Q4FY22-23 Results

Rs 19/sh dividend declared

Financials

https://www.bseindia.com/xml-data/corpfiling/AttachLive/223e6561-0adf-4050-896c-515773148a99.pdf

Q4FY22-23 Results

Rs 19/sh dividend declared

Financials

https://www.bseindia.com/xml-data/corpfiling/AttachLive/223e6561-0adf-4050-896c-515773148a99.pdf

HDFC Bank Q3 concall highlights-

Industry Mkt share in Advances at 11 pc, in Deposits at 10 pc

Customer base at 8.3 cr

Total branches at 7821 (opened an avg of 04 branches per day in FY 23 !!)

52 pc branches in rural and semi urban areas

Credit card Mkt share at 28 pc !!

NII - 24940 vs 20350 cr, up 23 pc

Non Interest income - 9610 vs 8380 cr, up 15 pc

Operating expenses - 14590 vs 11010 cr, up 33 pc (due massive branch expansion)

PPOP- 19960 vs 17720 cr, up 14 pc

Provisions- 2680 vs 3320 cr, down 21 pc

PAT (consol)- 12590 vs 10440 cr, up 21 pc

Total Advances at Rs 16,14,200 cr, up 17 pc

Total Deposits at 18,83,400 cr, up 21 pc (big achievement)

