Unit Linked Insurance Plans - Expected to be Hit the Most Post the Market Crash due to Covid-19

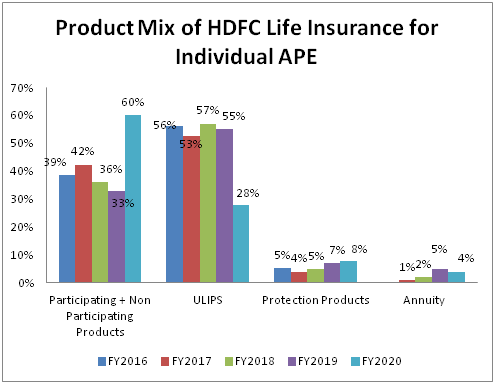

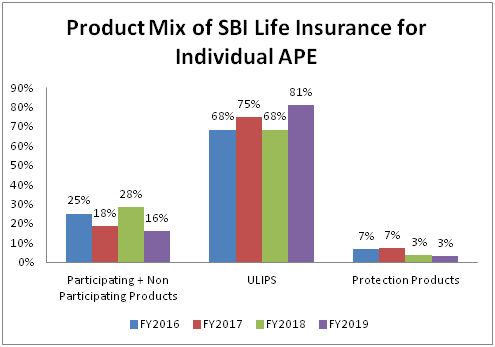

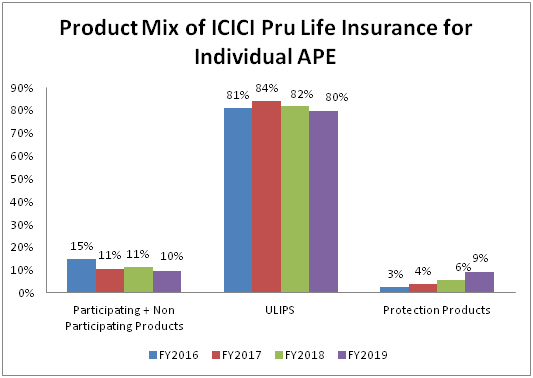

SBI Life & ICICI Life has significant exposure to ULIPs. Almost 80% of their retail new business premium on the basis of annual premium equivalent (APE) came from ULIPs. HDFC Life has a more balanced product mix with ULIPs accounting for just 28% of retail APE.

ULIPs are generally a hit product when capital markets are in a bull run. With the Covid-19 uncertainty looming over capital markets & the sharp correction Indian bourses has been through, it is highly likely that people will discontinue their policies. This creates uncertainty amidst SBI Life & ICICI Life as their retail product mix is skewed towards ULIPs.

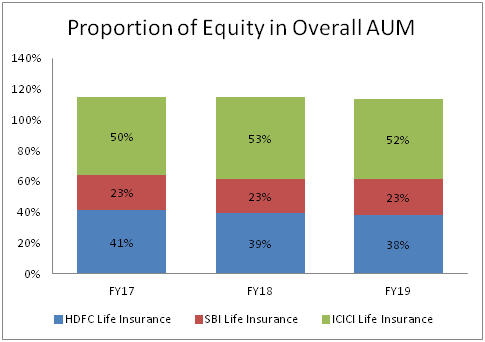

Further, looking at the composition of debt/equity mix in the assets under management (AUM) of these players, ICICI seems to be the highest exposed as it has significant proportion (i.e 52% as of FY19) of its AUM in equity. While, that ratio stands at just 23% and 38% from SBI Life and HDFC Life.

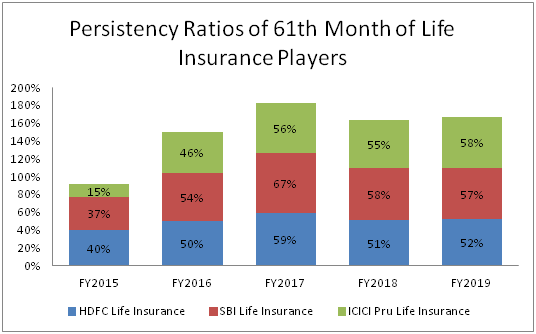

An exposed retail product mix skewed towards ULIPs can also dent persistency ratio at ICICI Life. As people discontinue their policies, persistency ratio can take a hit. It is observed that in bear markets, the persistency levels see a decline. ICICI enjoys the highest persistency ratio as at FY2019. And this can come under pressure in the coming quarters which could impact the Embedded Value.

