Hello,

Would love to know your thoughts on Heritage results.

Thanks

Hello,

Would love to know your thoughts on Heritage results.

Thanks

It seems like they have decided to give up Margins to capture Market Share. Generally a good strategy for new entrants. In that light, the results are not so bad (Although, yes, a little disappointing). The Revenue growth is promising.

VADP as a percentage of overall Revenues is about 25% now. They have also recently taken to online campaigns like the “Heritage Bytes” one on YouTube with celebrity chef Bhakti Arora:

(Both the videos have a respectable view count of 220k+. Some of the views and most definitely many of the comments might actually be because of the prize giveaway the company has been conducting on FB / Twitter / Instagram)

I have not listened to the concall yet. I will update further comments if I have any.

I was on the call when Mr Rao was answering questions related to margins. He said that there has been a rise of about 11% in procurement costs. This is primarily due to the irregular monsoons this time which have caused availability issues.

As a strategy, they passed on only half the increase to the consumers (price hike). This should get compensated in the next quarter when there will be an availability surplus and the procurement prices will go down. Overall for this year, they think the margins will be approx 100 bps lesser than last year.

My personal opinion is that we cannot derive much from the quarter results for such a business.

It is not surprising as this is not an industry with ny players having pricing power. Milk powder price fluctuation is something which is not new and if one tracks dairy companies for more than 5 years , he would have witnessed. Usually, whenever it has happened, company is not able to pass it fully n hence if we break the historical nos purely for dairy we can see margin fluctuation , so, whatever they said made sense. The only thing I found amusing was when it came to milk powder n milk prices they gave extended summer being the reason for raw material cost rise but when they were asked for subdued curd sales, they said too much rain n hence demand yoy was not good. The only possibility i see extended summer in specific states n rain in specific states. Hope i heard it properly. Disc : no investments

Short clip explaining where the RCEP stands. We’ll get to know India’s decision very soon.

Edit: Just listened to the concall. Someone asked a question about RCEP. So there is certainly a widespread concern about diary products being included in the RCEP agreement. It looks like the companies can take a price hike without hesitation, but the farmers will be impacted a lot. Let’s hope for a positive verdict.

But there is a more specific concern about New Zealand dumping their goods in India. We will have to wait and see how this will unravel.

Update:

Dean Foods U.S

Quote

Dean Foods, America’s largest milk producer, is filing for bankruptcy.

The 94-year-old company has struggled in recent years because Americans are drinking less cows milk. 2019 has been particularly brutal: the company’s sales tumbled 7% in the first half of the year, and profit fell 14%. Dean Foods stock has lost 80% this year

The company, which produces some of the country’s most recognizable milk and dairy products, including Dairy Pure, Organic Valley and Land O’Lakes milks, has blamed its struggles on the “accelerated decline in the conventional white milk category.”

Would like to share an observation regarding quality of milk Heritage provides.

In Punjab ‘Verka’ has a quite good repo n its n old cooperative brand.

I was at a reliance retail store which sells both VERKA n DIARY LIFE brands of milk. But to my amazement all the crates of Verka Milk were full ( Unsold) whereas all the crates of DIARY LIFE brand was empty ( SOLD out), which was quite strange considering the brand value Verka holds in Punjab.

Enquired the same with employees n they confirmed that customers prefer Diary Life over Verka bcoz of quality of milk n all the milk is sold out within 1.5hrs. Price point being the same for both brands.

N it was opposite last year, Dairy life milk pouches remained unsold till night n Verka used to stock out.

Don’t know how this change happened, but really a positive development.

Though its a very small sample size of just one retail store and their milk is still not available in local kiryana stores all over the state whereas Amul n Verka has quite strong distribution network.

Would request forum members from southern states kindly share your feedback regarding Heritage products as they are easily available there.

Disclosure: Invested

In South, the Co-operatives have an absolute strong-hold. I can personally vouch for Aavin in Tamilnadu and Milma in Kerala having a far better brand recall than Aarokya and Heritage put together.

But some trends I have seen is that many corporate houses go for branded milk rather than Co-op milk, so there could be some networking at play here. Also, the newer generations prefer to be associated with private brands rather than the Co-op brands.

