With this sale, Abrdn will completely exit HDFC AMC and that’s a relief

Would be interesting to see who buys the stake

With this sale, Abrdn will completely exit HDFC AMC and that’s a relief

Would be interesting to see who buys the stake

Thank you for the update! what will be the implications for this?

I can’t think of anything negative. It’s just a silent / sleeping promoter selling their entire holding in the company. If it’s bought by a strategic investor OR the main promoter HDFC Bank, then it is positive.

Lot of foreign & domestic funds have bought in the stake sale.

Interestingly, SBI MF has bought almost 4% and has taken it’s stake in HDFC MC close to 7% (Note: Navneet Munot is ex-CIO of SBI MF before he joined as CEO of HDFC AMC)

SBI MF is the second major non-promoter shareholder behind LIC which holds 9%

The main issue is growth, there has been substandard growth, that needs to be sorted out.

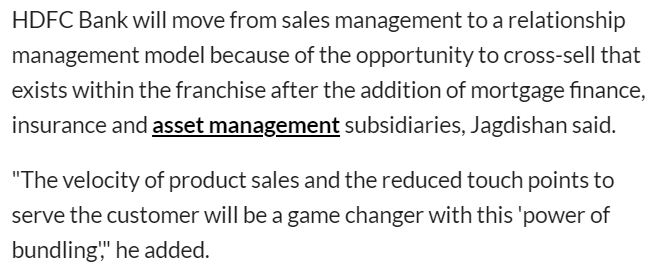

Counting on what the HDFC BANK CEO has said recently… Since all group companies have a single parent - HDFC Bank, the growth of subsidiaries is also a responsibility of the bank now. Hoping that they really use the cross-sell opportunities

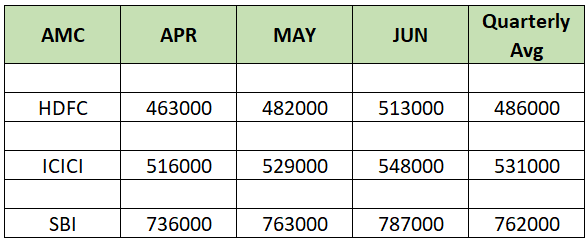

Seems the growth in assets continues for HDFC, the June numbers seemed to have crossed 5 lakh crores and reducing the gap with ICICI

The below aum numbers are from www.amfiindia.com, except for June which is calculated by deducting Apr & May numbers from the Apr-Jun quarterly aaum

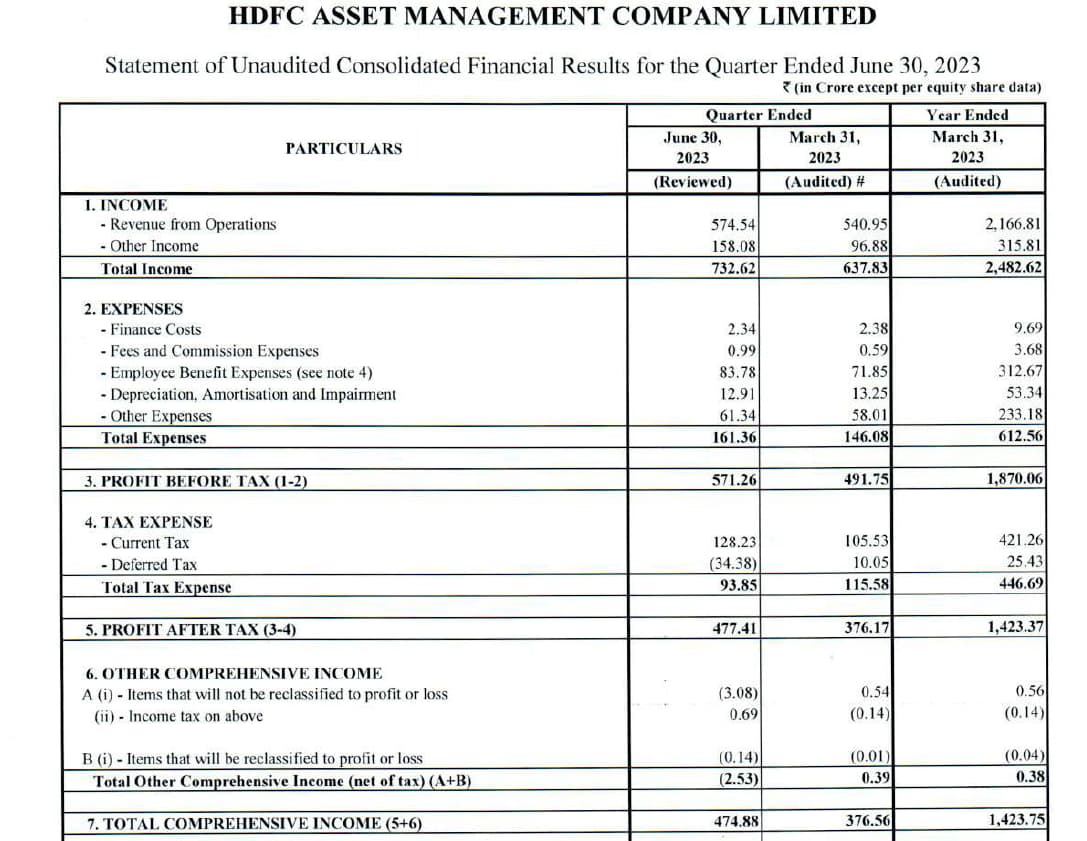

Good set of numbers. On expected lines as the AUM growth was already known.

ICICI AMC with additional 41000 Crores AUM also has reported same profit of 474 Crores (from ICICI Bank Q1 investor presentation). But HDFC had some deferred tax benefits

What is the source of other income? Does HDFC AMC have any other revenue stream?

It primarily relates to what they call as Mark To Market gains arising due to increase in stock prices. I don’t know how the fee income (revenue) and MTM gains (other income) are calculated based on AAUM (the increase of which is the result of inflow into funds and increase in prices of the fund held shares). It would be really helpful if any knowledgeable member can share the details

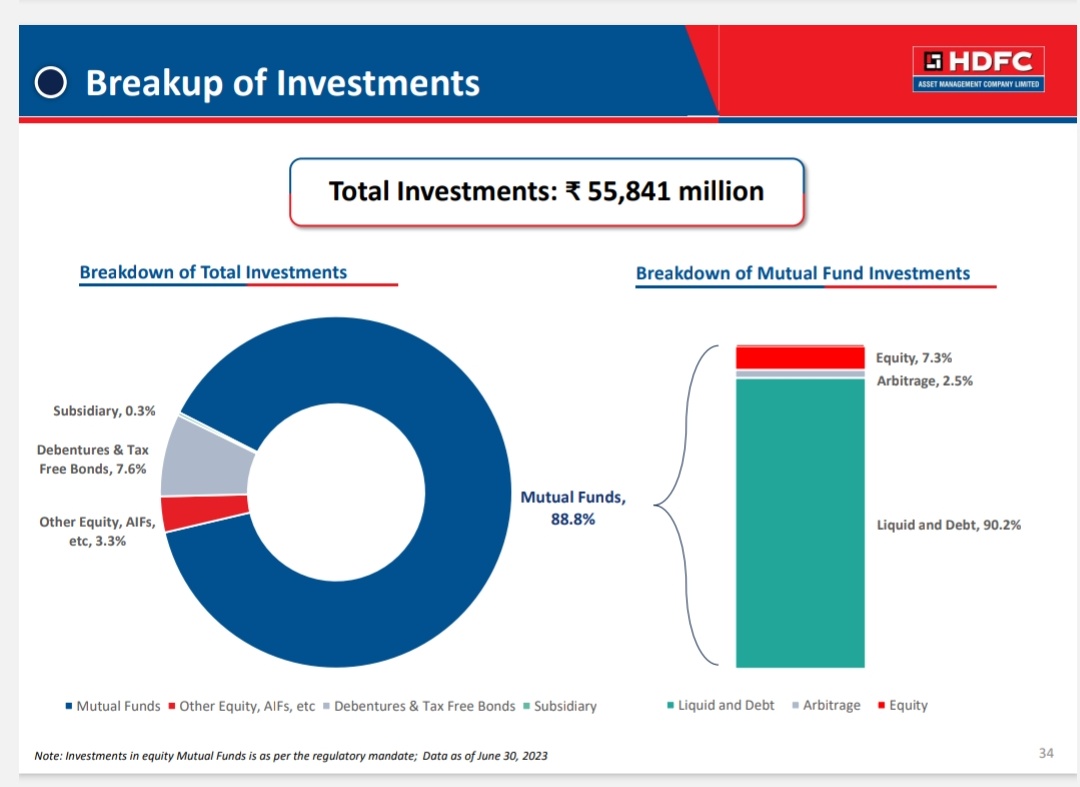

HDFC AMC have roughly 5500CR cash on balance sheet which they have invested in equity,debt as well as FD.So every quarter they adjust it to MTM and report profit or loss on investments in other income.

Here is a snapshot of current investments as per Q1 presentation.

Jio financial services planning to start AMC business in partnership with BlackRock.

Can they disrupt AMC and every other financial services business like they way they did with mobile services? One possible action from their side could be to keep the TER low to grow AUM and be ok with lower profitability for few years.

With big companies like Bajaj & Reliance entering the mutual fund business, competition will only get tougher and possibly lower profitability for all companies? And it’s not just the competition but even SEBI wants TERs to come down

So, wondering how the future would look for HDFC AMC which is already struggling for growth (unless until they quickly jump on an acquisition spree with the financial strength of HDFC Bank)

What other services does the AMC provide, apart from the MFs, what other verticals does it have?

I am guessing there must be some migration from vanilla MFs to PMS or AIF or others, so does the competition refers to the services that are provided for the retail, where to some extent there is no difference, but with other services an AMC can bring in its unique expertise.

Not invested.

----------------------------------Removed the chaff and left the wheat-------------------------

HDFC Asset Management Company Limited Q1 FY’24 Earnings Conference Call” July 24, 2023

**systematic transaction flows has seen a healthy growth. In terms of incremental share in new folios - net new addition of new PAN, we have got a very high market share. Market share on equity across all channels, we have been seeing our market share improving.

** When we are referring to margins, it is predominantly about our equity-oriented AUM. We have mentioned it in the past and continue to say that our book margin is higher than flow margin and would lead to margin dilution with every new rupee flowing in. The impact does get further magnified when the existing low-cost AUM moves out. This is structural. Of course, the pace of dilution has slowed down meaningfully, which I mentioned earlier, due to rationalization of brokerages that has happened in market. Secondly, the TER formula does clearly entail fall in TER with increase in AUM. To make it easier to understand I have pulled-out data for our schemes in terms of AUM and the TER, the TER is regular plan TER and is completed based on SEBI’s formula. So, this is gross TER number, so no impact from distribution costs, etc. So, say, if I take HDFC Balanced Advantage Fund, for example, the AUM was approximately Rs 52,000 crores, and the TER as on 31st March was 1.5%. The AUM moved to over Rs 57,000 crores, which is a combination of mark-to-market gain as well as the fresh flows as on 30th June and the TER fell to 1.47%. So, 3 basis points fall on entire AUM due to change in the AUM. And this fall is what, if you remember, even SEBI’s Chairperson referred to in our last Board meeting interview, that the economies of scale are being passed out to investors. As we saw a rapid increase in the AUM during the quarter, the same is the case with a couple of our other larger schemes too. So that’s just to explain the impact of rise in AUM and consequent impact on the TER and the second was on the flow side. I mean, the newer flows are coming at a lower margin than the margin that we have on the book. But let me make this point very clearly that from our perspective, think about it. The example that I gave a Balanced Advantage Fund, Rs 57,000-odd crores into 1.47% gives us higher revenue as compared to Rs 52,000-odd crores at 1.5%. So clearly, I mean, a higher AUM while will lead to a margin dilution given the formula, but for us, it’s higher absolute profit. Now I’m sure somebody may ask a follow-up question then why don’t you cut the commission on the book every time this happens. So easier said than done. Also, market movement of 5%, 10% can make this swing one way or other and is not practical.

** on the merger, we have a very optimistic view of this opportunity. As you know, bank is a formidable distribution machine, and we will put in enough and more effort to capitalize on it. We already are deeply involved with them across all levels, but alignment of interest can definitely be a big tailwind for us. We are seeing material improvement in the engagement, and we’ll continue to work on strengthening it further.

**There is one NFO which we’ll have now is the transportation and logistics fund. But from an incremental product range, I think we are more or less full on the product side when it comes to equity as well as fixed income. On the passive side, where we have done lots of products over the last 2 years, idea would be to grow all of those products over a period of time.

Other income, there was a component of MTM. So, is it possible to quantify that?

**Rs 158 crores other income, is largely all MTM, it’s a function between equity and debt. Since the skin in the game circular has come into play, we have a sizable amount of our investments in equity mutual funds, and they have given returns in line with the market and based on our fund returns and the debt is largely as we explained due to the interest rate movement. This part of other income is totally market linked. I mean whatever the market will perform on the equity side, the equity funds will perform accordingly. And the debt investments in mutual funds will go in lines in with interest rate movement.

**bank deposits are Rs 180 lakh crores and when we compare that with mutual fund debt plus liquid AUM, it would be around Rs 15 lakh crores. But as an industry, what we have done on the equity side, if we do something similar on the fixed income side, and we’re just talking about the inherent benefits of debt mutual fund as an investing vehicle, there is a lot of scope for us to grow in that space as well. And particularly for us, in HDFC, given our brand and pedigree, there is a bigger opportunity for us as and when that segment starts growing faster. Madhukar Ladha: Thank you, sir for the answers. And all the best.

Your ability to gather assets in the market in terms of the strong fund performance. Whether based on your expectations, maybe four quarters, six quarters back, whether the incremental flow market share is spanning out as per expectations?

** it’s improved substantially relative to where we were. Of course, we always want a higher and higher share. Also, the percentage of new investors that we have been able to garner in this quarter, the percentage of new volumes that have got created in the industry, the share in systematic transactions, all of that are like very heartening to us. For us, our partners are very, very important. They bring like on more than 3/4 of our business. They are our face to the investors, and we ensure that, they make good margins at the same time we ensure that, we have a very healthy margin on every rupee that we gather. there is not a direct correlation between paying higher brokerages and getting higher market share. So, one of our larger funds, where we pay the least possible brokerage is seeing healthiest of the flows.

Lot of new players …any changes on the ground that you’re seeing in terms of competitive intent?

** At any point in time, there have been many competitors. the total addressable market is substantially higher. It’s a very beautiful business from a long-term profitability perspective. So, this will invite a lot of players. Having said that, I think that the way we have built in terms of our people, our processes, our product range, our presence, both physical as well as digital, the partnerships that we have built, the platform that we have built and on top of that, if I can add two more, the passion with which we are working and the deep sense of purpose that we have put for ourselves to be the wealth creator for every Indian, we believe, we will continue to do well.

In spite of the AUM growing the revenue of the AMCs have stagnated. The increase in AUM is not trickling into the bottom line. All of the AMCs have great ROEs. This is attracting huge investments, leading to patient money back newcomers. To top it, we have a regulator who has taken a tough stance on the expense ratio. The influx of all the new players will keep a tight lid on the margins and growth of the incumbents. Which is eerily reminiscent of the classic capital cycle that has played out in all industries. The industry as a whole will grow, the end customers will benefit the companies will fight to protect their market share and hence the shareholders of the companies will make little.

Yes, this seems to be the case. AUM growth may not translate much into PAT growth due to regulatory norms to reduce Expense ratios, Investors moving to Index Funds and many such reasons.

Also, I personally believe that, for various reasons (mostly known to all), Indian GDP and Per Capita GDP is not actually growing as per its true potential. With such a large population of earners in the age group of 25 to 40 years, Growth in people’s real income seems to be negligible.

Focus on improving productivity of large population, good and fast transportation facilities, transparent governance are those areas which need to improve so that, productivity of population can improve translating into much more growth in GDP and also Per Capita GDP. This area seems to be often neglected which is an essential ingredient to lift the income of people which can increase Saving rate (which is currently at the lowest in past 3 decades).

Once the Saving rate is increased, there is potential to see high rise in AUM growth much above current 10% to 12% low to moderate growth in Equity AUM.

Disc : Invested in HDFC AMC with moderate expectations.

I may be wrong in my analysis.

With new big companies entering the field (Bajaj, Reliance etc), consolidation will have to happen. HDFC should make a plan for inorganic growth

I always have this thought that why one should invest in AMCs when we have listed players like CAMS, KFinTech which are catering to the entire MF industry. Investing in individual AMC will have its ups and downs based on the AMCs performance and product mix where as RTAs like CAMS and Kfintech does not have that risk other than the cyclicality of the markets.

Would appreciate views of senior members like @Chandragupta @zygo23554 @Dev_S @akacker to understand pros and cons of both these business models.

Went through the entire thread but could not find the comparison hence the query.

Invested in CAMS and HDFC AMC.

I guess, if market does not perform, there will not be much interest to participate from the retail via MF route, as they have number of other options to put their money in. And if there is not much of retail participation, whose participation forms the majority of AUM for an AMC, the vertical which caters to these AMCs listed or not, will come down for RTAs too. All these entities are participating in the same ground with a major portion of their revenues intertwined, excluding the verticals which are independent and exclusive to one company.

So my limited view is that, market should grow, the interest/incentive to put money should continue, the wheel should not slow down, then maybe yes I guess RTAs may yield more than AMCs, more so when the differential is diminishing between one AMC and other, unless there comes a Quant, which may or may not continue its outperformance.

Just my thoughts, not invested in any AMC, had a position in CAMS before.