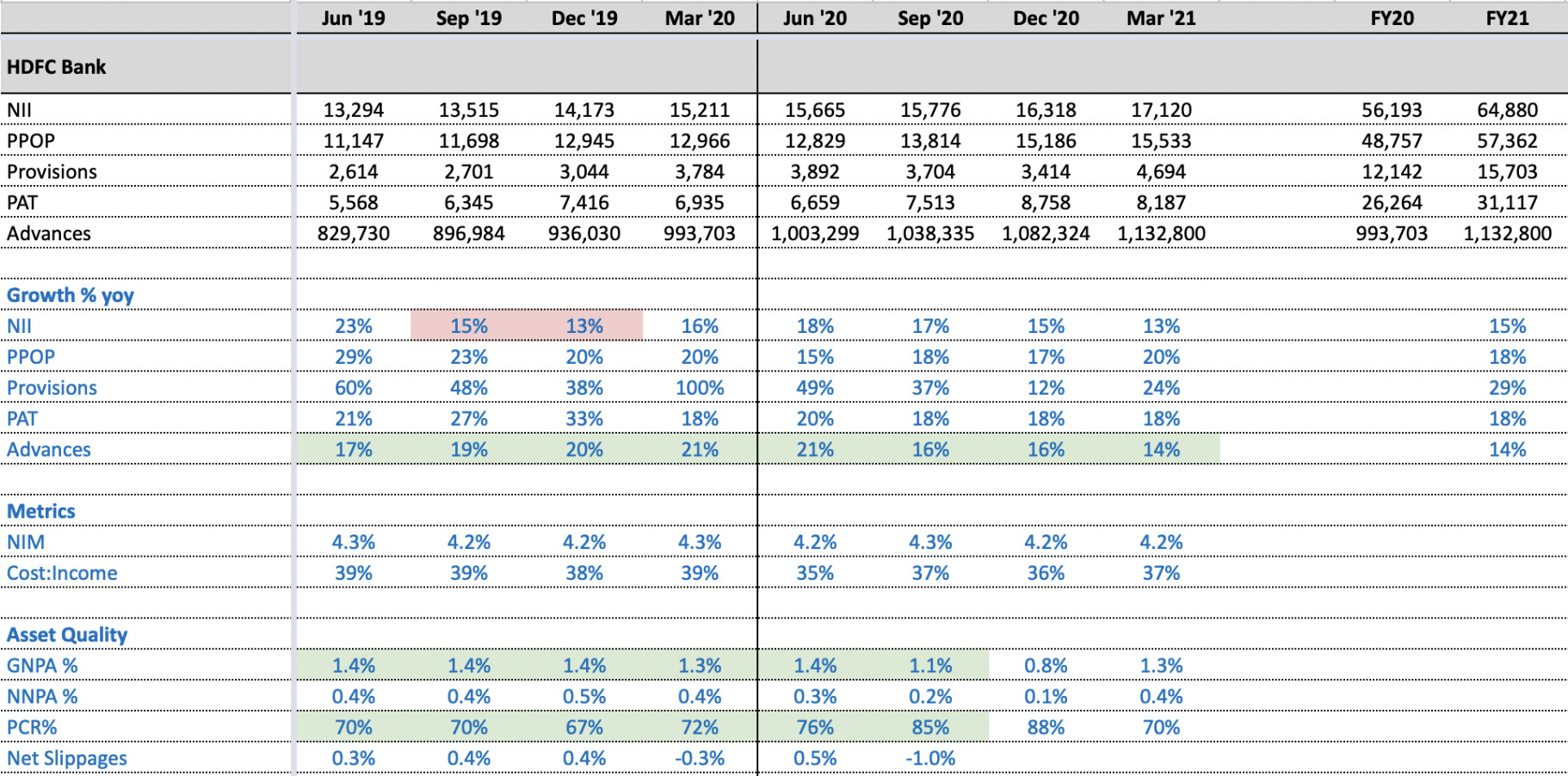

🏦Profits grow at 18.2% 🏦Asset quality remains stable with credit costs at 1.65% for the quarter 🏦CAR at 18.8% 🏦Gross NPAs at 1.32% vs 1.38% 🏦HDB Financial returns to profits

