A 50% equity dilution for raising working capital is not a good idea but given their current situation there wouldn’t have been other options. Although I m a bit nervous with this new supply of shares, I m of the opinion that all the negatives have been factored into price. They plan to reduce debt from their dues from the Govt. which is the key development to watch going forward.

This could have been a good turnaround story, but HCC’s struggles with arbitration claims and dealing with this government’s penchant for constantly changing the rules of the game, appear to be never-ending. https://www.bloombergquint.com/law-and-policy/arbitration-act-supreme-court-to-decide-whether-automatic-stays-can-be-retrospective

With these kind of arbitrary(!) amendments - refer the article above, fat chance of an infrastructure revival.

1 Like

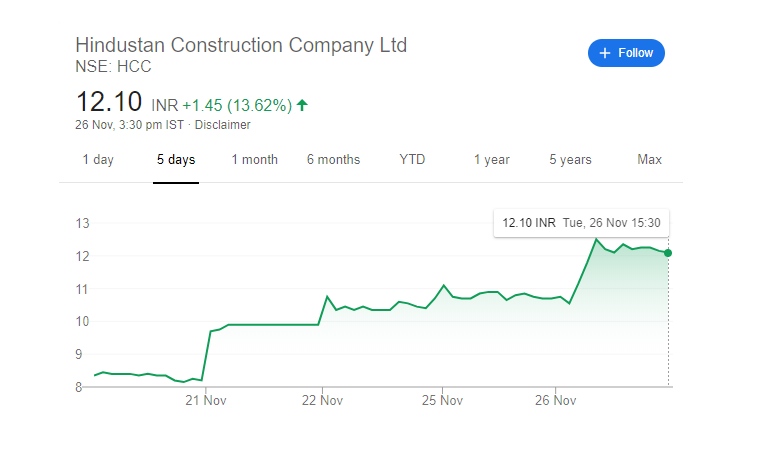

This 50% jump in last 4-5 days is predominantly due to Cabinet approval initiatives to revive the Construction Sector, which was done on 20 NOV 2019

1 Like

looks so,lavasa city and NCP go long back.

1 Like

The company has reduced debt considerably and has an order backlog of Rs 16,632 Cr in Q2 FY22

Key Highlights: Q2 FY22

- Consolidated Group revenue at Rs 2,848.2 Cr in Q2 FY22 vs Rs 1,831.1 Cr in Q2 FY21

- Consolidated Net Profit at Rs 139.2 Cr in Q2 FY22 vs Loss of Rs 476.6 Cr in Q2 FY21

- Standalone E&C revenue: Rs 984.6 Cr in Q2 FY22 vs. Rs 466.2 Cr in Q2 FY21

- EBITDA margin (excluding Other Income): 4.8% in Q2 FY22 vs. 8.3% in Q2 FY21

- Standalone Net Loss of Rs 159.3 Cr in Q2 FY22 vs Net Loss of Rs 169.7 Cr in Q2 FY21

- Sustained operations momentum with easing of lockdowns on progressive vaccination coverage

- COVID restrictions delayed Arbitration hearings and award publishing, which otherwise should

have given a much higher contribution to the turnover in Q2, but got deferred - Abnormal rise in prices of construction materials during last 12 months (steel ~36%, cement

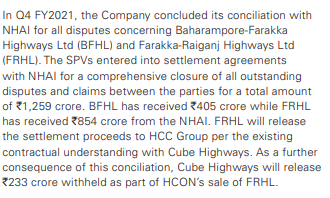

~23%) posed a challenge - HCC and HCC Concessions received monies from NH34 BOT conciliations. HCC Concessions

received amount held back by Cube Highways - Debt carve-out resolution plan with lenders is in final stages of implementation

(Source: From their investor presentation HCC_InvestorPresentation.pdf (1.1 MB)

)

To avoid litigations, the GOI in the Union Budget has proposed

a conciliation mechanism for resolving disputes in the

construction industry. Para 135 of Budget provides as under:

135. To have ease of doing business for those who deal with

Government or CPSEs and carry out Contracts, I propose

to set up a Conciliation Mechanism and mandate its use

for quick resolution of Contractual disputes. This will instil

confidence in private sector investors and contractors.

This mechanism is likely to spur private investment in the

Infrastructure sector, which is greatly problematic due to

mechanical challenging of awards and long delays in dispute

resolution. The above mechanism-specific mandate to the

CPSEs will go a long way in helping the contractors and the

government agencies to ensure the infrastructure projects

are completed with minimum delays as the disputes would

be settled and the money would be available during the

performance of the Contracts.

(Source: Annual Report 2021:HCC2021.pdf (3.9 MB))

This makes it easier for the company to receive its past dues . IMHO I think the turnaround for this company is taking place now only, they have bagged new orders like HCC_ChennaiMetro_OrderWin.pdf (349.8 KB) .

The stock price has been trading in the 5-10 rupee range for around two years and I think the negatives have been priced in . The management also seems to be walking the talk by completing sale of assets and reducing debt. India has developed US$ 1.5 trillion

(111 lakh crore) National Infrastructure Pipeline (NIP) built on Infrastructure Vision 2025. The total project capital expenditure in infrastructure sectors in India during the fiscals 2020 to 2025 is projected at over `111 lakh crore in which sectors such as Energy (24%), Roads (19%), Urban infrastructure(16%), Railways (13%) and Ports amount to around 70% of the

projected capital expenditure. HCC has executed major projects in the past and are capable of doing so going forward.

(Disc: Positively biased and invested)

Anyone else tracking the stock please share your views.

HCC India featured in Construction Worlds Web Series

Small interview of Ajit Gulabchand

Hindustan_Construction_Company_vs_National_Highways_Authority_Of_on_22_November_2021 (1).PDF (201.4 KB)------>

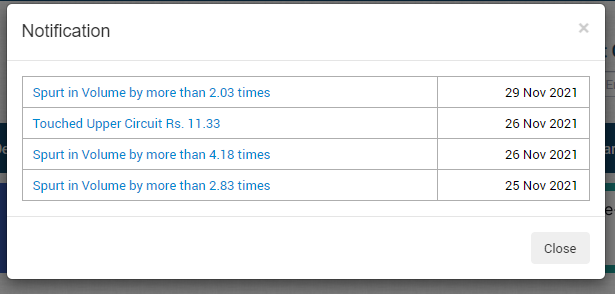

The company has received some arbitral award from NHAI on Nov 22.

BSE notifications that week

referring this order ----->Hindustan_Construction_Co_Ltd_vs_National_Highways_Authority_Of_on_16_March_2021.PDF (202.9 KB) I think the awarded amount is 100crores

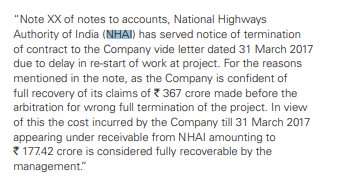

.From annual report

Does anyone know which amount is received by HCC , ( whether 1259crore or the 177.42 crore)

(Disc: Same as above)

More people are starting to notice the company , maybe there’s a chance for rerating

India will hv 9 new operational nuclear reactors by 2024. In addition, 12 new reactors hv been approved during pandemic to generate 9,000 MW once complete, taking the country’s nuclear power capacity to 22,480 MW by 2031 that is at 6,780 MW currently.

HCC Biggest beneficiary…

1 Like

This article is from 2015 , but we can get an idea of which companies are top in their segment of operation . Only HCC and L&T are present from the construction side .

2 Likes

HCC: (Zee Business Exclusive). The creditors have chosen the Darwin Group’s bid for the former Hindustan Construction Company (HCC) controlled Lavasa township and are likely to vote on the bid soon. Sources aware of the development exclusively informed Zee Business that the creditors in lieu of dues worth Rs 8,836 crore have opted for a plan of Rs 1,814 crore. Rs 1,466 crore, out of Rs 1,814 crore is the resolution amount. Banks will get Rs 929 crore out of Rs 1466 crore while Rs 250 crore will be invested to complete the project and Rs 440 crore has been fixed for settlement of claims of the home buyers. An amount of Rs 679 crore will be converted into a 6% Rupee term loan and Rs 250 crore has been fixed for secured NCD redemption

2 Likes

The stock might get further rerated if the company gets contracts for nuclear plant construction .

1 Like

HCCinvestorpresQ3.pdf (549.9 KB)

Standalone profit increased to 28cr

HCC financials do not look good at a glance. In fact, there is a great divergence between its long financials and the price movement:

Compounded Profit Growth

10 Years: 11%

5 Years: 19%

3 Years: -13%

TTM: -116%

The movement:

As our friend @capsule91 has stated, it is a turnaround story. The company has been winning orders recently.

It has won one largish order yesterday/

A joint venture between Megha Engineering and Infrastructures Limited and Hindustan Construction Company has emerged as the lowest bidder to build the Bandra Kurla Complex station of the Mumbai-Ahmedabad bullet train project, a NHSRCL spokesperson said on Wednesday (That would be 28th December, 2022).Bullet train project: Megha Engg-HCC lowest bidder for BKC station contract | Mumbai news - Hindustan Times

Themetrorailguy.com, a website that tracks infrastructure projects in the country, said on Wednesday that MEIL-HCC had emerged as the lowest bidder with a bid of ₹3,681 crore. It beat giants like L&T and JKumar Infra.

Please add if you find any new favourable or adverse factors.

Disclosure: Invested a small sum today.

Edited: Found the DLOF on HCC’s website. Link below.

HCC Rights Issue announcement - https://www.bseindia.com/xml-data/corpfiling/AttachLive/cbe2bcba-361b-4d4c-ae79-c4df600f8732.pdf. Says “the Company has filed the draft letter of offer dated December 14, 2023 (“DLOF”) in connection with the Issue with the Securities and Exchange Board of India.”

The DLOF document is here https://www.hccindia.com/public/uploads/annual_return/0_64564600_1702642075_Hindustan_Construction_Company_Limited_-_Draft_Letter_of_Offer.pdf. Rather hard to read, but essentially 213 crores of the estimated 300 crores rights issue will be towards working capital. I guess the promoters will participate. Beyond that, lots of detail (including an industry overview section) that’s probably useful to go through.

HCC’s actual situation and growth prospects has become rather hard for me to assess now. It’s worked out alright over the long-term after I entered at the wrong time, but took the risk of adding a bit (should have added more in hindsight) when it was quite low purely on the hypothesis that technically they are are a strong company - maybe the best after L&T and therefore would sort out their mess somehow. They have cleaned up their balance sheet to a considerable degree, but they haven’t been winning major orders in recent times (partly, due to a conscious decision to focus on debt overhang first). The status of arbitration claims and awards remains unclear. Promoter ownership is quite low, more dilution can possibly be expected even post this rights issue. And finally, it’s highly reliant on government orders. So, policy and government changes risks continue to be high.

@hitesh2710 had recently posted that technically, HCC looked bullish. I am no technical expert, but given his experience and knowledge of technical analysis, probably he is right and it can run up a bit.

I am undecided if I should exit or stay invested.

HCC earnings call recording - https://hccindia.com/uploads/reports/Analyst-Meet-Recording-Q3-FY24.mp3

My short summary

Q3 FY24 Revenues up ~8%, EBITDA margin at 12.4% slightly down, standalone and consolidated PAT up (from standalone losses in FY23). Bids worth 7000 crores submitted, and pipeline of 46000 crores in future bidding (in the next 3-12 months. A good part of it seems to be in hydro and pump storage, but medium term expect to more in the transportation segment - railways, tunnels etc. with the odd hydro project. Nothing mentioned about nuclear except that they were clear they won’t focus on nuclear projects opportunities outside India). Mumbai Coastal Road - first large-scale monopile project in India.

Money from Steiner AG sale (partly used to fund Steiner - seemed vague, partly to return capital to HCC for growth, not for debt). One can potentially expect to see either exit or dilution of Steiner AG development business too in the next few quarters (my inference from the answer to one of the questions). Larger fund raising planned in a couple of quarters - to support growth and strengthen balance sheet with more liquidity (rights issue, expecting approval soon).

Current execution run rate of about Rs.1200 crores per quarter. Looking for average size of projects only around 1000-1500 crores, with some projects of over Rs 2000-3000 crores. Lumpiness expected because of fewer projects that are more material in size.

Debt - OCDs outstanding of Rs.2000 crores (annual repayment on or before 31st March each year, i.e. bullet payments; repayment of 340 crores this March which will reduce debt further. Net debt reduction by about 100 crores in FY24). Weighted avg interest rate of 11% on debt. Interest cost going forward expected to be around Rs.400-450 crores in FY25 (reduced by half from past - not sure if it’s FY23 or FY24). Will focus on refinancing debt after building order backlog and cash flow improves. Will try to prepay debt as arbitration awards come in. Arbitration awards - for 4-5 awards, trying to settle via Vivaad se Vishwaas scheme, but for bulk of awards, not opting for it as it’s financially unattractive.

Land parcels worth 50 acres (Navi mumbai, Thane, Mumbai etc.) - indicated they will disclose more details next time.

I think it will be interesting to see how much of that 46000 crore in pipeline translates into wins. They haven’t won anything in 6 months (also because they have bid very little), but these projects are in their areas of strength, so a good win rate here is important.

Question - Can anyone share some perspective on how rights issue tend to get priced? I mean it will be at a good discount for sure, but I don’t know much about how the pricing is arrived at. Would love to understand better.

Disclosure: I trimmed ~20% of my position last month. I am optimistic about the company but with the upcoming dilution, uncertainty of order wins, possibility of having to raise debt again (never know what can go wrong), and heavy reliance on government projects, it is still a risky investment proposition.

5 Likes

Rights issue price at ₹21 per equity share, which is a discount of 35-40% of CMP.

Russian Nuclear Agency Chief announces to supply next generation nucIear fueI to India.

Key HISTORIC announcement by Russian Nuclear Agency Chief –

-

Serial construction of Russian-designed high-capacity nuclear power units at a new site in India.

-

Implementation of land-based and floating low-power generation projects

-

Cooperation in the nuclear fuel cycle area, as well as in the field of non-power applications of nuclear technology.

HCC is giant in Nuclear power sector.

1 Like