Then again, they also don’t want to spend hours and hours in converting milk to another VADP in order to use it for cooking. They would much rather pay for the final product. This is why I think there is a large scope for VADP in India. This becomes more attractive to the private players when we realize that the Co-op brands are very slow to adopt to this and may not necessarily want to be in this segment in the first place.

This article offers a better perspective:

The challenges / opportunities will be in:

Marketing: Using more and more social media platforms to reach millennials and using more personalized marketing.

Distribution: Using delivery partners to directly reach the customer. Grocery delivery is just picking up in India.

Branding: Millennials love branding and they are more health-conscious than ever. So associating the company with health and welfare would be the perfect way to attract and retain the younger generations.

Of course, backing all this up would be the Supply Chain, which as I have mentioned time and again, is a extremely important component for any diary player. A well-developed Supply Chain built over several years acts as a great entry barrier too.

Surprised that the Credit Rating was reaffirmed. But I’ll take the good news when I can.

Could you please explain.

Did you expect the rating to be downgraded and why.

Thanks

Yes. We had to bring down Margins (Or should I say, purposely not pass on Margins) as a strategic move. We are also doing a large amount of Capex which is not live fully yet. The Capex is also funded a part by Debt. So it does turn down the Credit profile of the company (Temporarily, at least).

But good to see that the Rating has not been downgraded.

I am looking at the past few years of PL statement of Heritage. There is an item under “Fair value gain on FVTPL equity securities” which goes under Other income in screener. There is another item “Loss due to changes in fair value of derivative liabilities” which I think goes under operating expenses in screener. The second item “Loss due to changes in fair value of derivative liabilities” kind off nullifies the “Fair value gain on FVTPL equity securities” in the past two years in the PAT while it causes problems in operating profit calculation in screener.

Question - Could someone please explain what these items are and why it impacts the profit?

Also under investments in balance sheet there are two items

Question - Why are these treated differently? Can the company sell these investments at the market price? Is there any restriction on the sales of these shares? I understand that they recieved the equity on the sale of the retail division.

These shares are locked in till mid of 2020.

