduction in Production Costs. As you said, this may not be sustainable. By the way, Hatsun also has a good quarter because of this.

Revenue drop may be due to COVID-19. But it’s disappointing that all that marketing for VADP hasn’t helped the Sales numbers. But their ongoing Technology overhaul and Social Media campaigns are interesting and warrant tracking at least.

Capital Work in Progress has increased, as expected. I’m assuming most of the work is still stagnant due to COVID-19, since Depreciation has reduced despite the Capex.

Looks like they sold off the FRL stake finally. There has also been a significant reduction in Debt (Which I presume is from the proceeds of the FRL stake). Excellent use of Capital here. D/E is below 50% now (You can also see the reduction in Interest Paid).

Ultimately behind all the bells and whistles, they’re well behind on their target to achieve 6,000 Crores in Revenue by 2022. It’s impossible to achieve now. Even if we give 2 additional years on account of delay in Mumbai construction / Mumbai rains and COVID19, it’s still a tall ask to do 2.5x Revenues in 4 years.

I’m still positive here because my expectations of VADP ramping up is going on as expected. The management seems to be good at allocating Capital, as evident by the FRL stake sale (Regardless of the price drop - no price anchoring bias) and subsequent reduction in Debt. Other positives I didn’t expect are the technology overhaul (Including an App) and the social media campaigns.

5 Likes

Stake sale finally happend today with d stock locked up at 20 percnt if dey reduced 131 cr debt how much more is left and how will d stock reacted going fwd

1 Like

We didn’t know why the stock fell so much in March. We also didn’t know why it recovered 100% after. So we shouldn’t pretend to know about this 20% rally or any future price movements as well.

Let’s stick to Fundamentals. As I already mentioned, I think selling the stake was a great move which clears up more space for the management to focus on the core business.

2 Likes

The fortunes of Heritage are tied little bit with Andhra Pradesh Politics (as per my opinion). There is an acrimonious cold war going on between AP ex CM Nara Chandrababu Naidu (His son & Daughter in law are promoters of Heritage) & AP CM Jagan Mohan Reddy. The AP govt is trying to bring in Amul to Andhra Pradesh by which they are promising 4-7 rs extra income to cattle farmers per litre milk. Also, the govt is trying to revive the milk cooperative societies, which might hurt heritage. So, there is lot of uncertainity & at the moment the govt is not unpopular (hence the chances of Chandrababu coming back as CM are not bright at the moment). So, Heritage has tough battle to fight and come out of.

Discl: Not invested & not much idea about the Heritage’s underlying business fundamentals. Just my 2 cents as distant observer.

7 Likes