Cost/Income at 42 pc- despite massive branch expansion

NIMs at 4.1 pc vs 4.0 pc

RoA at 2.2 pc

Capital Adequacy at 19.3 pc, Tier-1 at 17.1 pc

Retail:Wholesale deposits at 83:17

Retail:Wholesale Loans at 47:53

10 yr Advances CAGR at 21 pc

10 yr Deposits CAGR at 20 pc

10 yr PAT CAGR at 21 pc

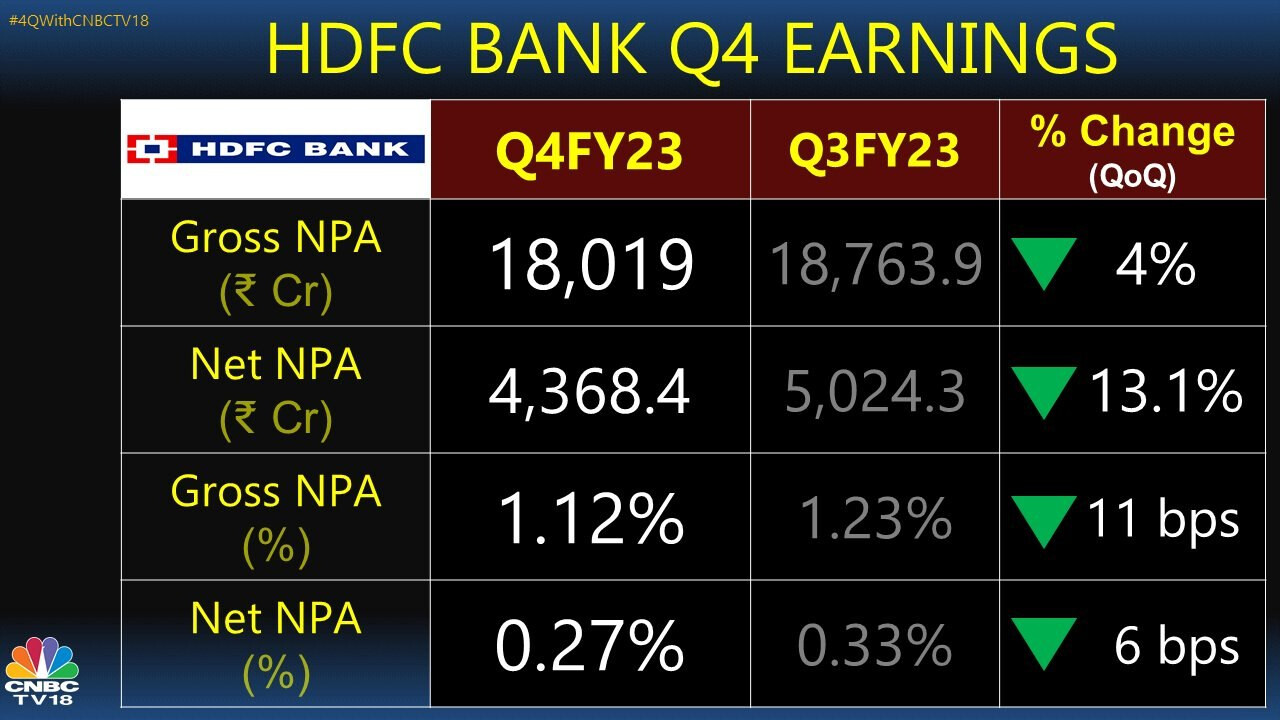

Asset quality-

Gross NPAs - 1.1 vs 1.2 pc

Net NPAs - 0.27 vs 0.33 pc

Bank’s POS machines currently operational at 39 lakh, up by 30 over previous FY end

Bank’s merchant App- Vypaar added 75,000 merchants per month in FY 23

Branches offering wealth management, now over 900 vs around 700 LY

Branches offering gold loan at 4182, up by 3X vs Mar 22 (bad news for gold loan companies)

Added 1.06 cr new liability customers in FY 23!!

Employee addition in FY at 31600 !!

CASA ratio stands at 44 pc

Q4 loan growth breakup -

Retail loans up 21 pc

MSME and priority sector loans grew by 29 pc

Wholesale loans grew by 12 pc

Express car loans gaining tremendous traction, now constitute 20 pc of all car loans

Slippage ratio for Q4 was 28 bps (this is too good)

Recoveries and upgrades in Q4 were 22 bps (awesome)

PCR at 76 pc. But if u add contingent, general and other provisions, this jumps to 176 pc of GNPAs (eye- popping)

HDB Fin Services (subsidiary) reported improvements across loan growth, PAT and asset quality. Its full year PAT almost doubled to 1950 cr !!!

HDFC Securities revenues and PAT de-grew slightly in Q4. Full yr PAT was 777 vs 984 cr LY

CV portfolio of the bank grew 11 pc QoQ (V Strong growth)

Benign credit cost cycle allowing the bank to go full throttle on branch expansion without worrying too much about expenses

43-44 pc loans are fixed rates loans with avg tenure of 2.5 yrs

Retail loan book : Wholesale book to grow because of aggressive branch expansion

Branch addition speed ( which is already hyper ) to continue in FY 24 as well, subject to Qtly evaluation

Full benefits of this hyper addition in branches to be visible in 2-3 yrs as new branches and new customer relation start to mature

Merger may get completed by July

My take -

Exceptional performance wrt deposit mobilisation, asset quality, slippages, provision coverage, acceleration in retail loans

No discussion on Bank’s planned all new Website / user interface was a disappointment

Performance on most operational metrics - Superb

Disc: holding, biased

MERGER UPDATE

Investor day

Question for experienced folks

Would the breach of 10% holding limit for mutual funds create pressure on price in coming weeks. What is the likely scenario.

Thanks

IMO… this is known to the Mkt for over 2-3 months now. A lot of rejig would have happened by now. Some more may be left

Should not be such a big issue …imho

HDFC Bank reports margin contraction, decline in EPS, and an increase in NPA. But the management strongly believes that there is a seasonality effect in Q1 and growth will pick-up here onwards.

There was emphasis on the fact that the company never engages in “deposit-pricing wars” to gain market share and will continue to focus on building a better relationship with their clientele.

Mr. S. Vaidyanathan, CFO

Merger update

General Update

Key Themes

Other Income

In the medium and long term, customer reach is the key.

HFL

Continued strength has been shown. PAT increased by 30%. RoE of 17.3%. EPS is at 22.2 at consolidated level.

Q: On deposit growth. Quarterly fluctuations are there but on incremental business, it seems like you have lost market share.

Q: On advances, the merged entity grows at 15% but you said it has grown at 18%. What number to go by?