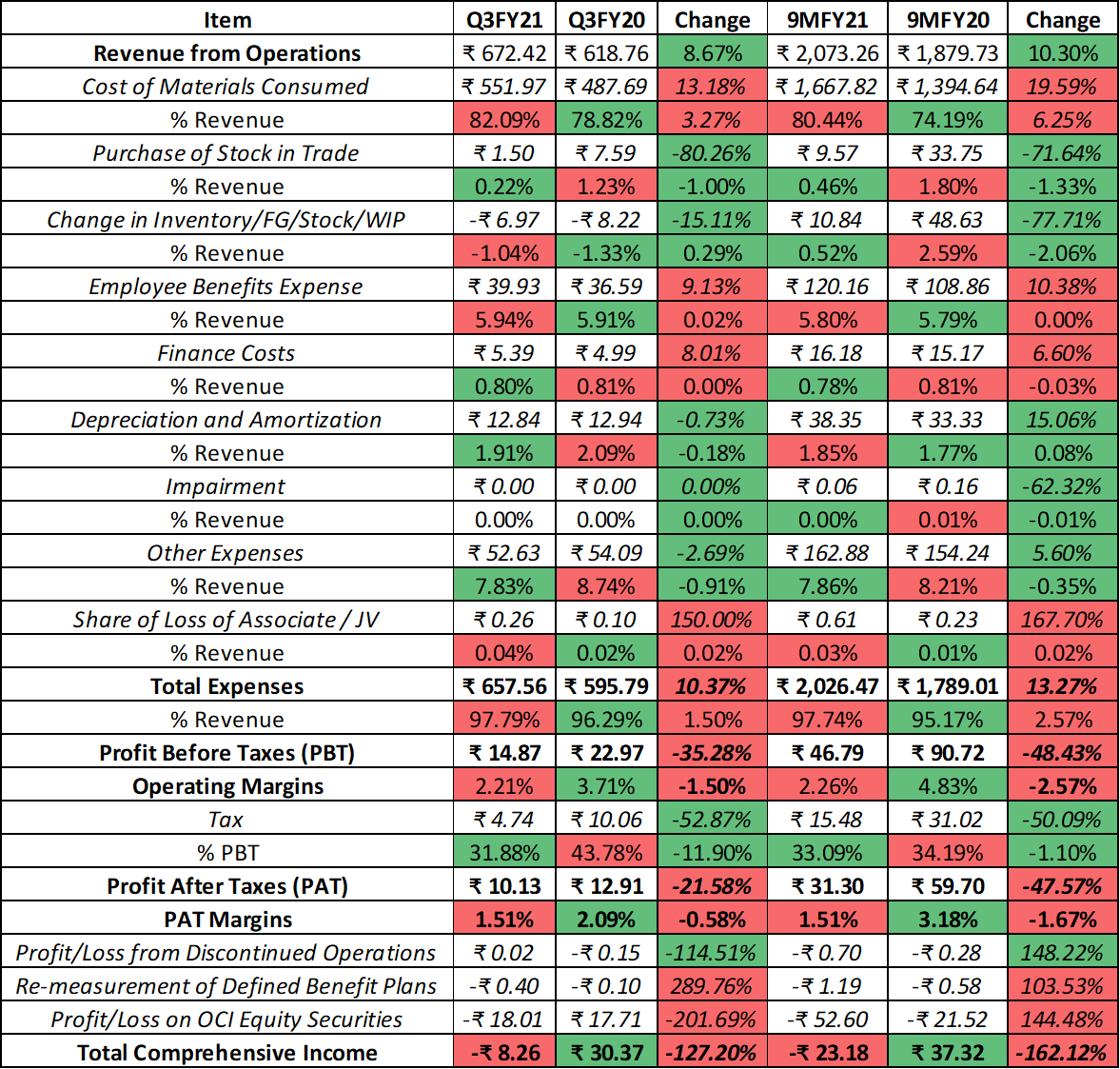

Poor results continue, but again Revenue Growth of ~9% is promising.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/b1e9743a-ec53-40e4-acae-0b1eba741946.pdf

(Took the liberty to exclude Future Retail Stake Gain/Loss and the related Derivative Gain/Loss)

Investor Presentation

https://www.bseindia.com/xml-data/corpfiling/AttachLive/89c5a879-a7a5-4cf3-99d2-0e2822288495.pdf

