AR22 notes:

Miscellaneous

- Aggregate capacity: 15’224 MTPA

- Sent 1st consignment to USA in October 2021

- Incorporated Mikusu India Pvt Ltd

- CSR: 3.06 cr. (no unspent)

- Median salary: 4.06 lakhs (vs 4 lakhs in FY21)

- Permanent employees: 714 (vs 601 in FY21)

- Contract employees: 805

- Share price: 551.1 (low), 866.85 (high)

- Shareholders: 93’108 (vs 111’829 in FY21)

- Auditor remuneration: 40 lakhs (vs 40.5 lakhs in FY21)

- Cumulative receivable impairment: 22.45 cr. (vs 17.11 cr. in FY21)

R&D

- R&D team of 22 members (vs 22 in FY21), have been working on a product basket of 15-20 molecules

- In FY22, worked on developing 2 fungicides, 2 herbicides and 1 insecticide. 2 of these compounds are at an advanced R&D stage, and are being developed for sales in Europe and USA

- Will commercialize 3 molecules in FY23

- Plans to launch 5 molecules in FY24 (subject to getting registrations)

- Will expand pyrethroid product basket from 5 currently to the entire range of 10-14 molecule

Capex

- Had CAPEX of 80 cr. in FY22, 1/3rd towards on the Sarigam site. Spent 25 cr. to acquire land at Saykha

- 180 cr. has been earmarked for Sarigam technical expansion. This phased expansion will increase capacity by 5,000-6,000 tonnes in phase I by the end of Q4FY23, and 10,000 tonnes by the end of FY24.

- 50 cr. has been earmarked for the Sykha site. However, it will be given further priority in the coming years, upon complete commercialization of the Sarigam site

Manufacturing units

- Unit I (GIDC Vapi): Manufactures a wide range of synthetic pyrethroids, organophosphorus insecticides, and various pesticides intermediates. It is a large scale manufacturing unit for insecticides, herbicides, fungicides & their intermediates

- Unit II (GIDC Vapi): Manufactures Cypermethric Acid Chloride (CMAC) and all other Isomers/derivatives of CMAC. Also manufactures Cypermethrin, Alpha Cypermethrin and Permethrin technicals. The Company has acquired an industrial plot measuring 2702 sq. mt. adjacent to the existing unit which has enabled them to enhance production capacities and upgrade Unit II’s environmental pollution control facilities. Common Boiler System is also being explored on this newly acquired plot to cater to steam requirements for all the Company’s running Units at Vapi

- Unit III (Sarigam GIDC): Equipped with modern formulation and packing facilities capable of handling large capacities of Liquid, Powders and Granules. The formulation division was established to exclusively focus on manufacturing branded formulations and trading activities. In addition, this unit is involved in the manufacturing and distribution of agrochemicals for plant and public health segment. Company has installed and initiated its new setup of spray drying facilities for WDG formulations for various formulations of sulphur such as WDG and specific combination formulations of sulphur such as Sulphur/Imidacloprid 70WG/ COC WG, Sulphur/ Tebuconazole, and other such spray-dried granulated products. This unit is also equipped with a rooftop solar plant that generates 185.0 KW per annum energy, utilized for captive consumption, in addition to its DGVCL power connection of 750.0 KVA. Got EC approval for technical manufacturing, production should begin by FY23 end

- Unit IV (GIDC Vapi): Large volume production facility to produce highest purity products from by-products and Intermediates, which have agrochemical applications. This facility enables the Company to become self-dependent, mainly for Bromine recovery, without relying on external job workers. Commercialized in FY22 and expect 100 cr. revenues from this site

- Sakhya: Has land parcel of 34’600 sq.m for further expansion with EC approval for annual capacity of 10’680 MTPA. Company has also acquired an industrial plot measuring 57,248.29 sq. mt. at Saykha Industrial Estate for further expansion

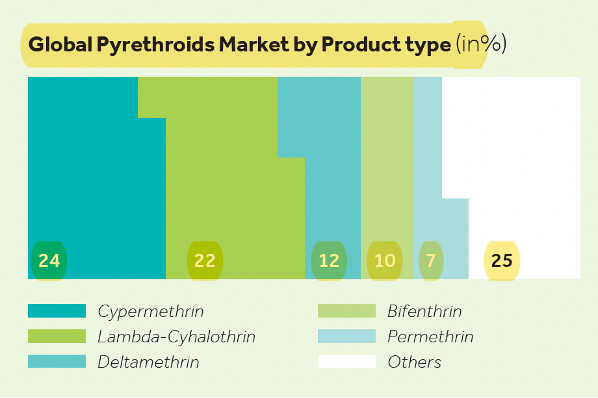

Pyrethroid molecule breakup

Disclosure: Invested (position size here, bought shares in last-30 days; still building up the full position)