Q: Can you sustain the current levels of RoA?

Q: On Opex, this also happened in the last year’s Q1, Opex growth scales up in the 2nd half (600-700 branches in each quarter in the 2nd half). 8% sequential growth, will it come back?

Q: On loan growth and incremental deposit growth. Loan growth you had indicated doubling of growth – merged balance sheet has grown at 13%. Can we see 17-18% growth as we end the year?

Q: Would you be able to quantify the CRR and SLR for the quarter?

Q: On retail deposit side, last time it was quite encouraging. Q1 has some side of seasonality but with the investment and capabilities we have, what is the traction you see for the next 7-8 quarters?

Q: Credit growth doesn’t account for IBPC (inter-bank participation certificate) , right?

Q: What will be the Integration costs with respect to the merger?

Q: On deposit cost, Interest cost is up sharply QoQ. On HDFC mortgage book, it is already repo-linked, right?

Q: What impact will it have on NIMs?

Q: Going to your statement of you using low credit costs to expand – till when will you be able to sustain this?

Q: On segmental growth, home loans have picked up. Everything else is subdued. Is this effort…or only quarterly phenomenon?

Q: Any incremental colour of PSLC, RIDF?

Q: Any one time costs expected from the merger?

Q: On wholesale book, how much is left to rundown?

Q: On deposits, incremental deposits market share is at 25%, but we are at 20% right now –so incrementally would you have to raise rates to fill this gap? Will this lead to stickier rates on the Cost of Funds?

Q: Is RoA calculated on quarterly bank balances?

We will share with you the denominator

Pranav – Burns (?)

Q: If we didn’t go down the IBPC route, what would’ve been impacted? What would you have to sacrifice?

X.

Ps. There have been certain omissions/paraphrasing in these notes. It is not a word-for-word transcript

FY23 AR has optimistic tone for the just concluded merger of HDFC Ltd. Snippets:

The merger has come into effect from July 1, 2023…The merger perhaps could not have been better timed…… plan to contribute to the growth of affordable housing, as over half of our branches are in semiurban and rural locations……completes our product suite through the addition of home loans……. This would enable the Bank to serve its customers in a significantly enhanced way with a bouquet of financial services…..merger has now been completed within our estimated timelines and focus now shifts on capturing the full benefits of the synergies and future proofing the Bank for the coming decades….Buying a home is a family decision and an emotional one. This emotion is transferred to the home loan service provider and helps build lifelong bonds with the customer and his family. Also, only 2 per cent of our customers source their home loans through the Bank, while 5 per cent do it from other institutions. This itself is a huge opportunity. It is this bond with the customer that the Bank would like to build on. HDFC Bank with its stronger digital platforms, digital journeys and physical branch network will have the ability to offer the home loan customer a complete bouquet of the Bank’s and subsidiaries’ products and services. Savings accounts, personal loans, insurance cover, SIPs can all be bundled along with a home loan to create a compelling value proposition to the customer, that probably does not exist in the market at the scale at which this is envisaged……A bigger balance sheet post merger will enable HDFC Bank to take a larger exposure in infrastructure projects. This means we can participate more meaningfully in India’s growth story and contribute to nation building. In light of all this, the pace at which we aim to grow - we could be creating a new HDFC Bank every 4 years…..The merger with HDFC Limited is a positive for its long term growth story with the addition of the home loan product to its portfolio opening up a significant runway.

However, market valuations indicate that merger is equivalent to COVID moment for the bank.

| March 2020 (COVID) | March 2020 (COVID) | July 2023 (Post-Merger) | |

|---|---|---|---|

| HDFC Bank | HDFC | Merged Entity | |

| Share Price | 813 | 1500 | 1685 |

| Share Qty (Cr.) | 540 | 346 | 754 |

| Mkt Cap | 439020 | 519000 | 1270490 |

| PAT | 27296 | 22826 | 64158 |

| Equity | 176350 | 126479 | 444946 |

| P/B | 2.5 | 4.1 | 2.8 |

| PE | 16.1 | 22.7 | 18.8 |

How did you calculate the pe for merged hdfc bank? That seems totally wrong.