Heritage Concall Q3FY20

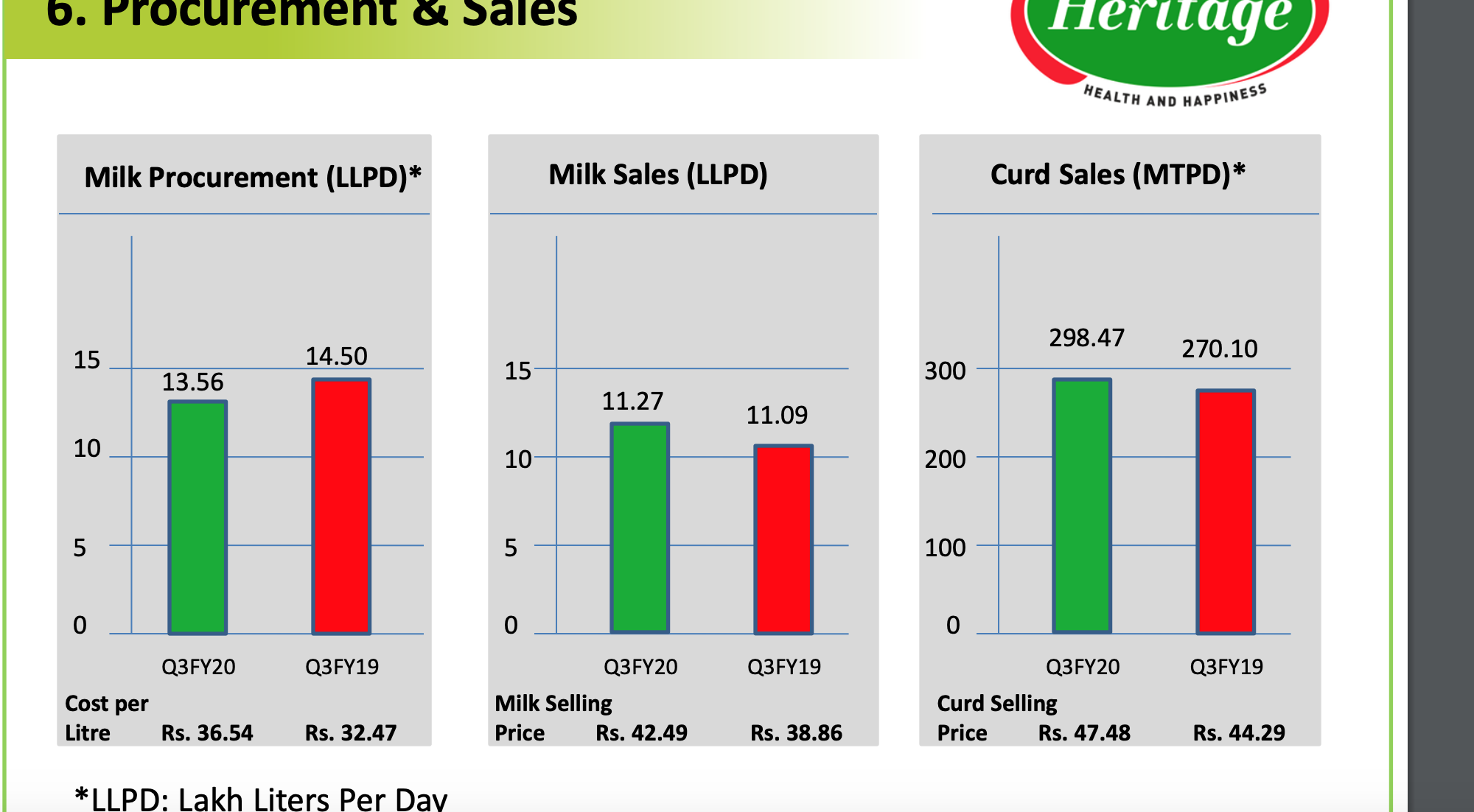

Milk procurement prices have risen in Q3 as well to about INR 37/liter and we have also increased prices by INR 2 Rs/liter on 13 LLPD/ volume from Jan 21 to INR 44.5/liter.

Flush season starts in October and peaks in January however this year flush season has not fully arrived yet due to delayed monsoon.

SMP processors are aggressive in procurement due to high SMP prices (320 Rs/kg). This is affecting procurement for liquid milk players like Heritage

Expect to do 6% EBITDA margin in FY20 as compared to 7.3% in FY19

Fat product sales have declined because procurement has declined.

Hoping for removal of duty on SMP imports to lower milk procurement prices.

Low stocks of SMP with local players as compared to previous years.

Yogurt plant go-live in Mumbai is delayed to Q2FY21 due to monsoons

Might not sell FRL stake even after expiry of locking at end of FY20

INR 30 lakhs capex for 10,000 LPD capacity at chilling center

My comments:

A lot of moving parts in this business - SMP prices, government policy, monsoon impact on lactation cycle, flush vs dry season volatility, inability to pass on price hikes immediately and in full. y-o-y curd volume growth has also slowed to 10% this quarter. Given that procurement has slowed at the peak of the flush season, next 3 quarters are going to be tough for Heritage. Especially if SMP prices stay at current levels or go higher, the cost of maintaining sales in the dry season will take margins even lower. Looks like a tough FY21 without government intervention.

Disc: Invested

YoY Gross margin has declined by 270 bps while EBITDA has declined by190 bps. Clearly, higher RM prices are the cause of lower margins even though the co has been more operationally efficient

In absolute terms, gross margin has declined by INR 6.6 cr y-o-y while it has increased by INR 9 cr q-o-q

Out of this, gross margin contribution of liquid milk is INR 3.5 cr decline y-o-y and INR 4.1 cr decline q-o-q

I am assuming that change in total GM - change in Milk GM = change in VADP GM. Therefore, in absolute terms, the gross margin contribution of VADP has declined by INR 3.1 cr y-o-y while increasing by INR 13.1 cr q-o-q. Q3 would have been much worse than Q2 if not for the recovery in VADP gross margins.