Considering all this, HDFC Life seems to be better placed than the other players given a very well diversified product mix.

Pure Protection Products to Benefit of Covid-19

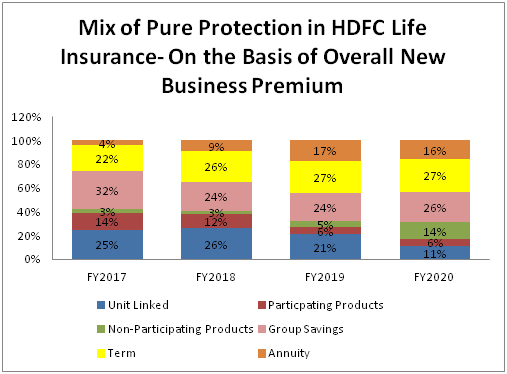

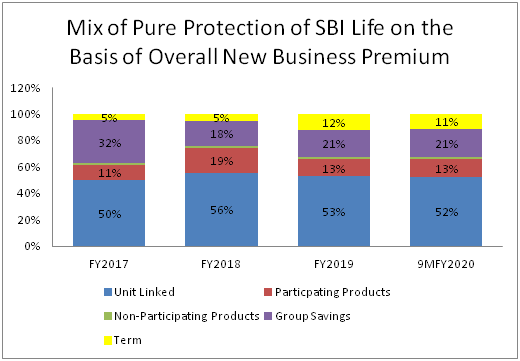

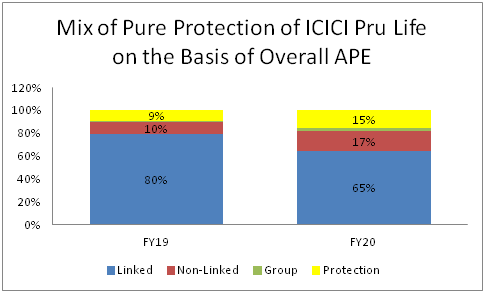

Pure term products will gain popularity post Covid-19 as people adopt to such products which protects their families incase of their untimely deaths. Reportedly, the VNB Margin on such term products lies between a very healthy 70-100%. Hence, it’s a good value proposition for a life insurer to grow this product vertical. HDFC Life has 27% of its overall new business premium (individual + group) coming from this vertical in FY19. For SBI and ICICI, this ratio stands at 11% and 15% respectively.

The persistency level of pure protection products is generally higher when compared to investment cum protection products. Hence, sustainable business can be derived from such products.

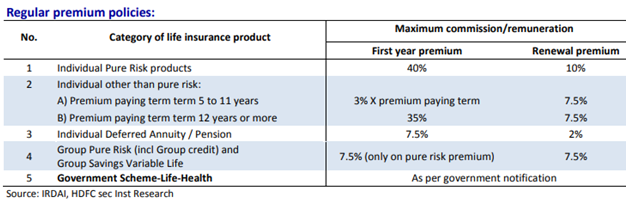

Further, IRDAI has made it more lucrative for distributors to sell these products as commission rates are higher when compared to pure risk products as seen in this table:

