Attrition is not a new problem especially in the private banking and nbfc sector. One of the reasons being an appraisal and target based performance management system is in place unlike psu. For years I have noticed RMs and Sales associates switch banks in 2 years time failing to meet aggressive deposit, loan targets. Whenever they move, they make efforts requesting the customers served by them to switch to the new bank. Many of you who received such cold calls should be able to relate.

3 Likes

Pressure to sell banking products which are not at all suitable for the customers seems to be the reason behind high attrition rates in all the banks.

If you try to sell unwanted and unrequired products like personal loans, home loans, auto loans, fancy credit cards to people who are above 50+ years of age, then Why they will buy such products? Can the person who is 50+ will take a risk of taking huge auto loans, home loans and personal loans when their job is already in danger to some extent? Most of the people in India today have the constant pressure of job loss after age of 45 itself. Banks target these people for selling high interest rate loans, which is of not much use.

I believe that, HR departments of Banks should set realistic targets which can be achieved in today’s uncertain environment (of massive lay offs in few industries like Airilnes, IT and high inflation), and have some mechanism to reward employees apart from setting targets for them. Employee can be rewarded based on some other parameters like efficiency, understanding of customer needs, turn around time, apart from targets, then this attrition problem can be resolved to some extent, else there could be operational risks for the banks.

(Being from IT industry, I can sense that Bank Managements seem to be moving in incorrect direction…)

7 Likes

Banking sector seriously needs to be disrupted. They keep upselling products to aged and non tech savvy people.

The private bank people keep lying to customers in branches where things are not recorded.

There are so many social engineering frauds going on to loot the non tech savvy people.

Most of the data of Indians are available publically with their personal detials which is increasing the incident of fraud. The cases of cyber security does not gets resolved as they are too many and resources are few.

New age fintech are not doing any disruption. Their target people is mostly different due to their high cost of funds. All the current fintechs that I see are after giving loans to people at high interest rate instead of solving any meaningful thing. Collections at these fintechs employ all unethical tricks that you can think of.

There is proper case of disruption that needs to be done.

My guess is with the advent of large language model like chatgpt who can guide people over calls and while talking to any person will solve most of the upselling and frauds. It can also summarise long legal document of the bank. The bank other earnings needs to go.

Disclosure: Recently visited Axis bank branch. Have some experience in fintech in personal loan division.

6 Likes

Yes, there is lot of mis-selling happening in all banks today. Most of the times, it seems that, Banks do share private data of the customers to third parties and it reaches fraudsters easily. This is evident from large number of frauds happening in India which is unheard of in Developed Nations. This is very serious issue since I have worked in Cyber Security practice of large IT company, I am aware about this.

This is one of the reasons I do not personally use credit cards to pay bills, as Billers can misuse the credit card data though it is supposed to be masked or encrypted.

I agree that, FinTech industry has not solved the problem of cyber frauds in India and This is one major area which looks complete re-look.

2 Likes

Sharing an ET piece on HDFC Bank. It’s based on a recently issued research report. While I don’t care much about projections…

There’s a very important factual sentence in this piece that’s worth taking note of:

“Our zipcode-level analysis shows that HDFC Bank has added branches in areas with limited competition from private banks. In fact, 45-50% of new branches are in markets where leading private banks, such as ICICI Bank and Axis are not present,” said the Jefferies note."

To me this shows the willingness of the management to make a bet which is painful in the short term but has the potential to pay off in future.

Exactly the kind of long term thinking long term investors need to appreciate.

Discl: Interested

23 Likes

I like the strategy if bank expanding in rural currently where there is little competition, I also agree of misselling by bank RM’s I was not aware that banks sell our private data, if yes who and how are they selling this data, also I think regarding our credit card data if we only use it on some non reputed sites there is problem of it being used by fraudsters, else all card data is encrypted, using credit cards for 6 years now, never had a single fraud.

3 Likes

I work in a Bank. The attrition rate in the branch banking side has always been high. The inter bank poaching is one aspect. The quality of the hiring is also poor, since this is an entry level with a major part of salary is linked to incentives the hiring teams also do not pick the right candidates,

May people hired realise their interest in other things, go for higher studies, go to selling in other industry, study in parallel and switch. Further the people who do well carry on a move to a better roles while the new talent comes in.

I agree there is a need for the Banks to think of this talent pool differently.

