The purpose of rights issue is to raise money. Period.

Here, they issues rights share at Rs.5 against cmp of 300+! They weren’t really raising money but was equivalent to bonus issue, yet they didn’t give bonus but did right issue to gain some more shares in place of innocent retailers.

This is definitely wrong on part of promoters

4 Likes

Promoter woes

1 Like

Wonder what has Naidu got to do with Heritage? Is he involved in day-to-day operations? Is the company involved in any fraudulent activities? The management has years of experience in the dairy and FMCG sector both in India and western economies, has negligible debt, high return ratios, partnerships with multinational dairy brands, sometimes people just want a reason to instill fear using irrational rationale

4 Likes

Andhra Pradesh exit polls shows majority for TDP-BJP alliance. Owner of heritage foods Mr. Naidu and good Q4FY24 results few days ago can provide the required momentum to the stock.

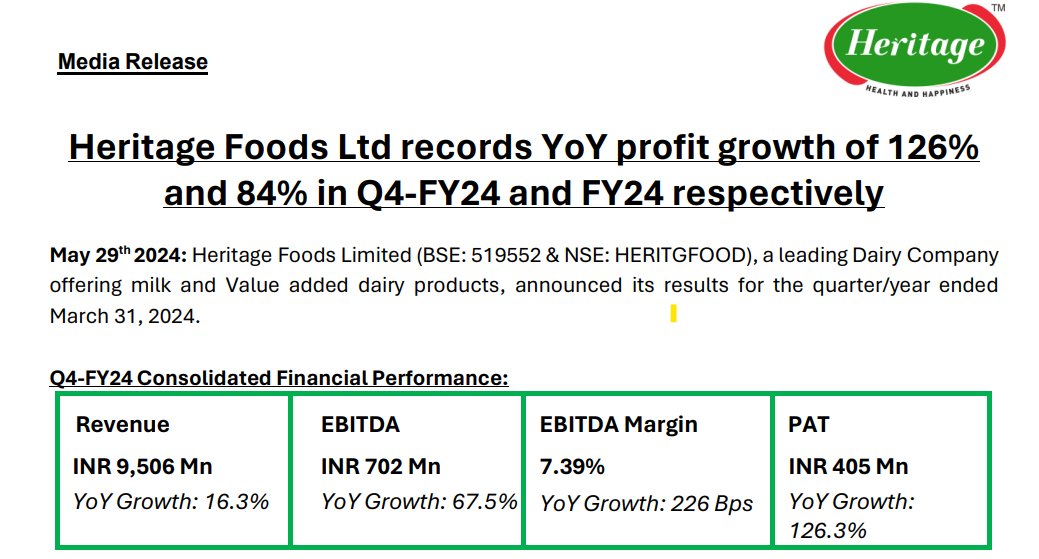

Also, margin saw an improvement of 200 bps! Extremely positive

Note: Invested hence biased.

Heritage has seen growth in Odisha. Atleast in Bhubaneswar, I saw a lot of their products. But the pricing is off. Their buttermilk is Rs. 20 compared to Rs. 15 of Amul.

1 Like

58% of revenue comes from milk however future business outlook based on management commentary includes a focus on increasing VAP share to 40% of revenue (which will take margin even higher), expanding the product portfolio (already launched 2 new ice cream: Fig Honey Cashew & Berry Burst & Vibez Ice cream) and penetrating new geographies.

Furthermore, Heritage Nutrivet Limited robust Top-line growth YoY 50% and bottom line YoY grown Exponentially 360%.

1 Like

Chandrababu Naidu has won the state elections. The stock price seems to factor in Andhra state’s market as it was majorly pushed out during previous government’s period. Is the company reflecting fundamentalsad expected growth or is going up the hype train?

2 Likes

There might be some political flavour to it but largely the rally was driven by stocks under Rural Consumption theme defying the crash. This happens to be one of them.

With the rate the stock has risen, political flavour seems to be the reason. With CBN secured at state and necessary at centre, the stock has a lot of political backing.

Stock has clearly been rerated way above where it should be on multiples after Naidu’s reelection. Considering the growth company is projecting, the current multiples look quite expensive. Retail investors need to be very careful while planning entry. 20-25% correction can come anytime.

Disc- Invested from 200s levels.

2 Likes

This was my stance 9 months back, and this will be my stance till the company keeps delivering results. Dairy is extremely fragmented sector in India coupled with being heavily underpenetrated. Being a milk surplus nation, the entire sector (not just heritage) has good long term prospects. Important to note that the dairy industry is supply pushed rather than demand pulled. Heritage is one of the few which owns the entire supply chain unlike many cos who just do contract manufacturing and label them due to which they’d never have any inventory related shortages

Let’s see it mathematically

Revenue: 3794 Cr

EBITA margin (average from past): 11% (revenue from value added products will increase over time thereby increasing margins)

EBITA: 417 Cr

Profit after tax @25%: 266 Cr

EPS: 28.53

considering industry median PE @35;

price per share comes at 998/-

@Hemant_Kumar2 Please provide if you have any anti-thesis, it would help us.

1 Like

PAT for FY 2024 was reported to be 107 crores and stock currently quotes at 50 p/e (way over Industry median).

But let’s try to predict what earnings could be in the future as it’s more important for stock price. (Disclaimer- calculations may not be very precise and I have ballparked a few numbers).

1- Management in the last concall, after a lot of prodding from the analysts, nodded towards a topline growth in the range of 15%. Management’s view is that milk consumption (70% of current topline) tracks country’s GDP growth and since milk is quite organized (40% of total country’s milk consumption), heritage’s top line growth in the best case scenario (growth in consumption and steady gain in market share) will not be more than lower double digit (say 10-12%).

2- Main trigger to topline growth will come from value added product (VAP) category where margins are higher and organized sector’s share is very low. Heritage is growing its VAP portfolio in 18-20% range and currently it accounts for some 30% of total revenue. Management seems to be confident about VAP reaching 40% of topline in next few years which will also improve EBITDA.

So combining above, I feel that weightage average growth in topline should be around 15% (in the best case scenario) doubling in 5 years.

As for EBITDA, a higher share of VAP in portfolio and some operating leverage could yield an EBITDA of 11-12% (historically it’s been in 5-7% range). So if Heritage were to reach a topline of 7000 crores say end of 2028, we’ll have an EBITDA in the range of 800-900 crores (again in the best case scenario).

Coming to PAT, it’s been 1-4% of topline historically. But at 11-2% EBITDA, it’s very likely that PAT grows to 6-7% of topline giving us 400-500 crores.

Taking your median P/E of 35, this translates into 1400-1700 of share price, implying a stock price CAGR of 15-20% for next 5 years.

Now if you were a pessimist like me, and projected a 15% CAGR from here onwards, it may not look exciting for a small caps stock, considering that growth prices in the best case scenario. But then 20% CAGR on the other end of the spectrum is quite satisfying (if not mouth watering).

So I think investors getting into Heritage food will have to be fully sold on company’s future growth prospects hoping for everything to play out perfectly without any hiccup which hinge on the management’s ability to:

1- Grow VAP to 40% of total revenue in next 5 years

2- Consistently grow market share in both milk and VAP category

3- Consistently pass increase in milk prices to consumers

If management could deliver on the above and Heritage traded at multiples above sector median (due to reasons such as a friendly state government or company’s recent foray into now BJP-ruled Odisha), one can make a very strong bull case for the stock. But it will be a P10 bull case. One should temper this scenario with analysis of potential downsides and then take a call accordingly.

7 Likes

I disagree with this hypothesis. Attaching a video which I completely resonate with and the reason for which I wouldn’t let go of Heritage or think of it as just a short 5 year story. As long as they keep delivering on their business plan, I’ll retain the company in my portfolio

https://x.com/FundamentalGems/status/1799496350385463337?t=-nkPWpRMUSVJT-OTY8cYLA&s=19

1 Like

You have misunderstood my whole post choosing to focus on a slice of it. I myself am an investor in the company since 2021 and don’t intend to sell it (although booked some profit today).

None of what I wrote should be construed as a bear or bull commentary about the stock.

I was just responding to a query on the valuation of the stock positing that valuations at current level can be seen as stretched or comfortable depending on how one see the future unfolding, giving a P10 and P90 scenario.

Reason I considered 5 year time horizon is because in my view it’s sufficiently long holding period for an average investor in which they would like to make decent returns. But it doesn’t mean that I’m implying that company would survive for only 5 years.

The same data points, gleaned from management commentary, can be extrapolated, by investors, to 10, 15, 20 years time horizon to base their investment case on.

3 Likes

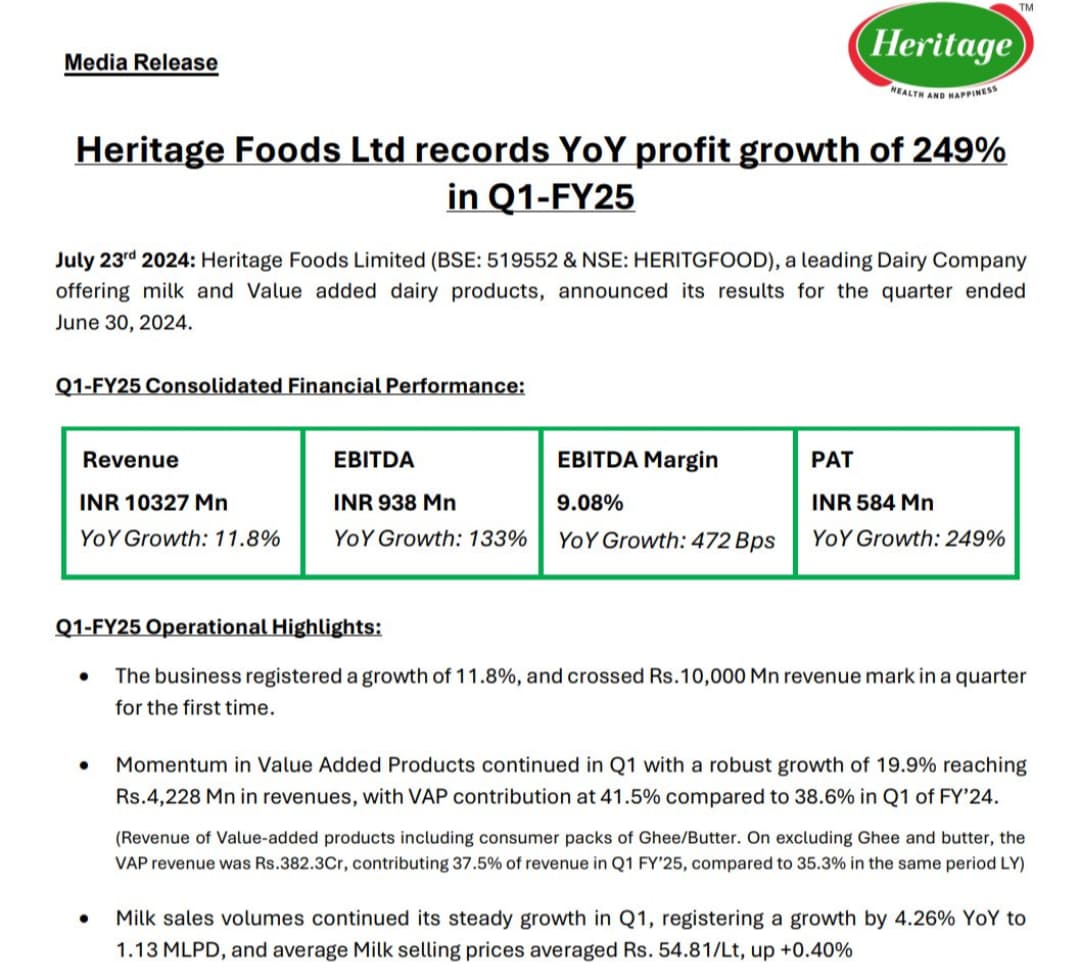

Management walked the talk with 41.5% contribution from Value Added Products (VAP). This also reflected in their EBITA margin of 11%.

Furthermore, considering similar margin phase of Hatsun agro from 2016-2019, heritage foods is relatively highly undervalued. (Hatsun use to trade at an average of 2.3 price/sales during 2016-19)

Let’s see what future holds!

Invested hence biased.

1 Like

Indeed great results and management seems to be executing strategy quite well. At 720 (which stock touched last month) valuations were very expensive but at 580 and with current earning growth 30 p/e looks very reasonable and in line with historical averages (adjusting for some rerating due to current government and increasing margins).

I still won’t call it undervalued comparing it against insanely valued stocks Hatsun which I don’t understand why they need to trade at 80+ p/e. At some point in time these stocks need to come down to 30/40+ p/e .

2 Likes

Thank you!

Your thought process in valuing stocks is impressive. While comparing, I didn’t acknowlegde that Hatsun could have been overvalued.

Please do share your Twitter ID if you’re present on the platform.

Thanks for the kind words. I’m not on twitter and I have recently started writing on valuepikr. May be will start my own Twitter thread at some point in time.

All the best with your investment journey.

Notes from the concall:

- Quarterly revenue crossed ₹1,000 crores for the first time in history.

- FY’28 target : sustain 17-18% growth YoY with 7-8% EBITDA margin for next three years. 9% EBITA achieved in this quarter is kind of peak for near term. Looking to grow in high teens, with 5-6% from price increases and 12-13% from volume growth.

- Expect growth to come from both volume expansion and revenue increase.

- Focus on shifting towards value-added products to drive revenue growth. (Ice cream segment witnessed 20% odd revenue growth. Bangalore is becoming big market via swiggy, zomato, zepto)

- Orissa as a new geography is responding quite well.

4 Likes