The Emerging Channels in Distribution- Online Channel

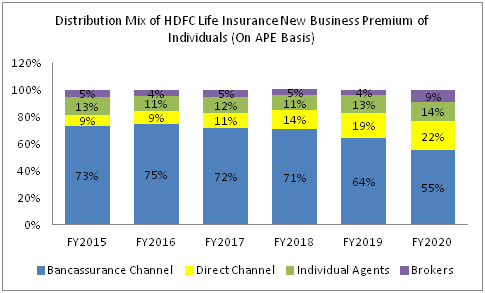

Digitization as a channel to sell products to millennial generation is the need of the hour for all life insurance players. And HDFC Life is capturing this trend pretty well. As of FY2019, HDFC Life secures 22% of the retail new business premium on the basis of APE through digital channels. Further, as reported in its latest investor presentation 85% of renewable payments are made digitally. This ratio stands at less than 3% for SBI Life and 13% for ICICI Life. There are huge commission costs life insurers pays to intermediaries such as banks, individual agents or brokers to generate sales. These costs will get eliminated if client is acquired through digital modes.

Further, HDFC Life has diversified well from over-reliance on the bancassurance channel. The contribution from bancassurance channel has reduced from 73% now to 55%. HDFC Bank solely contributes 80-82% of new business generated from the bancassurance channel. Hence, if there are any regulations in future suggesting banks to reduce exposure to one life insurer to the extent of not more than 50%, then the bank is better placed.

At the same time bancassurance offers an immense opportunity. HDFC Bank is well on its way to double its branches in the coming years. And hence, this offers a significant opportunity for HDFC Life as well.

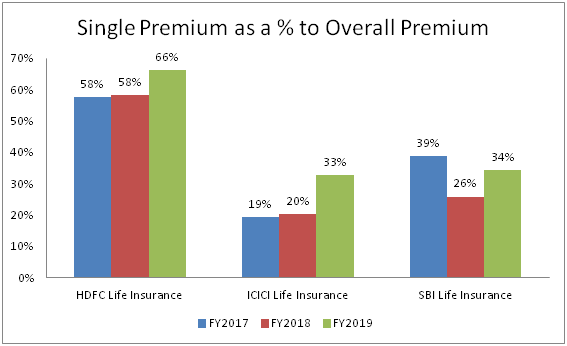

Single Premium as a Percentage to Overall Premiums

Single-premium life (SPL) is a type of insurance in which a lump sum of money is paid into the policy in return for a death benefit that is guaranteed until you die. There is no renewable premium to be paid thereafter. It’s a single bullet payment. Hence, the hassle of following up to pay the renewable premiums and maintenance expenses to be incurred for following up on the renewable premiums are reduced.

HDFC Life has the highest proportion of single premiums when compared to overall premiums in the industry at 66% in FY2019. Whereas, this ratio stood at 33% and 34% respectively for ICICI Life and SBI Life Insurance.

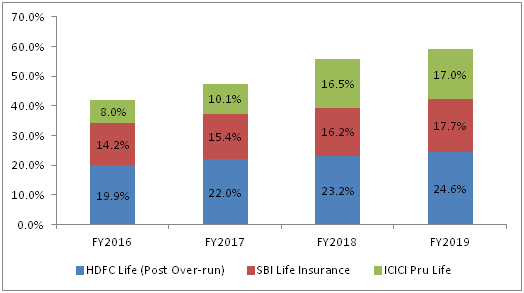

Value of New Business Margins of Insurance Players

The Value of New Business Margins (VNB) are the highest for HDFC Life. This is on account of a product mix which is skewed towards high margin products. Reportedly, the new business margins on selling the following insurance products are as follows:

| Particulars |

ULIPS |

PAR |

Non-Par |

Protection |

Group Savings |

| New Businesss Margin on APE Basis |

2-10% |

12-20% |

20-30% |

50-100% |

0.5-2% |

| Source: HDFC Securities |

|

|

|

|

|

ULIPs have the lowest margins. Whereas, the margins on Protection and Non-Par are higher. As HDFC Life is scaling its protection and non-par business vertical as seen in Chart 1, the margins are on an increasing trend.

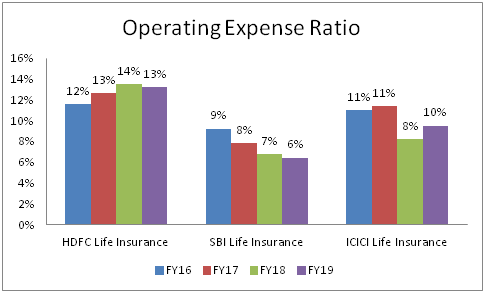

Operating Expense Ratio

The operating expense ratio is the highest for HDFC Life which is a negative. Whereas, SBI Life enjoys the lowest operating expense ratio amidst the private players. One of the reasons for costs being higher at HDFC Life is the technological investments done to grow the online channel. Also, the digital marketing campaigns run to lure the prospective customers to purchase online involve cost.

SBI is the most efficient players when it comes to cost as it relies highly on bancassurance distribution model to sell its products. Selling products through bancassurance channel is relatively cheaper when compared to other distribution method. There is certainly a high operating leverage in selling products through bancassurance channel and one of the main reasons for cost being lower at SBI Life.

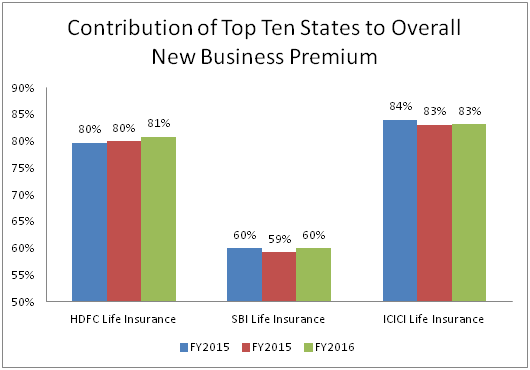

Geographical Diversification of Life Insurance Players

Acts of gods can lead to a spurt in mortality/morbidity rates. Gujarat earthquake 2001, Kerela floods 2018, Tsunami in 2004 can create a huge spike in claims in certain geographical areas. This can dent profitability of insurance companies. Hence, prefer insurance companies who are geographically well diversified. However, SBI is the only life insurer as on FY2016 which appears to be well diversified with 60% of its new business premium coming from 10 states and none of these states account for more than 10% of new business premium.

Whereas, in case of HDFC Life and ICICI Life 80% of new business premium comes from 10 states. And both insurers have exposure to Maharashtra exceeding 25% of the new business premium. Hence, there is a geographic concentration when it comes to HDFC Life and ICICI Life.

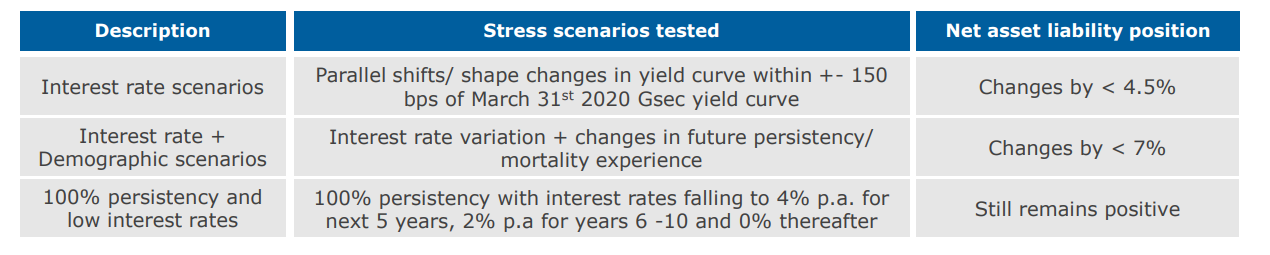

Sensitivity to Variables which Could Impact Embedded Value

This table indicates that Embedded Value of HDFC Life is most immune to the changes in interest rates. Further, an increase in tax rates can lead to a considerable dent in EV value of life insurance companies.

| Sr No |

Sensitivity of Industry to Following Parameters |

Scenario |

% Change in EV for HDFC Life |

% Change in EV for SBI Life |

% Change in EV for ICICI Life |

| a |

Reference Rates |

Increase by 1% |

-1.2% |

-5.0% |

-2.5% |

|

|

Decrease by 1% |

0.6% |

5.0% |

2.6% |

| b |

Equity Market Movement |

Decrease by 10% |

-1.1% |

-1.0% |

-1.8% |

|

|

|

|

|

|

| c |

Discontinuance Rates |

Increase by 10% |

-0.7% |

-1.0% |

-1.1% |

|

|

Decrease by 10% |

0.8% |

1.0% |

1.1% |

| f |

Mortality/Morbidity |

Increase by 10% |

-1.8% |

-2.0% |

-1.6% |

|

|

Decrease by 10% |

1.8% |

2.0% |

1.7% |

| e |

Tax Rates |

Increased to 25% |

-7.7% |

-8.0% |

-5.8% |

Conclusion:

Not considering valuations, all these indicators as stated above leads to some conclusion that HDFC Life is the best placed player in the life insurance space.

However, what are the valuations to be given to these companies?

Here is the one of the report of Edelweiss which values life insurance companies as follows:

Source: Edelweiss

Source: Edelweiss

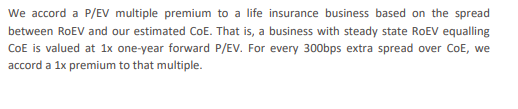

Keeping some extra margin of safety especially post Covid-19, for every 400 bps extra spread over CoE, we accord a 1x premium to that multiple. Here is the levels at which stocks can be bought.

| Particulars |

HDFC Life Insurance |

ICICI Life Insurance |

SBI Life Insurance |

| Return on Embedded Value |

18.1% |

17.7% |

16.5% |

| Cost of Equity |

11.0% |

11.0% |

11.0% |

| Spreads |

7.1% |

6.7% |

5.5% |

| Additional Multiple to be Givn on Spreads of 400 bps |

1.8 |

1.7 |

1.4 |

| Overall Multiple to be Give to the Business ( Price/Embedded Value) |

2.8 |

2.7 |

2.4 |

| Embedded Value |

20650 |

23030 |

26290 |

| Instrinsic Value of Business |

57304 |

61605 |

62439 |

| Premium Valuation Given the Fundamentals Of HDFC Life |

20% |

0.0% |

0.00% |

| Instrinsic Value of Business |

68765 |

61605 |

62439 |

| Current Market Capitalization |

97376 |

55948 |

71487 |

| No of Shareholders |

202 |

144 |

100 |

| Instrinsic Value of Business |

341 |

429 |

624 |

| Correction Required |

-29% |

10% |

-13% |

This is my assessment. I am pretty naive to this industry and I have not invested in any of the life insurance companies. My opinions expressed here are quite biased towards HDFC Life as I am willing to invest around 5% of my portfolio in this stock.

Please Help Me Find Answers to this Question:

a. Will the high ULIP exposure of SBI Life & ICICI Life threaten their premiums coming from new business premium given the uncertainty around capital markets?

ULIPs are a complete pass through products like mutual funds and hence the impact on the balance sheet of SBI Life & ICICI Life will be negligible. But, strain will be seen in the P&L as people stop renewing and these companies will be unable to recover their acquisition costs

b. It seems like buying term products (i.e pure protection) is gaining popularity. Post Covid-19, can this trend intensify?

c. How has LIC been the numero uno player in group and retail insurance? It commands a market share of 42% in retail new business premium and 78% in group new business premium. With the bancassurance channel and the onslaught of digitization, is there scope of shift in market share from LIC to private players?

d. Globally, life insurer players are trading at a very reasonable price/book value of (1-3 times). Here HDFC Life is trading at 13x, ICICI Life at 7.5x and SBI life is at 8x. Is the technique of valuing it at price/embedded value appropriate?

e. Annuity business is a huge opportunity for life insurance. HDFC Life is making huge strides in this space. Does other life insurers like SBI Life and ICICI Life have the balance sheet strength to underwrite such products at scale?

f. Any thoughts on the valuation table which I have mentioned above.