2 Likes

I believe that, Banks should start using AI capabilities more seriously than present, to tap the right customers which are actually looking for Loans and Credit Card products, rather than randomly calling all customers for marketing Loans & Credit Cards.

Currently Axis Bank seems to be calling every week to sell such products. (This is my own personal experience and also shared by few of my friends). Here there is scope for massive improvement.

I have seen that, some younger customers who need Education Loans may not get it so it seems that, there is some gap between demand and supply.

If banks can plug these gaps, they might able to reach correct customer base.

Note : This is general observation and not related to specific bank.

Invested in HDFC Bank since 2011 onwards.

2 Likes

Are you speaking about the bank’s RM’s or operational staff in general.

HDFC bank shall have huge data and if monetised appropriately will be really nice, instead of the annoying calls everyday for loans AI can be really helpful, most of the fintechs that are able to expand rapidly do on the basis of tech/digital moat, the only issue I find in them is they are focusing on the bettering their tech, even after the recent updates the app is still poor with frequent crashes and if it can dominate through tech it will be the most dominant banks in physical as well as digital capabilities.

1 Like

Recently have done a Balance Transfer of LAP Loan from Edelweiss to HDFC and the whole process was really frustrating, plus other banks are offering better rates like Kotak, but since there is a pre-payment penalty does not make sense to switch again, as a customer even to get a simple statement for it is really time consuming, as the LAP was sourced through RM and a way to get a statement digitally is very hard plus hard some pre payment charges levied by bank for no fault of mine, and took am=lost 1.5 yrs to escalate the issue and get those reversed, I was assured of 0 processing fees but in the end I had to pay 0.25%, the amount of docs reqd etc it is really painful for a simple Balance transfer but a friend of mine recently got a Home Loan from Kotak, his experience was a lot better.

2 Likes

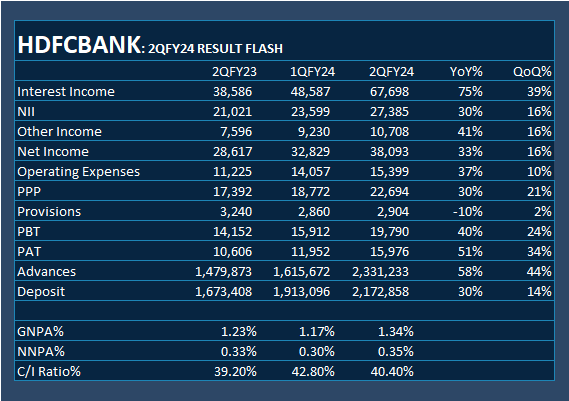

The Bank’s CASA ratio stood at around 37.6% as of September 30, 2023, as compared to 45.4% as of September 30, 2022, and 42.5% as of June 30, 2023.

I believe the focus over the next 4 quarters shall be on improving the CASA ratio and get it back to about 42-45%.

The numbers looks alright for the quarter considering this must have been a difficult one for the management to handle with all the disruption caused by the mega merger.

AJ

Disclosure: Brought during the last year and continue to hold. Closely watching the developments.

10 Likes

Q2FY23-24 QUARTERLY RESULTS

Concall

Concall Transcript

FINANCIAL

There was a lot of apprehension (including mine) about negative surprises emanating from the merger but the last analyst call and the results and concall from yesterday have alleviated such concerns to a large extent. The book value per share is ~553 and the annualized rate of earnings per share is ~89. This means that price to book at current market price of 1540 is ~2.8 and PE multiple is ~17.3 both of which are close to what they were at the height of the pandemic.

In other words, even after clarity on most aspects of the impact of the merger having emerged, the stock is trading at multiples (in terms of PB and PE ratios) that are close to their peak pandemic panic values. Is there something significant that am I missing here?

Disclosure: invested for a long term, recently added more.

12 Likes

ROUGH NOTES OF Q2FY24 EARNINGS CALL

Management Commentary

Mr. Sashidharan Jagdishan

- 1st result post-merger

- We just consummated one of the biggest mergers without any outside help – this shows the strength of our institution

- There was an incremental CRR that was announced and this cushion was very very helpful

- Day 1 adjustments to Equity mentioned in the presentation

- Some people mistook it to destroying equity – but they were just timing differences

- About the non-retail book of erstwhile HDFC – this restructuring brought about a spike in NPA… The accounts are yet current and performing. The bank will not see any loss from this book in the P&L. Our provisions too are adequate enough.

- Construction Finance: It is going to be an important part of our business. It will grow steadily from here on. This will help the top line as well as the margins.

- The results showcase the execution capability we are known for

- Deposits accretion of 1.1 lakh crore

- When the liquidity cushion was being built in eHDFC, we decided not to transfer some tickets – and this is what happened in June – that is why deposits were hit.

- Funding will never be an issue for us.

- Loan Growth: These are high-quality assets. Commercial, rural, MSME or retail – all are extremely high quality books. 4.9%, annualized 19.6%

- Very strong, very healthy numbers – bank will have the energy to grow at this pace

- Mid-September presentation mentioned a possibility of 25bps impact on NIMs for making the cushion. We are therefore, currently at the lower band. With time, we will recoup some of those margins. Especially with the changing mix towards retail.

- RoA: Maintained around the 2%, and RoE at the 16.2%. Therefore, topline growth and profitability is intact and will grow now onwards.

- We did the highest ever mortgage loan disbursements ever. We will now start to sweat the distribution system – along with digital bundling of products.

- The innate strength of the company is strong, we have demonstrated this year after year

- We are excited about the future

Mr. Srinivasan Vaidyanathan

- Macro Context: Good healthy tailwinds. Push from government through Capex.

- Key Logistic indicators were good. The environment is good for robust growth.

- Our estimate for GDP growth is 6.3%

- Key factors in the bank’s growth journey: Overall 10,436 branches increased YoY

- eHDFC branches we are working on building books of HDFC bank from those locations.

- 2.7 million liability relations added in the quarter

- Granularity and deposit focus continues.

- Term Deposits have been the bedrock of this growth. 7.6% growth sequentially.

- Retail accounts for 72% right now and this is our increasing focus.

- CASA was impacted due to merger

- We continue to pursue our tech foray. 3 million registered users on our app.

- Balance sheet remains resilient. CAR is at 19.5%. Core NIM was at 3.65%. Reported NIM was at 3.4%.

- Other income 10,708 crore – 65% is Fees and Commissions.

- Op Expenses 15399 crore represent Cost to Income at 40.4%.

- GNPA was at 1.34%. 22bps related to restructured account – which are current and performing but are classified as NPA

- Slippage ratio is at 33 bps

- 4500 crore of recoveries and upgrades in the quarter

- PCR was at 74%

- Credit Cost Ratio was 49 bps compared to 87 bps YoY. 34 bps net of recoveries.

- EPS (standalone 21.2) (cons 22.2)

Q&A

Mahrook Adajania – Nuvama

Q: On Margins, you’ve explained ICCR…but will there be any other adjustments while moving from IND-AS to IND-GAAP?

- We’ll have a session for IND-AS and IND-GAAP to explain it all

- There are a lot of differences that happen

- Profile of the balance sheet and interest rate structure are no longer comparable – there is a different regulatory regime

Q: So is most of the margin from excess liquidity and ICRR?

- The balance sheet is funded with debt

- Debt borrowing comes at a cost of north of 8%

- That is a part of merger management

- But when you think where it reflects, it is in the Cost of Funds

Q: There was a favourable decision in the tax rate…so does it normalize to 25% in the next quarter?

Yes. We will be at around 24.5

Q: How long would it take for the margins to come back to the 3% levels?

Utilization of better mix - focused on retail will help us bring it to normal levels.

Kunal Shah – Citi Group

Q: The Rundown in wholesale portfolio…is it largely done? As you said we should now be seeing growth…

- It has got 3 components

- Construction Finance – we want to grow this portfolio

- LRD book – Is also a growth oriented book

- Corporate Loan Book – We will take a decision about overall exposure. But direction is towards the better.

Q: Any one-off impact due in Fee Income due to IND-AS transition?

- Fee income is at normal level

- This is from multiple products but there are seasonalities – it goes up or down

- But historically, it is in the mid to high range

- This quarter it was at 19 odd %

Parag (Inaudible)

Q: Will there to be a 2% hit to growth rate? As you had said before …

- Growth rate is underpinned on 2 things

- Market Rate of growth from 10-12%. Depending on the growth. Nominal rate of growth x 1-1.1 will be our growth

- We have delivered a premium on the market rate of growth

- There is 400 bps growth in market share gain

- If you look at recent times, market share gain is faster than it was 5 years ago as opportunities to gain more market share are available.

- If you look at 2 years ago the cohort of branches we could see that breakeven happens in 2 years. As we add new branches, that is the average you can expect as it follows the scripted method ahead.

- For every 10 bps credit cost of opportunity from the timing point of view, it is about 1-2% of Cost to Income. As we make those investments, it will start to pay back.

Q: Till last quarter everyone was concerned about how you will fund. But going ahead, will listing of subsidiaries provide some value and funding?

When the timing is appropriate we will consider an appropriate valuation and let you know.

Atul Mehra – Motilal Oswal

Q: In terms of non-retail NPA, how much was un-anticipated and what was anticipated in the swap ratio?

- If you look at this book from a 6 quarter PoV, it has been on a decline. Go back to the June’22 quarter it was flat, post which it has been decreasing

- We want to grow this book, but before we do that we need to assess exposure for stability and to balance the risk

- We are currently comfortable with the provision coverage and the book is strongly positioned

Q: Did any incremental stress come as a surprise? Or was it already anticipated?

- Risk assessment is a dynamic process

- And it is a continuous process. It keeps changing.

Suresh Ganapathy – Macquarie

Q: 83-85% of the book is retail right? What is the comparable Basel 3 number?

- Yes

- But basel classification is different

- There is no 1-for-1 retail definition

Q: About the he synergy itself… counter share has gone up to 70% already, so what is the qualitative aspect contributing to this, can you some give light on that?

- We have focused on a few things. Engagement level has gone up significantly.

- The process itself. The sales process is significantly enhanced.

- Process has to be broad based across the country and that has already begun.

Abhishek Murarka – HSBC

Q: Can you quantify the LCR on a merged basis? And retail deposit # on a LCR basis of HDFC deposits?

- 121% after absorbing the ICRR

- There is no special tracking now, it is all part of one

Q: In terms of conversion to repo-linked loans…?

- That all has already been done

- December deadline if for customer communication

Rajeev Pathal – G3 Holdings

Q: There has been a 3% hit on the margins due to ICRR, will it start getting normalized from the next quarter? Do you think 4-5% growth in loan book is possible?

- We don’t give forward looking guidance

- We did allude to the margins and merger management – it has been long-term debt funded

- It will take some time.

- Better mix, and higher yielding retail mix will help us get there

Kiran Engineer - CLSA

Q: What are the SLR Issues as of Quarter-end?

We don’t say what it is, but we can say that we can carry more than that number.

Q: On branch opening, why is it subdued, and why is always back-ended?

- You ask a very important question

- 1st thing that goes in is the marketing team – to decide the location

- Followed by the credit team which maps the geography to potential for advances as well as deposits

- Our branches are 4.5% of country’s branches

- Our deposit margin share is near 10%

- We see the potential in the catchment area

- Then Infra team will say if they can build or not build it

- We know where we want to open the branches, but availability of the right space is a constraint.

- Then we go through this process and bunch it up. As much as we like it to be even through the year, but there are other constraints. And this is like a machine. The prep that goes in leads to a very long lead that goes in. Therefore, it is sort of cyclical.

Q: How much of slowdown is market-led?

- Market is under-penetrated

- Our pre-approved personal loan rate is high and demand is good

- We are at a 15-15.5% growth rate. Sometimes it is higher, currently we are in this 15% range – as we go ahead our canvas on personal loans will grow even more.

Manish Shukla – Axis Capital

Q: What is Average cost of liabilities acquired from HDFC?

- Cost of funds is up by 85bps – and most of this is from incoming eHDFC book.

- So you can calculate from what is already available

Closing Comments

- We are available through the next week for any other clarifications

- Please stay in touch. Thank you.

X.

15 Likes

Due to the large base of HDFC Bank, it will not compound at the historical rates of return.

Plus since it is a 100Billion plus valuation, it will be compared with global peers, who trade at much lower than 2.8x book value.

This is what makes making outsized returns in HDFC Bank (>20%) totally out of question.

Hence this isn’t a very interesting name for most if they are investing in individual stocks I feel.

Better to put money in an index vs HDFC Bank, less tracking to do and almost similiar returns

2 Likes

CASA Ratio has been dropped to 37.6% compared to Last year 45.4%. Is there any comment for this drop?