I had applied and got 2 lots of HDFC life in ipo. Thereafter wherever I think of investing I find roe roce very good. But the margins npm opm are Very low (even for icici And SBI). Can anyone explain how is this? Is the insurance accounting something different? Do they book all expenses at earliest? Can anyone pls throws some light.

For life insurance, opm are normally less at the start of business.

In initial years companies are targeting for business growth rather margin or profits.

One business is booked, company will receive premium for years.

Once penetration level is significant, then companies will focus on margins.

Also insurance cost in india is very cheap when compared to other countries, this is future is bound to rise.

Interesting interview of Vibha Padalkar after budget on removal of tax exemption , effects of DDT removal on there AUM , LIC listings, probability in pension funds

Thanks

3 Likes

https://twitter.com/darshanvmehta1/status/1224162590231687168/photo/1

Though with greater diversification of product portfolio like term/pension HDFC life better equip than others.

6 Likes

Forrester report on HDFC Life - Technology led Innovation. Dont have the complete report but met the research analyst

https://www.forrester.com/report/Case+Study+HDFC+Life+Insures+Its+Future+With+TechnologyLed+Inn

ovation/-/E-RES142198

FNO from Feb 28

1 Like

1 Like

Vibha padalkar . It is an obvious opportunity waiting to be leveraged

Possibility of new optionality in Life insurance

Thanks

2 Likes

What will be impact on Life Insurance Company, if COVID-19 related claim rise?

I checked with my insurance company and it said that my 3 Cr term plan covers COVID-19 related mortality.

If Covid-19 goes in third and forth stage, so many claim will be there with Life Insurance company. This will dent the balance sheet of a company.

Also, Irdai said all coronavirus-related claims shall be expeditiously handled and all expenses incurred during the course of treatment, including during the quarantine period, shall be covered by all insurers.

what your view on this ?

1 Like

My 2 cents. Mortality rate is expected to be higher in 60+ individuals. Though I don’t have the actual data, most private insurers would have relatively younger customer base so they would be less impacted as compared to LIC.

3 Likes

In short term is definitely negative but such major events creates more averness for life insurance in long run

I think this is for mediclaim policies

Some more negative points

1.Downturn in stock market may affect there AUM also

2.March is usually there strong month which may be affected

Thanks

https://www.ft.com/content/b2fb2326-6d13-11ea-89df-41bea055720b

Life insurers hold a mixture of assets — mainly bonds — to fund the claims that they pay. The collapse of stock markets will hurt, although for most life insurers equity exposure is limited. Risks to corporate bonds are far more significant, especially because insurers, like many investors, have in recent years been forced to buy riskier bonds in the hunt for yield."

3 Likes

In my opinion the following is playing in the insurance space having short term and long term implications:

-

Shift/Focus towards protection products. Unlike the saving products protection can be promoted digitally leading to cost efficiencies. Given the government steps towards easing income tax rules if one don’t claim a deduction, last minute insurance purchases or cross selling by banks will lose steam.

-

Impact of Corona Virus: Near term coronavirus will have a huge impact as its AUM mix was 62:38 / debt to equity (AR 2019). Given the free fall in the market the company will have a huge Mark to Mark Loses. In the debt AUM HDFC Life has a total exposure of Rs8bn (incl Rs1.05bn towards AT1 bonds at YES Bank) in the troubled names, equally split among Non-PAR, shareholders funds and PAR funds. (Macquarie). As of now the saving grace is that the mortality is more for senior citizens which are the most uninsured or LIC aficionados.

-

Consolidation: Given the current crises only the strongest players with Robust managements will survive/increase their market share. HDFC is well known name and is likely to be a going concern when this crises go through.

Disclosure: Invested since IPO. Not planning to add more till the impact of corona is visible.

4 Likes

Bulk Deal - BSE : STANDARD LIFE (MAURITIUS HOLDINGS) 2006 LTD sold 50000000 shares on 2020-03-27 at a price of 441.24

1 Like

Disc: Zero investment. Trying my learning experience.

Request you to comment and guide my mistakes.

Its my first try here. I have very less knowledge on investment. Investment (value) experience of less than 3 years. Pardon my mistakes and huge valuations mistakes.

Part - 1: Comparing internationals top Insurance companies(MetLife, Standard Life) with Indian HDFC Life Insurance.

For some reason, some of the biggest insurance companies( MetLife and Standard Life ) have not being able to create the shareholder value in long term. Any rationale?

Warren Buffet in Geico Insurance investment: The scenario was slightly different, Warren Buffet’s Berkshire Hathaway brilliantly used the Premiums they received from Geico, which they term it as ‘Float’ and invested them for a great returns (19%) in long term. (For more details on it: Here’s How Much Money Warren Buffett Has Made in GEICO | The Motley Fool)

Valuing Insurance Stocks, value expert suggests us to look into 2 things,

- Price to Book Value: <1 - Brilliant, 1-2 - Decent bets, 3> - Overvalued.

- Equity Growth - 10% - Good, 10-15% - Great.

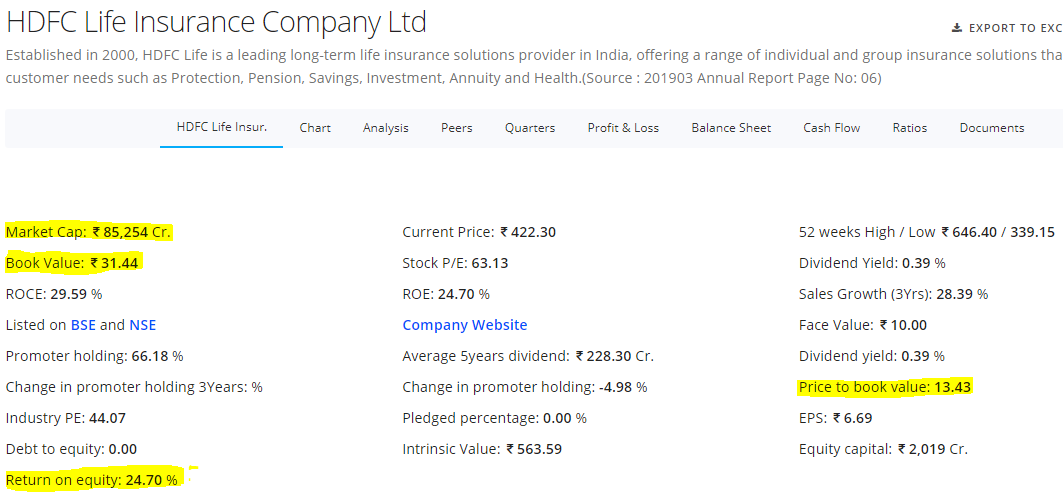

Part - 2 : HDFC Life current Valuations:

- ROE growth - 24% (Super Amazing)

- Price to Book - 13 times! ( Too expensive , good below max. 3)

- Market cap: 80,000 cr - $10 billion. ( MetLife Mk cap : $25.9 billion, x2.5 times )

- Sales: 43,247cr - $6 billion. ( MetLife Sales - $70 billion, x12 times)

Question I am trying to ask myself is: If HDFC Life reaches $70 billion(12 times) in say 15 years, will it have the $130 billion(13 times) the valuation it holds today?

Part - 3: Valuing/Comparison of the HDFC brand name. And deriving HDFCLife Future Valuation.

HDFC Bank: Book value growth.

From the above two pictures, it is exactly what I fear!

HDFC bank in its early days has enjoyed P/E of 40s (2006) and BV of 8-9 (2005). And Now the stock is able to enjoy P/E ratio of 25-30 and BV of 3-5 (Which is still very good compared to competitors)

Therefore: Valuations of HDFC Life in 15 years.

First assumption : HDFC Life is able to keep their ROE at 25% for next 15 years, Their book value will become close to Rs. 950.

Second assumption : Let’s assume it will enjoy premium price to Book value, say 4 (exceptional actually), the price of the stock would be Rs. 3800.

Result : If we are able to buy the stock at say Rs. 350. CAGR returns would be 17%.

Risks : 17% CAGR is with higher estimates of 25% ROE for 15 years and premium BV (at *4x) after 15 years!

13 Likes

Issue with comparing with international business with Indian firm is not always right. Check out the same with paint companies and other such companies. Indian firms with reputed management always commands higher premium than international players. Reason is there r very few such businesses available in India whereas elsewhere there are many such companies. So when there is quality people tend to buy it to preserve capital first and then gains.

1 Like

Yeah I fully agree with you, infact there is a very good article on this subject written by Prof. Sanjay Bakshi. One can read it here https://www.outlookbusiness.com/specials/the-name-is-buffett-warren-buffett/pay-up-but-dont-overpay-1502

3 Likes

I agree with you guys on Premium valuation a good management in India commands.

And, I also agree the likes of Paints and Adhesives stock in India v/s Rest of world. The rationale here is the brand name that are created v/s just commodity in rest of world and the Good Management Premium.

As a student of Value investing, I would be ready to ‘Paying Up’ for these premium business, lets say 4-5BV v/s ‘Over-Paying’ with 11-13BV.

@roushanr1 That is because Standard Life has sold their stake via multiple offers for sale.

1 Like