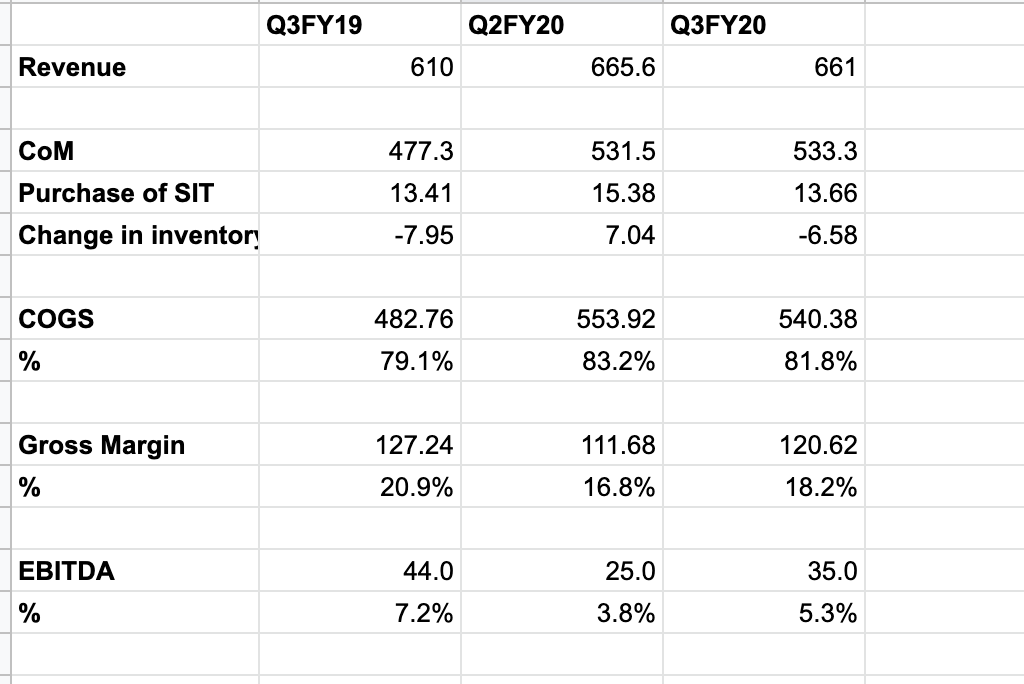

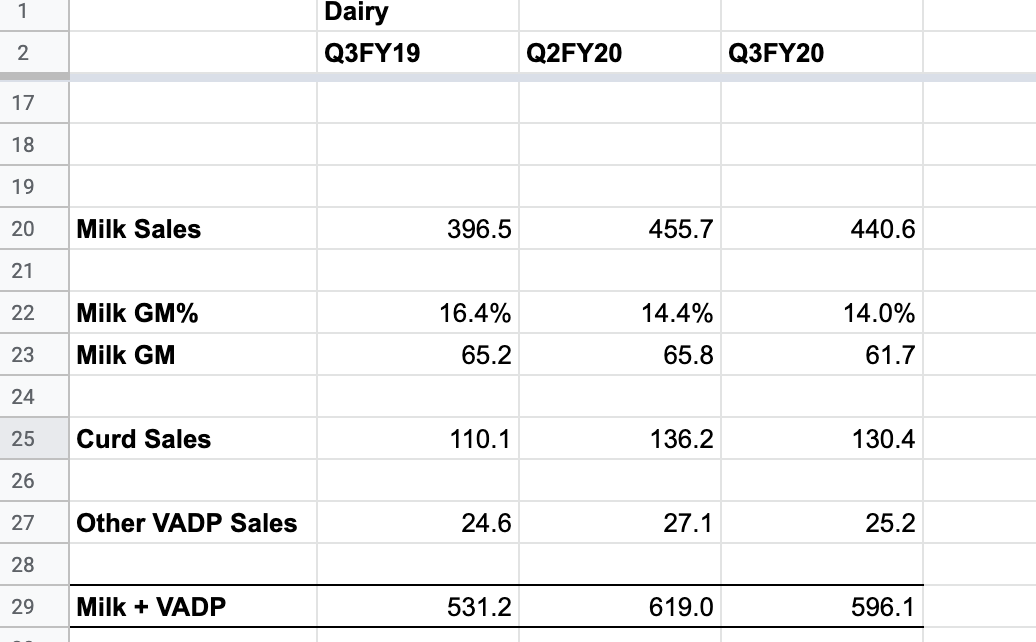

Note: All numbers sourced from Q2 and Q3 FY20 investor presentation. Milk Sales and GM calculated on the basis on below numbers.

Sale of Plant

We wish to inform you that the Board of Directors of the Company at their meeting held on February 28, 2020 approved to sale of all the tangible assets (viz. Land, Buildings and Plant & Machinery etc.) of the dairy plant located at Bhambri Village, Thesil Khamanon, Fatehgarh Sahib District, Punjab as a part of our business rationalisation in Northern India.

Sold off a loss-making unit for Rs. 21.20 Crores. This is should help with the Capex.

Future Retail Stake

As many of us know, Heritage Foods holds 1.784742 Crore Shares in Future Retail Limited, which is worth about ~Rs. 550 Crores at CMP. Divided by the company’s 4.6398 Crores Equity Shares Outstanding, that’s about ~Rs. 120 per Share. This investment alone is about ~70% of Net Worth and ~33% of Market Cap.

