Detail interview of Padalkar

Thanks

Ashit

Detail interview of Padalkar

Thanks

Ashit

I recently presented on HDFC Life at an informal meet. Please find the presentation attached:

HDFC Life.pdf (1.3 MB)

Disc: Content is for educational purpose only and not a recommendation to buy/sell.

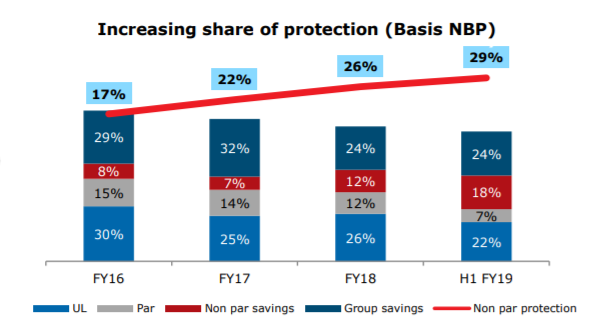

I am still trying to understand the various business terms of a life insurance company, hence have a lot of queries. To start with, can anyone confirm / correct my understanding as given below (data from HDFC LIFE H1 FY19 Investor presentation)

Linked plan:

I understand this as a plan that offers both life cover & investment option (of policyholder’s choice) where a part of premium goes for life cover and the rest (minus charges) is invested in debt/equity as per choice and kinda functions like a mutual fund. And only the life cover is guaranteed and the rest is market linked. Best example is ULIP. But what would be a non-linked plan? Is it any plan that doesn’t give an investment choice to policyholder (unlike ULIP)?

Participating plan:

I understand this as a plan where apart from guaranteed benefit there are additional bonuses involved. How is the premium invested by the insurance company to give returns? And ULIP cannot be a participating plan because ULIP does not pay bonuses?

Protection plan:

I understand this as a pure term insurance plan where there is no survival benefit. Can an endowment plan be considered a protection plan even when it offers survival benefit?

Is a linked plan (like ULIP) considered a protection plan as well as it has a life cover also? Are there any other plans (apart from pure term insurance ones) that come under protection plan?

And in the chart below, may I know how the protection % (shown as 29%) calculated?

H1FY19 Results - Conference call summary

I dont think the results are bad…seeing the stock at almost 52 weeks low is something which is quite strange though the valuations are stretched and when has the promoter has to bring down the holding to 75% currently it is at 80%…that may cause some pressure too…If anyone had any take on valuation what would be the best price to add more…given that insurance is still under penetrated in India

At the time of IPO, shares were sold at an EV of 4.2…so that should be the higher limit of correct valuation range because promoters who have a reputation for being honest sold their company at that price…

With the latest EV of 17400 cr, and EV of 4.2 , share price comes to at 362…

So that can be suitable entry followed with buy on dip…that’s my simple take…best price will be 25-30 pcnt lower than 362…i.e below 275…

Well, there is a segment of market which believes that Nifty is heading to 9k+ levels. This could trigger another round of ULIP exits etc. This may or may not materialise but the risk might be priced slowly. I think non-life insurers remain better bet on risk reward basis. Let’s face it, life ins companies have been finding it tough to sell high value pure term policies. I talk to folks in my circle and I don’t see any urgency to jack up their term plan coverage to 10x annual income. That will be the biggest driver whenever it comes. I think as general population becomes wealthy they would need policies to protect their wealth through health, accidental home/fire etc.

@drgrudge, @bvr007 Looking at the last one year data from IRDAI https://www.irdai.gov.in/ADMINCMS/cms/whatsNew_Layout.aspx?page=PageNo3734&flag=1, individual single premium is contributing more to HDFC life’s premium. So, to grow in future they have to acquire more individual customers than this year. How do you see this play out in future? Why HDFC life is not able to get good growth in Individual Non-Single Premiums? Please share your thoughts

Nice dataset ! How are you getting it ? When I go to the IRDAI website I cannot find it in any folder. I wanted to check it historically.

In my opinion, Non-Life Insurance Industry is more of a long term structural story. Every now and then institution do play as catalyst to make it stronger or weaker. Like recently SC made 3 year motor insurance mandatory. Whereas mindset of larger population has to be made aware about importance of life insurance for their near ones. Though Life Insurance is plagued by its own problem like mis-selling, selling for commission. Term Insurance will pick at its own time to become leader in their product portfolio. In that scenario, Insurer who has risked appropriately without affecting their Bottom line will be safe bet for future.

I think good idea to increase well trained sales force and win win situation for students and HDFC life

Thanks

Ashit

Huge 8.3 % discount compared with current market place…i have never seen this much discount on OFS

OFS price is almost equal to the current market price. What is the use of applying for an OFS if we get a similar price to buy from the market?

In ICICIDIRECT, the floor price in OFS is showing as Rs. 365.2. But the offer price was Rs.357.5. Can someone explain this?

It is adjusted based on yesterday’s response received from institutional investors… Please see clarification with * on price of Rs 357.5 as per email received from icici direct…

Quote

Floor price - Rs. 357.5*

*The floor price on exchange may change depending upon the cut off price in the General (HNI) category on March 12, 2019. You are advised to place limit orders on or above the cut off price.

Unquote

Thanks for the update.

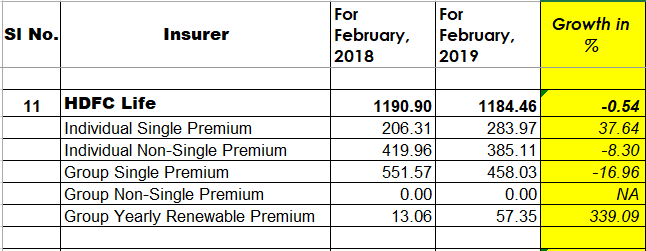

Also, for the month of February, the premium collection is slightly lesser than that of last years’ for HDFC LIFE while other companies have posted growth.

The absolute number for the month is still highest among all companies (except LIC of course)