It seems like earnings of hdfc ltd and hdfc bank was just added, but large part of hdfc ltd earning is through hdfc bank due to the shares it holds. So the earnings of the combined entity is lower than the sum of consolidated earnings of hdfc ltd and hdfc bank.

The real pe ratio should be around 20

Yes, I missed the point you highlighted. Thanks. Revised numbers in my previous note.

Perhaps its the size of HDFC Bank which is the limiting factor here. (in terms of market capitalisation)

It is already among the 10 largest bank in world by market cap. (after merger with HDFC Ltd), the data is wrong by around 20% on the above site I linked (around 7th or 8th largest by market cap)

The 4 largest Chinese banks each have 15-20x assets of HDFC Bank and 15-20x net worth. Even if I assume HDFC merger is not reflected properly in net worth on the above site, their net worth and assets are still 10x of HDFC, and yet they have same market capitalisation. (But they are PSUs).

According to me, it seems like the sheer size of HDFC Bank is very large. Perhaps the market is pricing slower growth for HDFC Bank in future, perhaps NIM contraction or higher NPAs or something done by government to ensure that 1 or 2 private banks dont capture the whole market?

The data is slightly wrong on this site. The market cap of HDFC Bank is off by about 15-20 %, but still, HDFC BANK is among top 10 banks by market cap.

I think I understand it now after looking at Q1FY24 presentation and the transcript of the Q1FY24 conference call. The merged entity’s loan growth [earnings] would be under pressure in the near-term compared to the norm (consistent growth of 17~18%). 2 factors stand out:

![]() Funding concerns arise after a $40 billion merger between HDFC Bank and HDFC.

Funding concerns arise after a $40 billion merger between HDFC Bank and HDFC.

![]() HDFC Bank seeks forbearance from RBI but faces challenges with Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR) requirements.

HDFC Bank seeks forbearance from RBI but faces challenges with Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR) requirements.

![]() HDFC Bank’s merger may impact Net Interest Margins (NIMs) due to increased low-interest yielding housing loans.

HDFC Bank’s merger may impact Net Interest Margins (NIMs) due to increased low-interest yielding housing loans.

![]() HDFC Bank aims to return profitability to historical levels in 18 months.

HDFC Bank aims to return profitability to historical levels in 18 months.

![]() HDFC plans to raise ₹50,000 crore from bond issuances for liabilities management.

HDFC plans to raise ₹50,000 crore from bond issuances for liabilities management.

![]() HDFC scrip closes down at ₹1,619.05 on the BSE.

HDFC scrip closes down at ₹1,619.05 on the BSE.

Investor day recording

Merger related nitty-gritty discuss in detail

Final minutes intersting view of management why they let go large corporate deposit client

I was outfoxed in anticipating the combined BV, which is now published officially in the latest presentation - Link. However, even the big fish like Nomura seems to be in a similar situation:

Disc: Hold position in family account.

Nomura is absolutely right…

The old so called PSU banking era is over ! Why pvt banks become bigger without applying any considerable efforts, is because of PSU banks.

PSU’s loss is Pvt’s profit. They have looted the nation in many ways. Todays wealth distribution gap is gift of this guys(pvt banks).

If u see the banking sentiment in the country has changed very slowly and progressively. See last 2 3 yrs BS of PSUs. You will find they have done tremendous job , and story continues…

Who will be the biggest loosers of psu’s gain off course pvt banks.

And the sweetest credit cycle is just started, if any black swan event not comes then psu’s will be much more than their current levels.

So the money completely shifting from large pvt banks to PSU basket.

Disc. Invested in canara and jk bank.

This Article from Morning Context (June 2022) captures some of the issues which might be playing out now (read the investor concall HDFC management had recently and the share selloff since then)

“Is HDFC’s merger with its subsidiary a bailout plan?”

Read more at: Is HDFC’s merger with its subsidiary a bailout plan?

The attrition is problem for all banks: