All along we knew, its pathetic IT System Will hv hundreds of restrictions of what u can do/ for what period you can get data and which format and at what time. They are more clear about what you can not do. They were blind to their obsolete IT system design. I also use ICICI and hdfc bk is way behind. Only reason we stick is perceived sense of security.

But now u see their IT bugs coming out of cup board.

I had worst experience when their IT system was down and branch just cant help for cash deposit. Other branch will levy non home branch charges. And no one can help customer even when problem is their side. I mentioned same in this forum earlier.

All such things at times go under carpet with charismatic leader at helm. Just one possibility.

It may not go down but may definitely loose its mojo.

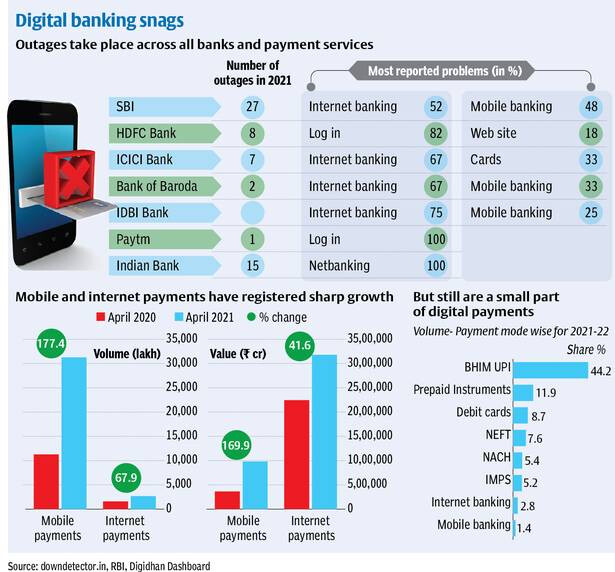

A bank of HDFC’s caliber should not be in the top of outage list. Though I am not an HDFC bank customer I understand the frustration of tech glitches. Aside I am very surprised to see ICICI bank at #3.

Thanks.

Another surprise…

just wanted to load this fy statement. i went to tedious path of statement loading as normal screen allows only 2 months of statement.

surprisingly after giving details it says come back after some time as we will be ready with your required statement data.

I waited for few minutes it says statement being prepared for download! Heght of user-unfriendliness!

With brokerages coming in with buy ratings (or reiterating the same) and RBI easing stance on asset quality projections it seems the banking sector ‘could’ be out of the woods.

The landscape for HDFC bank is marred with its tech challenges on the retail front. But I trust they have a task force for the same. Better late than never.

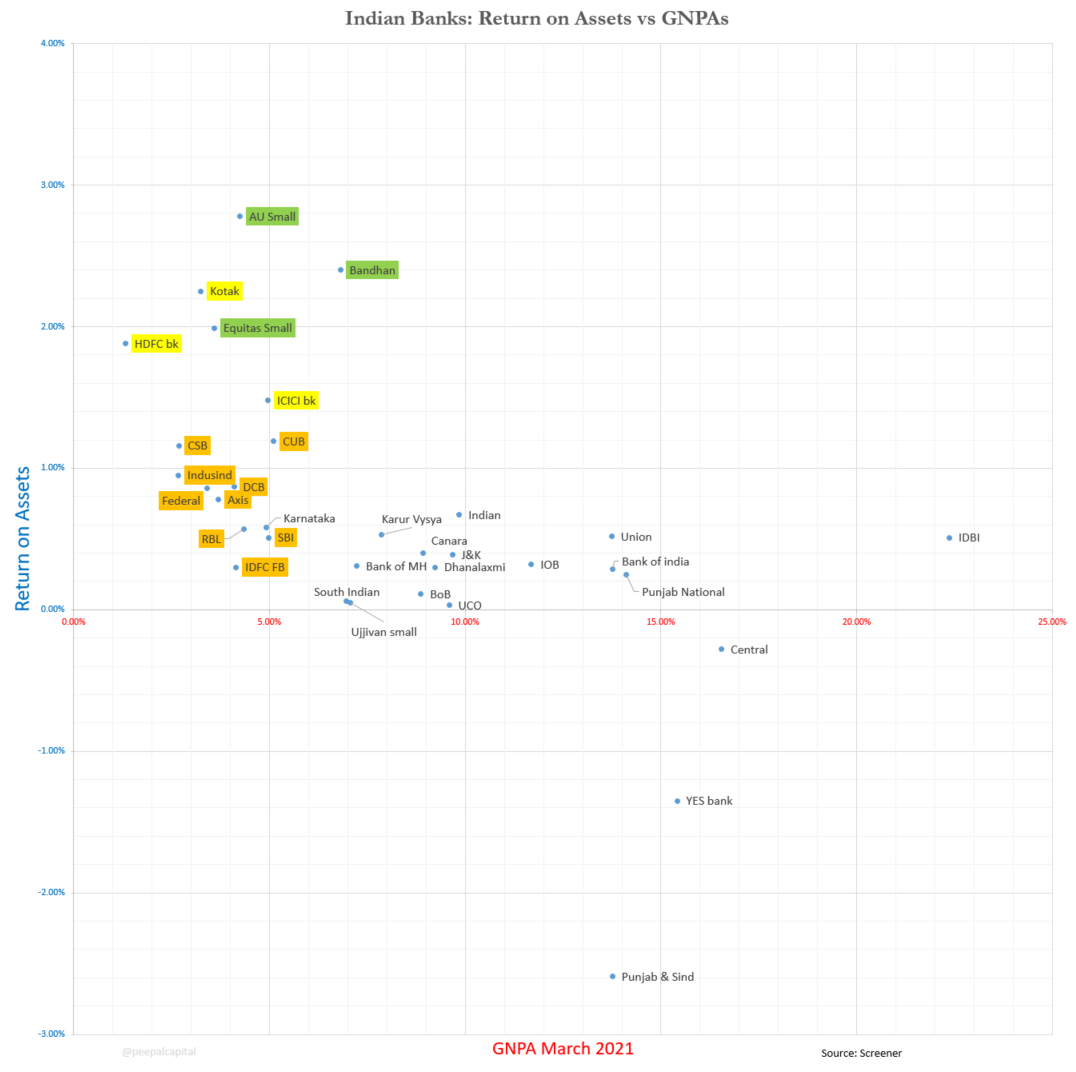

Looking at the entire set of 35 odd listed banks HDFC bk is the only one which exited at sub 2% GNPA with a top 3 or 4 RoA. This balance going forward will be important even in the event of slowed growth. My belief (not quantitatively) is that we might get above index returns in the next 2-3 years but not a wild run like the smaller caps. I guess no one expects that. Risk reward is in favour of HDFC bank in my books for the next few years.

Chart for reference below. (please click to enlarge)

These are only my personal views some based on quantitative data and some subjective.

Rgds

Deepak

Disc: continue to be invested in HDFC bank. SIPed last 30 days. Also invested in Kotak and ICICI and minor positions in 2 others. Not a registered RIA/RA/PM.

The Board of Directors at its meeting held on June 18, 2021 recommended a dividend of 6.50 per equity share of face value of 1 each out of the net profits for the year ended March 31, 2021, subject to approval of the shareholders of the Bank at its ensuing Annual General Meeting. Effect of the proposed dividend has been reckoned in determining capital funds in the computation of capital adequacy ratio as at June 30, 2021.

Increase in NPA in HDFC Bank and especially HDB Fin is getting highlighted and rightly so.

However, another aspect that should also be highlighted, that most large private banks (incl HDFC Bank) are raising additional capitals through bonds, QIPs etc inspite of being sufficiently capitalized well above the regulatory norms and having already provisioned adequately for existing NPAs.

Indicative of a high growth phase, these banks are anticipating post COVID where PSU Banks are contrained to expand their lending due to capital constraint (barring the top 2-3 PSU Banks).

The megatrend of PSU Bank to Private Bank seems to be accelerating.

NIM and Capital Adequacy Ratio look intact, but Provisions and Contingencies, and NPA’s are trending upwards.

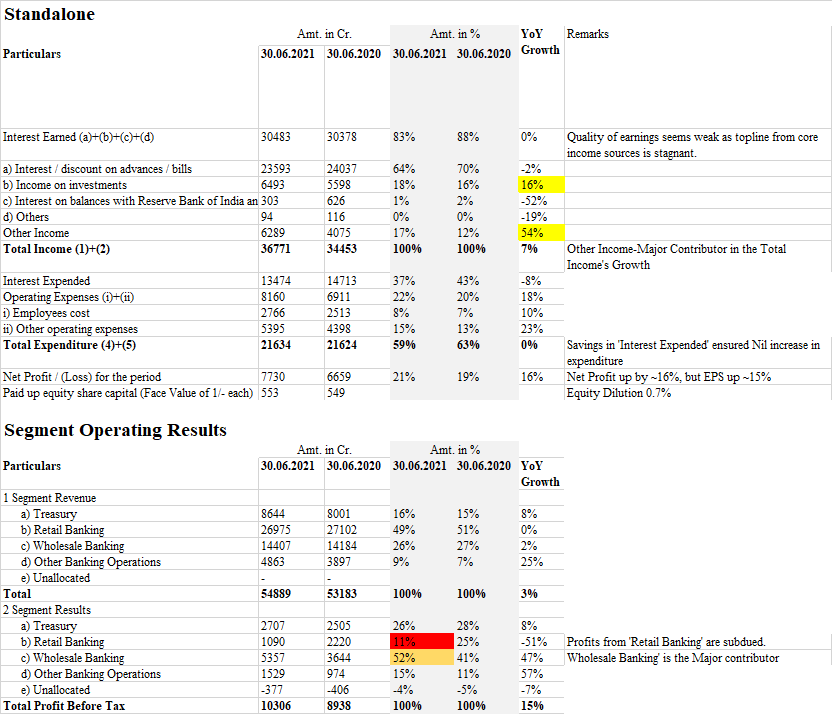

Net profit is up by 16% but the quality of earnings seems to be weak as the same is not coming from the core sources. Profitability from Retail Banking is under pressure, but Wholesale Banking is doing the heavy lifting.

Refer column named ‘Remarks’ for additional comments in the below snapshot:

Hi, I have the below two questions if someone can help.

In the Q1 2022 concall, an analyst said that the total slippage is 73bn out of which contribution of agri is 9bn. How to compute/reconcile these numbers from the quarterly statements released?

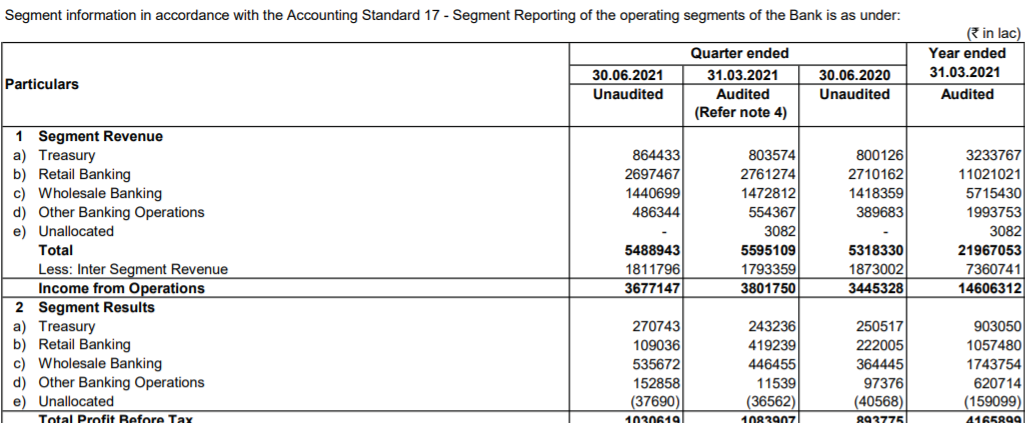

How come retail banking profits fell by ~ 75% (4192 Cr to 1090 Cr) while the revenue is more or less stable?

On the first one, i could see that the management quotes the number of annualized slippage ratio of 2.54% which will result into the aforementioned slippage (compared to the previous quarter ratio of 1.66%).

On the second point above, is it due to most provisions assigned against retail loans??

This looks a positive thing for HDFC Bank. While we appreciate strict action by RBI in this case, we always find it difficult to understand that, other private and PSU banks also have substantial issues either with their non-working ATMs, systems, but we have not heard of strict action against them so far. I have faced an issue of my investment disapprearing suddenly for few days from one reputed private bank web site. So such cases of technical failures / errors are common across many banks. We would appreciare that they also learn a lesson from this and improve their systems/ATMs/Non working systems in the bank branch.

“The sales teams have been asked to meet a target of issuing 500,000 cards a month starting September for the next few months,” said the source with direct knowledge of the matter.

RBI vide its letter dated August 17, 2021 has relaxed the restriction placed on sourcing of new credit cards. The restrictions on all new launches of the Digital Business generating activities planned under Digital 2.0 will continue till further review by RBI.