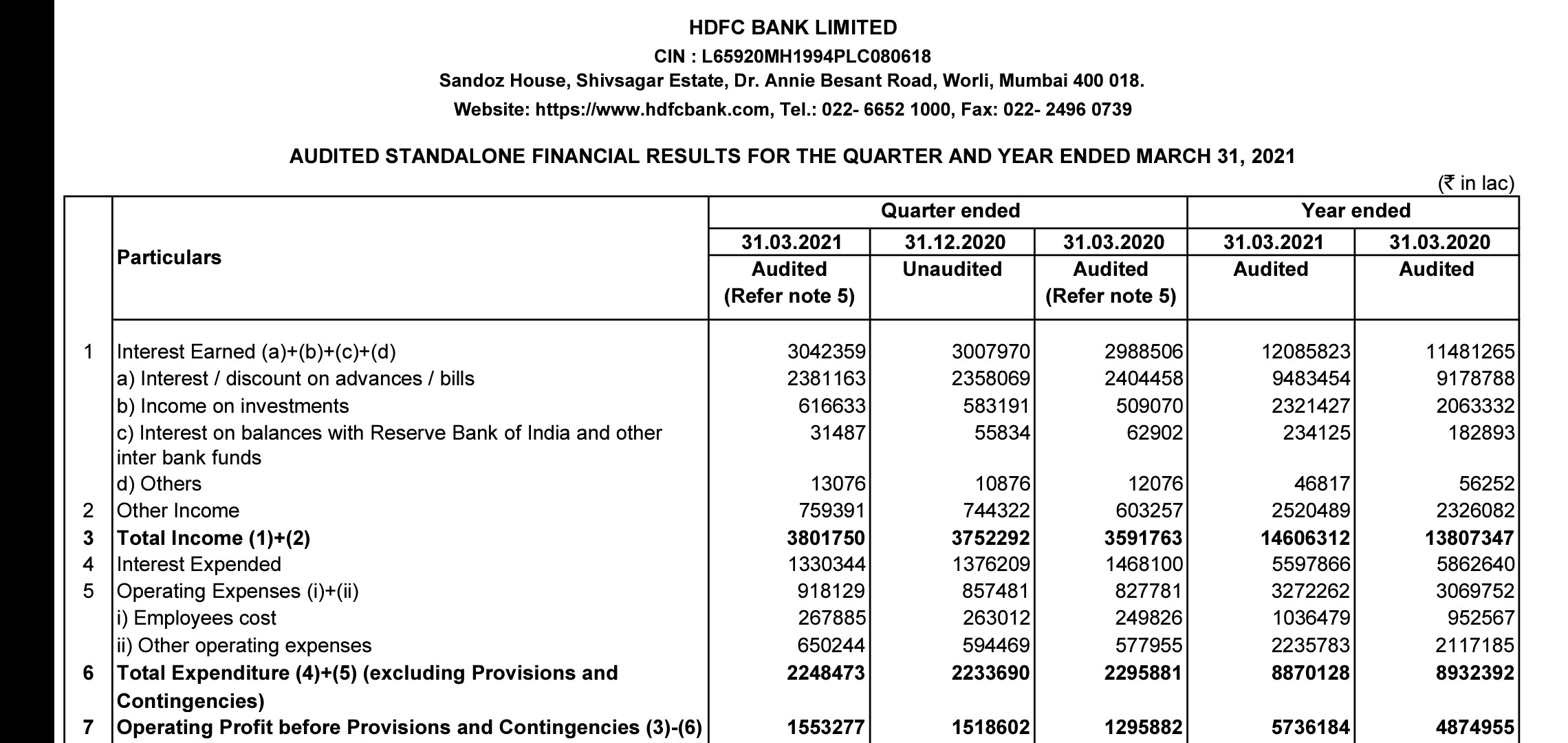

I am not sure where do you see the reduction in Interest income (I have attached recent Standalone Income statement).

Also, we need to see this income in light of falling interest rate (please see the reduction in Interest expanded). Given that overall Interest rates are going down, maintaining 4.2% Net interest margins is not bad.

In view of the ongoing stress and heightened uncertainty on account of COVID-19, it is imperative that banks continue to conserve capital to support the economy and absorb losses. In order to further strengthen the banks’ balance sheets, while at the same time support lending to the real economy, it has been decided that banks shall not make any dividend payment on equity shares from the profits pertaining to the financial year ended March 31, 2020

Does the bank hold a separate call for foreign investors? Was surprised at Saturday’s call - hardly 20 minutes of Q & A session. And the timing too seemed eminently unsuitable for FIIs - it would have been Saturday 7:30 AM at that time in New York. Surprising for India’s leading bank and one that is listed on NYSE and 40% foreign owned.

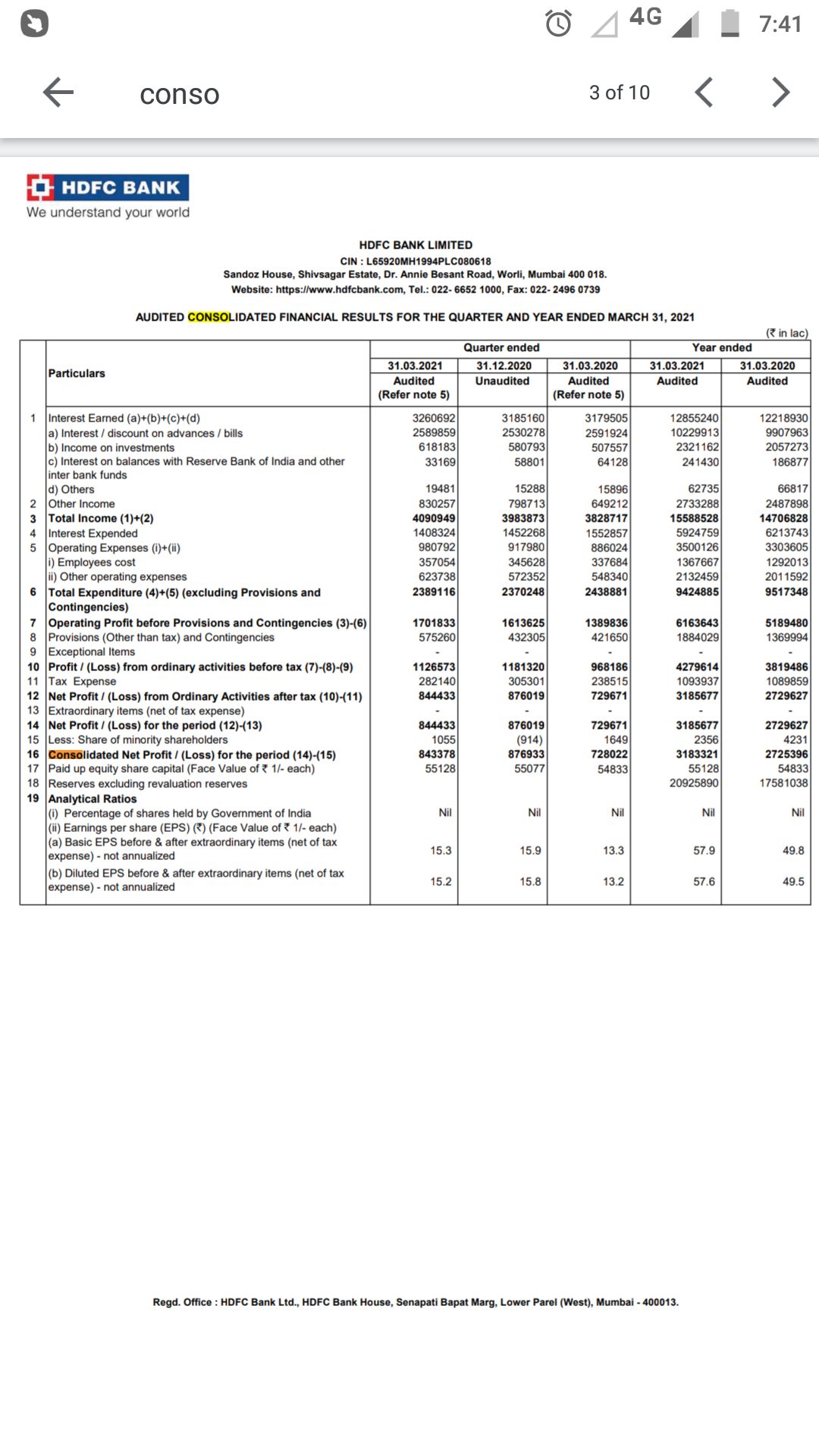

This is how I understand the results (standalone only - consolidation will make a marginal difference) -

% of Gross NPAs to Gross Advances (1.32%, which was 1.26% in FY20) and % of Net NPAs to Net Advances (0.40%,which was 0.36% in FY20) looks Ok

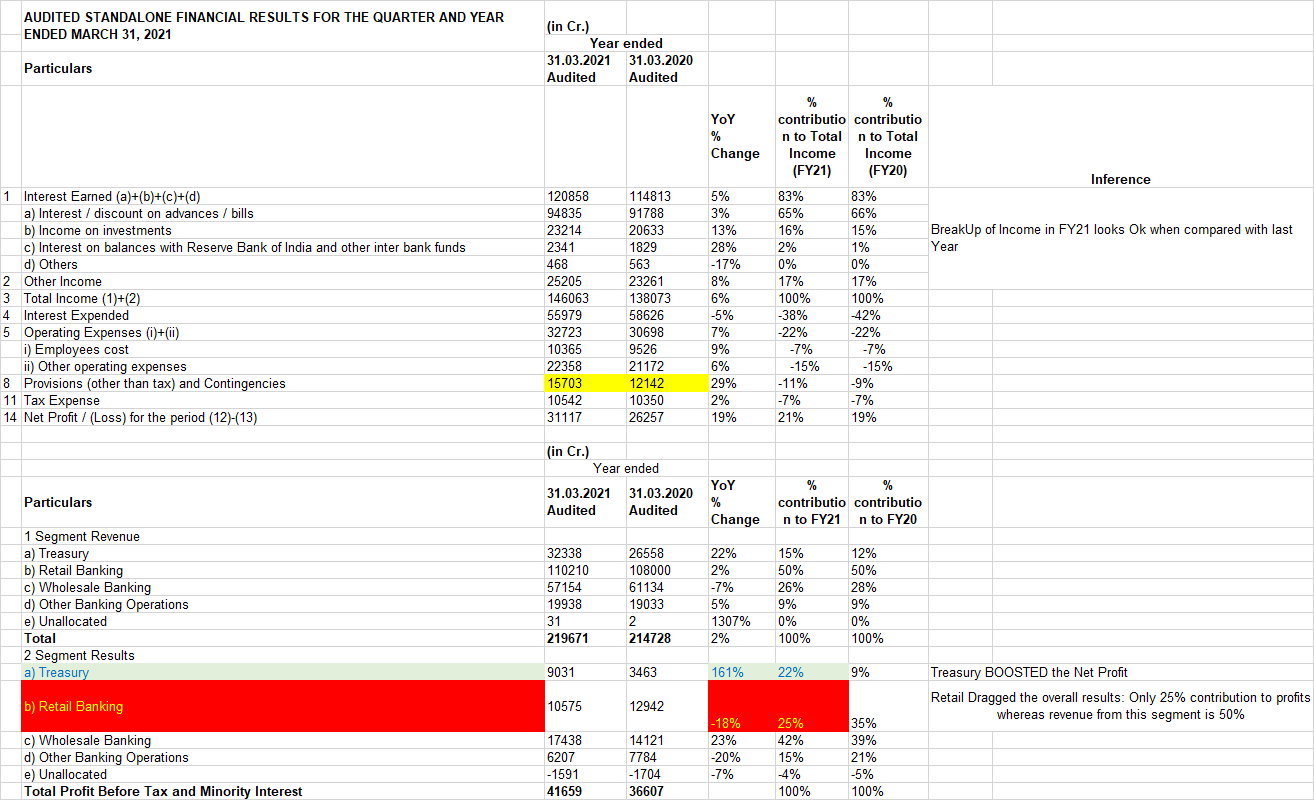

Breakup of Income in FY21 looks Ok when compared to last FY

In FY21, Treasury segment BOOSTED the Net Profit immensely whereas Retail dragged the overall results (only 25% contribution to profits whereas revenue from this segment is 50%). Need to see how it pans out for other banks in coming days.

Key Notes:

Note-6 Excerpt: … Given that the current “second wave” has significantly increased the number of COVID-19 cases in India and uncertainty remains, the Board of Directors of the Bank, at its meeting held on April 17, 2021, has considered it prudent to currently not propose dividend for the financial year ended March 31, 2021. The Board shall reassess the position based on any further guidelines from the RBI in this regard.

Note-11 Excerpt: … If the Bank had classified borrower accounts as NPA after August 31, 2020, the Bank’s proforma Gross NPA ratio and proforma Net NPA ratio at December 31, 2020 would have been 1.38% and 0.40% respectively. Pending disposal of the case, the Bank, as a matter of prudence, had made in respect of these accounts a contingent provision, which was included in ‘Provisions (other than tax) and Contingencies’.

Disc: Invested and have done transaction in last 4 weeks

RBI imposes a 10 cr. fine (largest ever fine) for irregularities in HDFC bank’s auto loan division. HDFC bank had previously investigated this issue and found misconduct from some employees, 6 of whom were subsequently fired.

I was aware from linkedin that they are setting up a separate team for all the tech troubles they have landed themselves into and a future roadmap. If I look at it positively the intent and effort is in the right direction, from a negative lens I hope this is not too late.

Aside the rumoured partnership with the Turakhia brothers is something I will watch very closely. They have been one of the best entrepreneurs of the country in my books.

A dividend of Rs. 6.50 per equity share of face value of Re.1/- each (i.e. 650% on face value) out of the net profits for the year ended March 31, 2021, has been recommended.