The lock-in for these shares are coming to an end Mid-2020. The management has not made an official decision on what to do with the investment yet. Regardless of their decision, it has to be noted that this investment should form a good part of Heritage Foods’ Intrinsic Value.

Do you any erosion in CMP of heritage despite uptick in dairy demand due to lockdown, just becuase of all the negative news around Future retail?

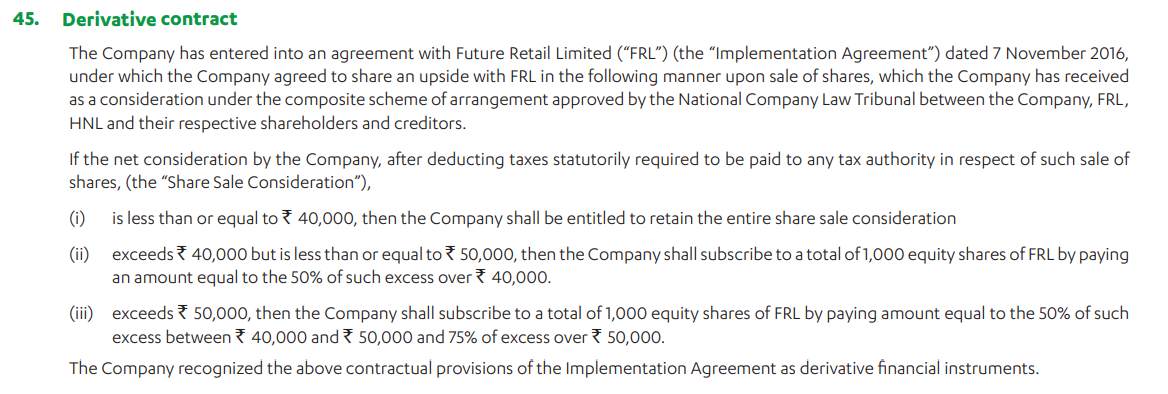

I stand corrected. The Derivative contract is to hedge against the contract Heritage made with Future Retail during the acquisition of the shares:

Thank you, @punitm306 for pointing out. I misread the Annual Report. So it looks like a fall in Future Retail’s Share Price does have an impact on Heritage Food’s Value. Either way, let us wait for the management’s decision on whether or not they are selling the stake.

A boring / standard concall. But good to know that Sales have not been impacted that much due to Necessary Goods status.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/58db774b-bc51-4a74-8361-3af144159040.pdf

In other news, Heritage launches A2 Milk: