HBL POWER SYSTEMS STOCK STORY

ELEVATOR PITCH

-

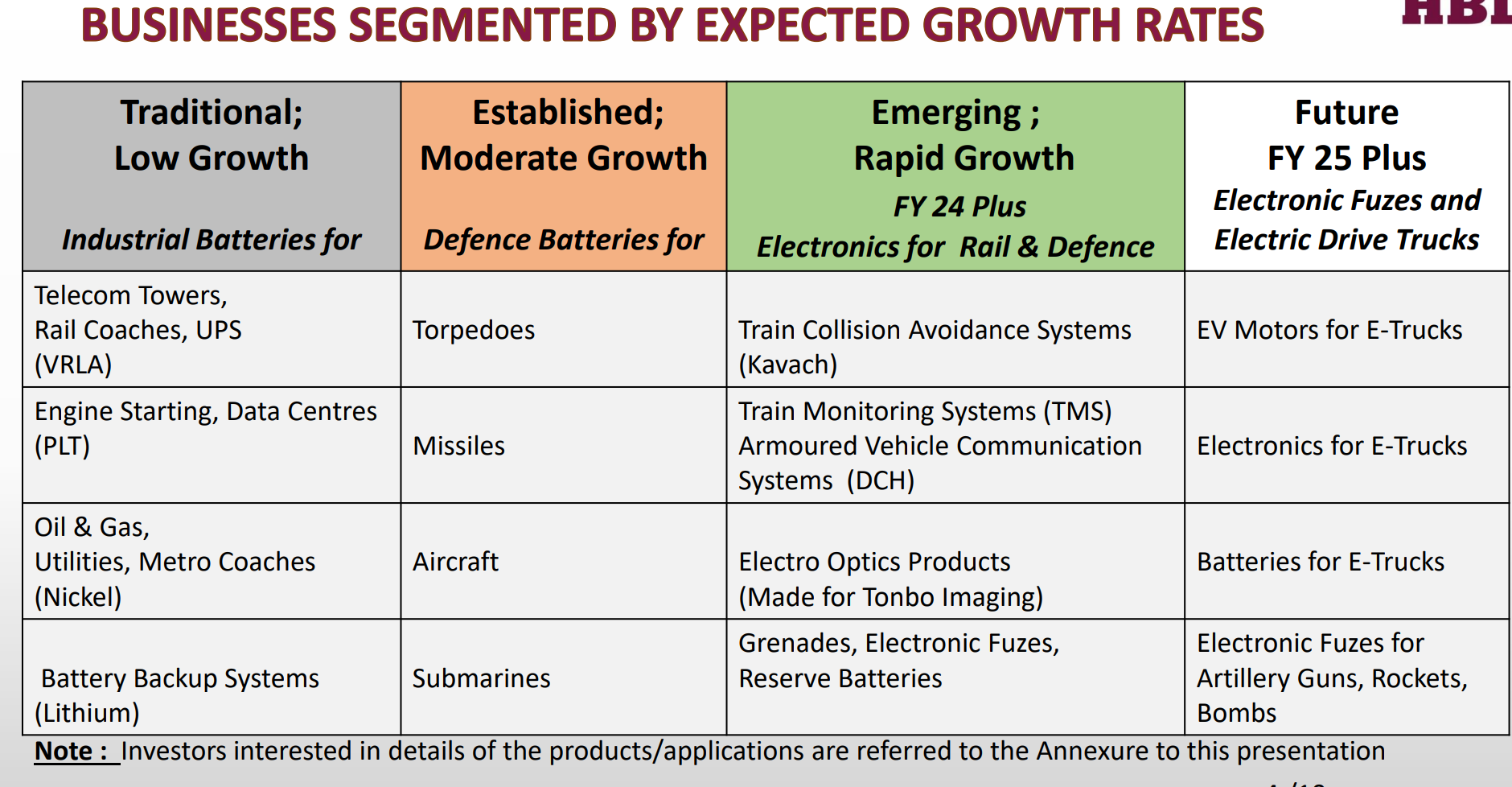

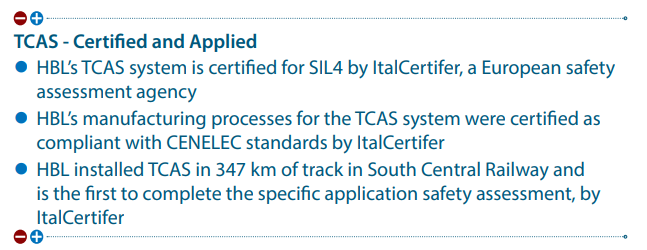

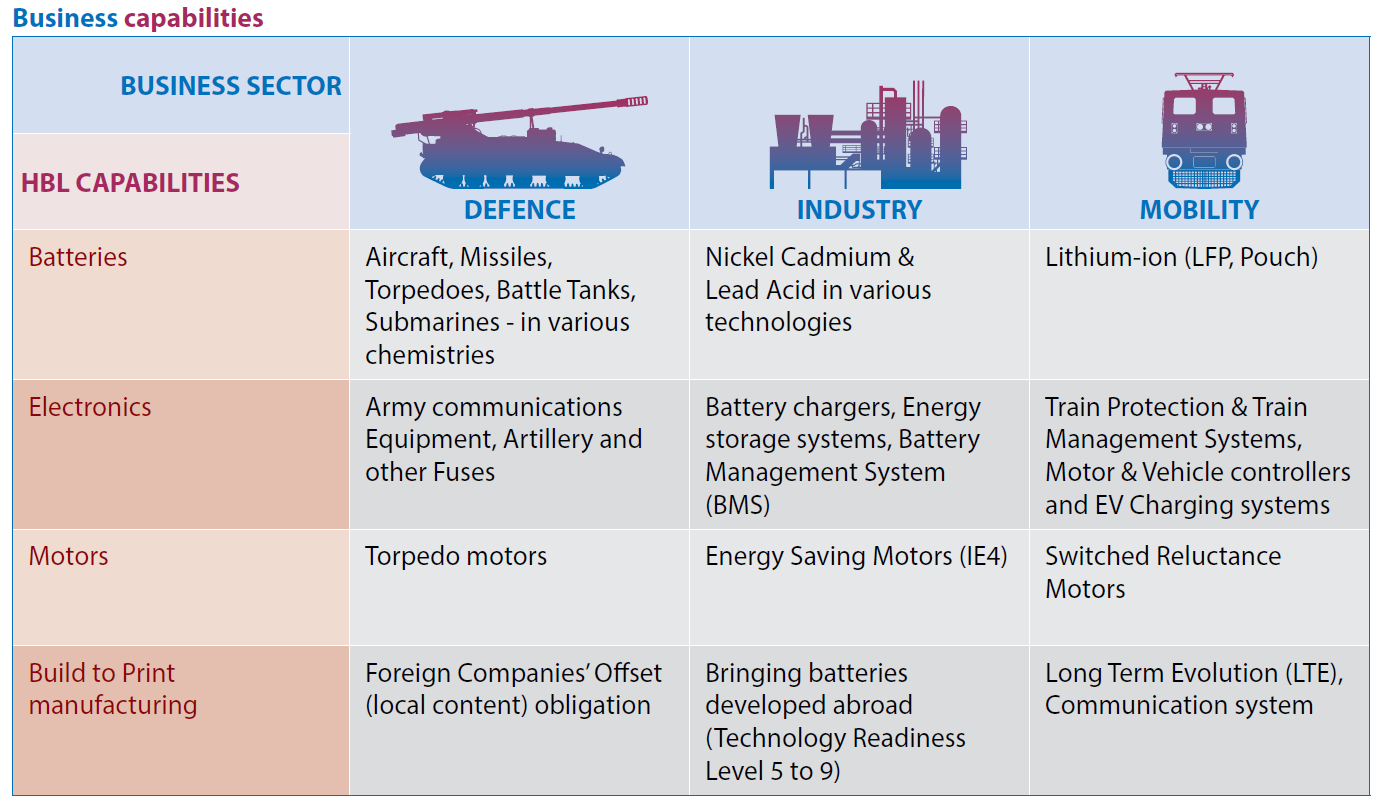

Focus on technology solutions: HBL specializes in identifying technology gaps and developing technology solutions inhouse through internationally benchmarked niche products in the railways, batteries and defence space. Viz (a) HBL is the only Indian player to have developed PLT battery, (b) One of the three companies to have developed an internationally certified TCAS system indigenously, (c) HBL is the only Indian company to have developed TMS system, (d) HBL is the world’s 2nd largest manufacturer of nickel cadmium batteries etc.

-

Game changer for HBL - The Indian Railways Opportunity

- HBL Power has been approved as a vendor by Indian Railways for Kavach (TCAS- Train Collision Avoidance System) along with 2 other companies. Any new vendor will take atleast 2-3+ years to get approved, thereby limiting competition.

- This is a very large opportunity - Expected to be deployed across 35,000 Rkms ‘route kilometer) and thus potentially a c. 15,000-20,000 crs+ opportunity over next 4-5 years.

Of this, tenders for c. Rs 2000 crs have been awarded this year (HBL received orders worth c. Rs 600 crs executable over 18-24 months) and potentially c. 1000-1200 crs is expected in FY 24 (more details later in the note). - This business has a high technology component and expected to have high EBITDA margins (c. 25%) also reaffirmed in FY 22 AGM of Kernex Microsystems.

- To summarise – A large opportunity in a specialized technology intensive product in an oligopolistic set up with visibility of no more competition at-least for 2-3 years.

- This product alone has the potential to more than double HBL’s EBITDA by FY 25 from FY 22 levels.

- Similarly, HBL has developed Train Management System in the Railways space, which is potentially a c. Rs 2000 crs opportunity over next 3-5 years with high EBITDA margins (due to HBL’s lower cost compared to competition – which are largely MNCs). Tender flow from Railways needs to be watched in this space.

-

Huge Industry Tailwinds

- HBL has been working on products in defence and railways space for 20+ years without any large-scale commercial success (ability to sustain R&D for such long period of time without commercialization is not common).

- However, they finally seem to be at the inflection point where they can benefit from the huge industry tailwinds –

- large capex in Railways space and

- huge thrust on Atma Nirbhar / indigenization in defence space.

Important thing to note is that profitability numbers have significantly improved over last 3+ years (from 7-8% earlier to 12% now) on the back of improvement in battery margins - without any meaningful contribution from railways or defence yet. The boost from industry tailwinds will reflect in their numbers in 2-3 years from now.

-

Steep Value Migration Curve - Notable product mix changes expected in the business in next 3 years viz

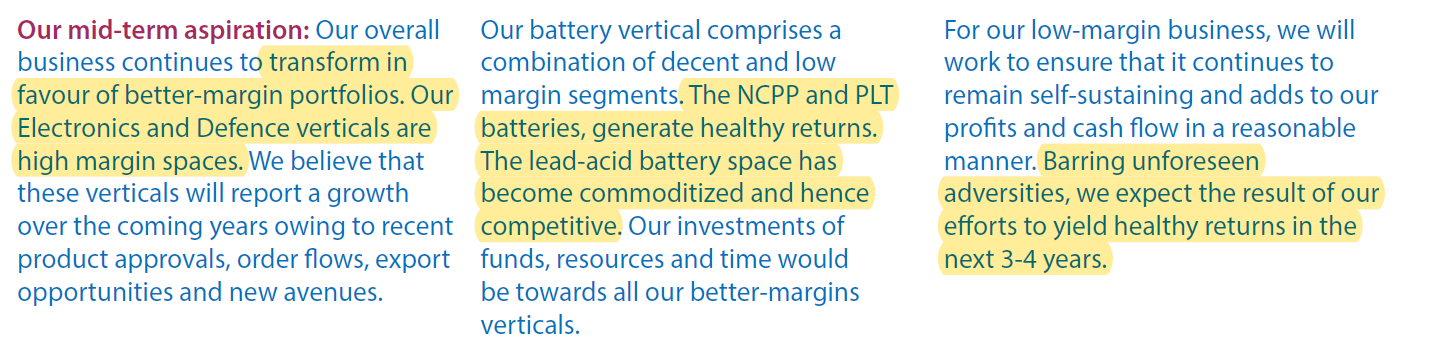

- Railway electronics to command much higher share than batteries which is a much higher margin business (c. 25% plus margins vs c. 12% in Batteries)

- Within batteries segment - Share of commoditized telecom lead acid batteries to decline and share of specialized batteries like PLT batteries, defence batteries to increase - resulting in overall higher margins. Also evident in segment margins over last 2-3 years wherein battery segment has reported improvement in margins from c. 8-10% earlier to c. 12-15% now.

- Defence business - Products like electronic artillery fuses, grenade fuses etc with large opportunity size (c. Rs 6000 crs over 10 years) and high margins to contribute to profitability on back of indigenization push by GoI in the defence sector.

-

Cash Flow and RoCE driven growth

Significant increase in profits driven by increase in topline and increase in overall profitability margins from c.8-11% range to c.16-20% range - Without any major incremental investment in Fixed assets (Batteries/Railways do not require any major incremental capex; only working capital will be required) - Will alter the RoCE profile of the Company considerably (from c. 10%-13% to c. 20%). Caveat - they do not falter on the execution -

Huge Optionality in the business going forward (all very high-margin segments)

- Artillery Fuses - 6000 -10000 Cr market spread over 10 years (one of only 3 players +2 PSUs)

- TMS - 3000 Cr market spread over 10 years (one of only 2 players)

- Electro Optics/Tonbo 5000 Cr market (one of only 2 players?) Upto 150 Cr Equity+Manufacturing Investment; Very large domestic opportunity Slide 29 HFCL Investor ppt

- Artillery Fuse Export Segment - Unquantified - (exclusive (?) in partnership with Ordnance Factory)

-

All Optionalities are Sunk-in Costs - What sets apart HBL’s Business Model uniquely (though historical, and perhaps incidental) from most other high-technology niche businesses is that major major investments in R&D/Product Development are already sunk investments. Order-Flow from Optionalities when they start coming in, will create big Operating Leverage and flow straight to the bottom line

CURRENT MARKET/INDUSTRY TRENDS

-

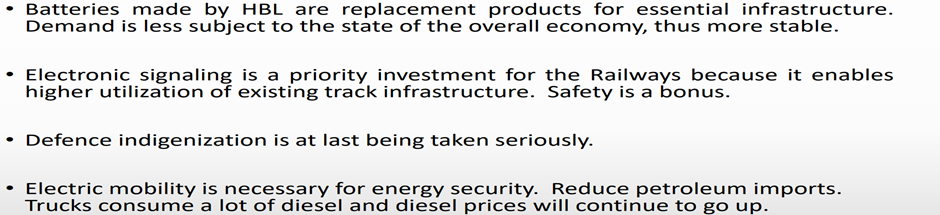

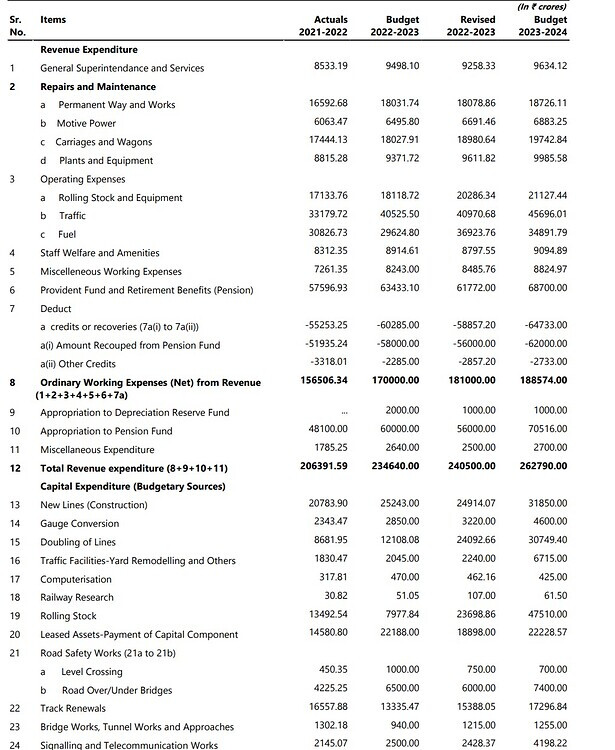

Railways Capex - Highest ever Capex plans of Indian Railways c. Rs 2.45T for FY 23 - with focus on 400 new Vande Bharat trains, 3 new ICF (Integral Coach Factory) besides the Chennai one at Latur, Sonepat, and Rae Bareily, Freight Corridors, TCAS, electrification, station redevelopment etc. Tenders for TCAS c. Rs 2000 Cr rolled out in FY 23. Potentially c. Rs 3500 Cr (5000kms) order possible in FY 24. Source: Ref Budget documents (line 24)

Also reaffirmed by Railway Minister Ashwini Vaishnaw wherein he mentioned Kavach alloation for 5000 kms in FY24 compared to 3000 kms in FY 23.

-

Higher worldwide focus on Defence sector in general given Ukraine-Russia conflict and realisation that countries need to be self-reliant in defence

-

Significant impetus from the Government on Make in India in Defence Sector and higher participation of private sector in Defence (which was not the case earlier). Interesting insights on the industry in this video How is India’s Defence Sector becoming Atmanirbhar | Amisha Vora, PL Group and JD Patil, L&T - YouTube

-

Atmanirbhar in Defence - Significant changes in defence procurement strategy with focus on IDDM - Indigenously designed, developed and manufactured - Release of positive indigenisation list by the government to be addressed over next 1-5 years - The Defence Ministry estimates potential contracts worth ~Rs. 4 lakh Cr (US$ 57.2 billion) for the domestic industry in the next 5-7 years (2025-2027).

BARRIERS TO ENTRY

-

Technologically advanced product segments requiring significant R&D work - HBL mostly prefers to operate in technologically advanced product segments which require considerable investments in R&D in product development.

(a) Eg. TCAS has been in development over 10+ years and has only 3 approved vendors as on date. Future competition will also be limited as only 2 other companies are working on the product development currently, and these 2 companies are also likely to take 2-3 years for product development, field trial etc. Also important to note that the new players need to be interoperable with the current suppliers which will make the development process more time consuming.

(b) Even in TMS space, HBL is one of the two Indian approved vendors in the space (other than MNCs).

(c) HBL is the only company making PLT batteries in India. Enersys is only other global competitor with more than $1bn sales.

(d) Defence - HBL supplies batteries for most missiles made in India. Even Artillery fuses has only 5 competitors - 3 private players and 2 PSUs.

Most of these products have been 5-10 years in making and this is the biggest entry barrier here. -

HBL over last 10 years has spent c. Rs 300 crs in R&D across various products in railway electronics, defence, batteries - This R&D expense provides them a big competitive advantage as it is not easily replicable by anyone else.

-

Also, important to note that most of the R&D expense was routed through P&L (Profit and Loss Account, and not capitalised) which speaks of their corporate governance and also explains their low margins historically.

-

Long gestation period: Most products require a long field trial period (given criticality in terms of usage viz TCAS critical for passenger safety, defence products safety/reliability, etc.). This implies a longer lead time for any competition which wants to come in - for product development, field trials, etc.

-

Establishing customer relationships in some of the products is a long drawn one viz PLT batteries, Aircraft batteries, Defence batteries, Railways etc.

BUSINESS MODEL

-

Niche High-Tech Import Substitutes - Customised high end technology products built to address specific gaps in technology within the country - which were largely being imported from MNCs earlier

-

Huge Entry Barriers - Most HBL product offerings in Railways/Defence segments have erected huge (insurmountable (?) entry barriers, likely to sustain first-mover advantage in a decade-plus India “Atmanirbhar-tagged” opportunity

-

Significant Cost-Advantage to MNC Offerings - HBL products enjoy significant cost advantage vs MNC offerings. HBL operations historically though have been Inventory-heavy (~150-190 days), leaving good scope for future improvements, especially as the product mix changes decisively to Defence/Railways Electronics being the major segments in next 3-4 years

-

Gross Margin Improvements - Steady Gross Margin levels (~38-40%) over the last few years as the company started executing better shows ability to withstand/pass-on RM volatility risks on existing segments. Gross Margins are way higher in new segments like Defence/Railways Electronics and will shore up inherent business model strength

-

2x EBITDA Levels in 2-3 years - Above Product Mix changes from low margin competitive products to high margin niche products in Defence/Railways Electronics, and higher margin batteries –could result in EBITDA levels almost 2x of current levels

-

Conducive “Atmanirbhar” Business Environment - Business growth in B2G Defence/Railway segments will always be dependent upon changes in Government Policy, Tendering, Rollout, and other external factors; subject to possible deferment/delays. Must be mentioned though that the current environment is very conducive for businesses with High-Technology/Import Substitute businesses like HBL

-

Enhanced Future Cash Flows - Medium Term/Foreseeable product mix with low incremental fixed asset intensity, coupled with higher margins - points to considerably enhanced future cash flows

-

Tomorrow’s “Cash Cows” from already seeded new revenue streams - Most of the Optionalities referred above, demonstrate the potential to mature quickly and Individually deliver “cornered profits” similar to current profitability ~100 Cr annually, when matured

INTERESTING VIEWPOINTS

-

In the National Budget of 2020-21, the Government allocated 7,500 Crore for installing TCAS over 25,000 route kms (out of a total railway network of 67,956 kms) in 16 zonal railways. [1]. For many years, TCAS was competing with European solutions like ETCS L1 and L2. FY21 saw this competition being put to an end, with the discovery of total cost of ownership and overall value proposition of TCAS as superior. It was named as the National ATP system for India (Kavach).

-

The FY21 National Budget provided an allocation of Rs 3,450 Crore towards installation of TMS and CTC in 1,646 stations (out of total 7,349 stations) of the Indian Railways network. [1] Significantly, unlike TCAS (3 RDSO approved Indian Vendors) HBL reportedly is the first Indian company approved as vendor for Indian Railways for TMS. Alstom’s ICONIS platform is the other known Integrated Train Management System (TMS) installation in Eastern Dedicated Freight Corridor (EDFC) Operational Control Centre. HBL also has orders from Siemens for TMS installation in Eastern DFCC project (probably in Kanpur-DDU section)

-

TCAS: HBL had received their 1st order for TCAS in FY 20 for 350 kms which they had successfully implemented. Next set of tenders was rolled out this year with HBL receiving orders valued c. 600 crs to be executed over next 18 months.

-

Electronic Interlocking (EI) –

- Indian Railways is planning implementation of Electronic Interlocking c.1550 EIs over next 3 years #

- Indicative cost for EI on average is c. Rs 1Cr/unit thereby being c. Rs 500 Cr/year opportunity at an industry level, on average over next 3 years.

- HBL is ready for field trials of electronic interlocking after successful testing by RDSO (as per AR FY 22).

- Electronic interlocking is a complex system largely dominated by MNCs like Siemens/Alstom/Kyosan and Medha being the only Indian supplier so far. This can potentially be a c. Rs 75-100 Cr/year kind of opportunity for HBL starting H2 FY24, with average c. 15% EBITDA margins.

-

Telecom batteries (Lead Acid) - This segment has seen many years of decline and is now making a comeback due to the improving demand in telecom space fuelled by 5G adoption and higher O&M replacement. Higher volumes in this segment can lead to better absorption of overheads and thereby higher margins from c. 8% to c. 10% – within the existing setup with no incremental investment.

-

Li-ion batteries: HBL absorbed technology from NSTL (Naval Science and Technology Laboratory) for manufacture and supply of Lithium-ion batteries for defence applications [1]. HBL has set up a pilot plant conforming to the requirements of the NSTL to develop Li-ion batteries for various defence applications. Source: 2020 RFI 1; Mar 2022 Vendor Award. Orders worth c. Rs 80 Cr received from NSTL for execution over next 2 years

-

Electric Drive Kit - HBL is working on developing Electric Drive train kits for retrofitting LCVs and buses. One motor and one battery module have received ICAT approval and developments on this front need to be watched. This is a long shot as of today, but if successful can be a pretty large opportunity.

-

Ability to Pass on Raw Material Price Volatility – HBL has exhibited strong ability to pass on increase in raw material prices to its customers viz Gross Margin in last 3 years has been stable between 37-39% (actually increased) despite huge volatility in raw material prices.

-

Well diversified customer segment spread: Revenue mix 3 years from now is expected to be well diversified across the 3 segments – railways, batteries and defence, compared to today. However, dependence on Government business would remain.

-

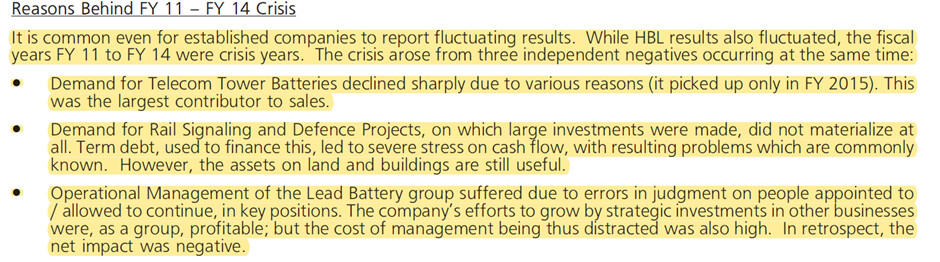

Steep Value-Migration curve – Over the years HBL has reduced the share of commodity telecom batteries (business was in doldrums in FY 11-14 period) and transitioned the business to value added product segments ‘largely within batteries segment so far.

-

Improvement in margins: There has been a significant improvement in margins in batteries segment over past 3 years (despite this being a period with very volatile commodity prices). Margin expansion visibility over next few years is high, especially due to a higher share of revenue from railways and defence (‘the higher margin segments’).

-

Suresh Kalyan, ex Amara Raja Batteries, has been associated with HBL Power Systems since 2014 and is currently COO at HBL, responsible for streamlining operations, bringing efficiencies across assets, operations etc.

-

Significant improvement in Balance Sheet - Reduction in debt from c. Rs 1,000 crs in FY 13 to Nil now, with cash on Balance Sheet c. 180 Crs as of Q2’ FY 23 end. Improvement in RoCE driven by clean-up of operations, focus on higher margin businesses etc.

-

Requisition/Undertaking and Forests Clearance during 2018-2020 for Static Testing Facility: Project is envisaged to cater to needs of Indian Army for proposed Artillery Electronic Fuses, GRAD Rockets, and APFSDS products. Latest activity in Oct 2022 as per the Timeline document above

BULLISH VIEWPOINTS

TCAS/Kavach

-

Kavach - Railways business is Tendered business. Only three Indian companies (HBL/Medha Servo/Kernex) have the technology (certified by RDSO) with significant cost advantage over MNCs as their cost is c. Rs 50-75 lakhs / km vs c. Rs 2 Cr / km cost worldwide.

-

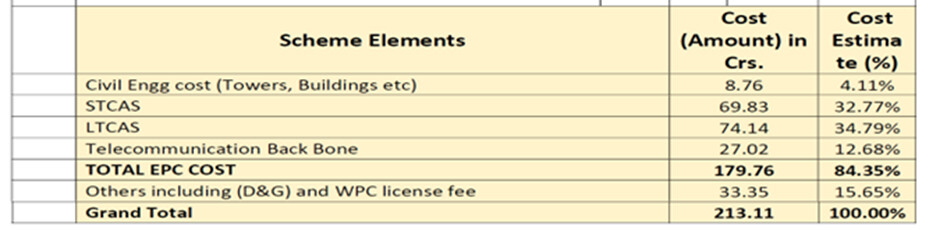

Of the total cost, significant part (70%) is on the technology related part - railways electronics/systems; cost component related to civil cost, license cost, etc. is pretty low

Source: https://ncr.indianrailways.gov.in/uploads/files/1646997292370-Kavach%20A%20new.pdf

- HBL had received their 1st order for TCAS in FY 20 for 350 kms which they had successfully implemented. Next set of tenders was rolled out this year with HBL receiving orders valued c. 600 crs.

Train Management System

- Overall, this is potentially a c. Rs 1,500-2,000 crs opportunity size (c. 3-4 TMS per zone across 16 zones at a cost of Rs 45-60 crs/ TMS) with no other Indian player other than Medha Servo and MNCs.

- This segment has attractive EBITDA margins. But the tenders from Indian Railways needs to be watched out.

PLT Batteries

-

These specialty batteries, specifically designed to deliver high current for a short time-period, are perfectly suited for large Data Centre applications and for DG and Engine Cranking purposes (large vehicles and battle tanks). The Company has been supplying its PLT batteries to Cummins for its DG sets under white label program – an association that has grown each year for over a decade.

-

HBL is only Indian player in the market to have Pure Lead thin plate (PLT) battery. EnerSys is the only other player and global market leader internationally making TPPL (PLT) batteries, and have pointed compelling arguments in favour of PLT vs lithium-ion technology . [2]

-

TCO of Lithium ion batteries is 2.0x+ of PLT batteries and convertibility / usability is easier in PLT compared to Lithium ion (which needs a BMS). Source: [3]

-

HBL’s PLT cost is c. 20-40% lower than that of EnerSys depending upon the application

-

Overall large opportunity size given significant expansion in data centre space in India (Existing c. 500MW, expected to be 3-4x in 4-5 years), and globally. EnerSys has been clocking revenues more than $1Bn, growing at 20% annually

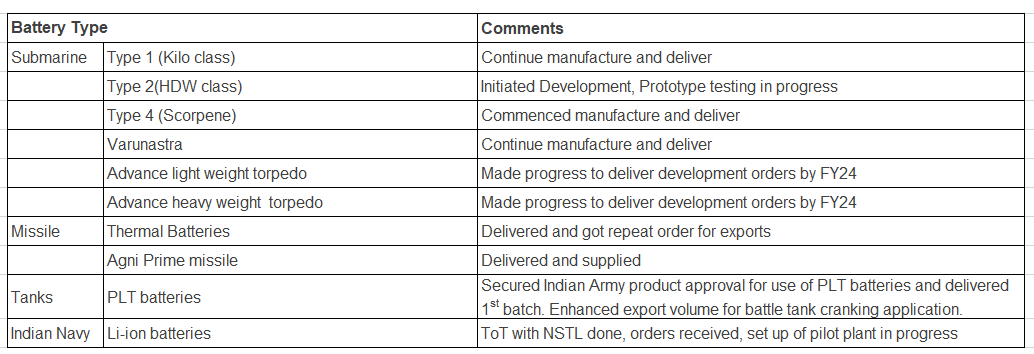

Defence Batteries

Every defence product needs batteries, and HBL has presence across a wide spectrum as below:

• Rest of the battery business is divided across other batteries viz nickel cadmium, silver zinc batteries, other VLRA batteries etc and as a basket overall, can be classified a stable business with marginal growth rates.

Defence Business

• Grenade Fuse

- HBL updated in AGM that they have received approval from Ministry of Home Affairs for fuses for grenades by ARDE and have been given Development cum production partner status. This can potentially be a high margin opportunity and any orders in this space need to be tracked.

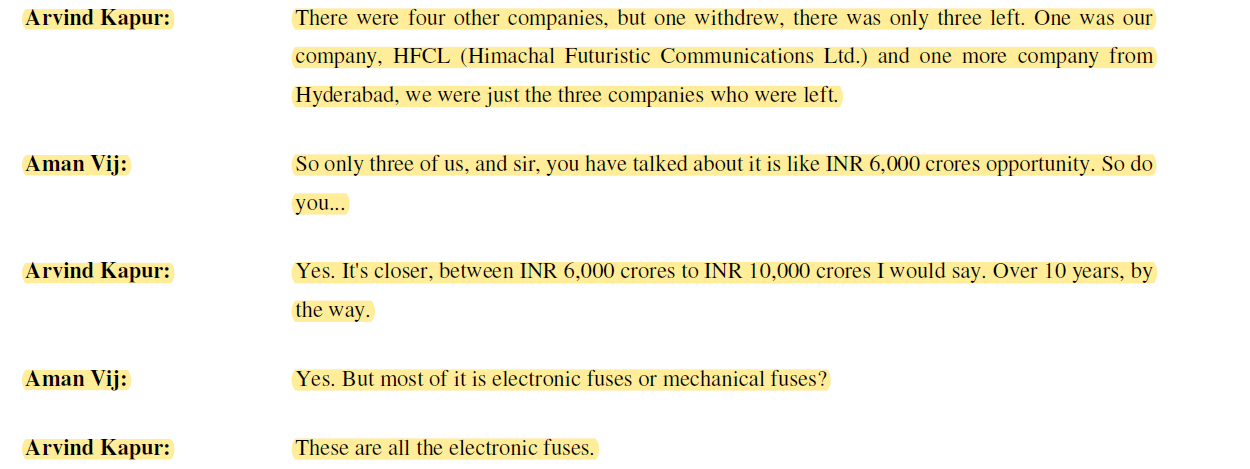

• Artillery Fuse

-

This is a segment with large opportunity size: Rs. 5000-6000 crs over 10 years and limited competition. Refer screenshot below from a competitor.

-

Tenders for artillery fuses had been floated by MoD, product trials were on. Tenders had a requirement for 100% indigenization within 2 years including battery, electronics portion etc. (which will be a disadvantage for PSU cos like BEL, ECIL who were majorly importing c. 60% of components thus far and assembling in India)

-

Limited competition with 3 players in private sector– HFCL, Aan Engineering (subsidiary of Rico Auto) and HBL power, and 2 PSUs.

-

Aan Engineering and HFCL both have a collaboration with a foreign company for R&D/technology while HBL is only one to have developed it indigenously.

-

These tenders have been in works for 3+ years and still not concluded. This remains the biggest risk in the defence space and order inflow in defence needs to be watched out for.

Ref: Q1 and Q2 FY 23 Concall Transcripts of Rico Auto are a good source to understand artillery fuses. -

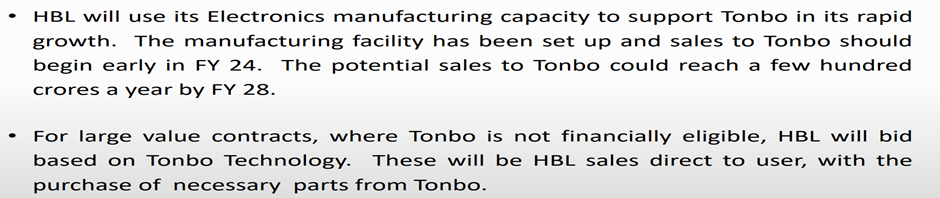

Electro Optics/Tonbo Imaging Investment - HBL has announced an investment of upto 150 Cr in Tonbo Imaging. Tonbo Imaging is an Indian company that indigenously designs and manufactures electrooptics and imaging systems for surveillance, reconnaissance and targeting. The ability to see better at night and over longer ranges to effectively engage targets, is a much needed and sought-after technology. Tonbo is recognized as a supplier of advanced electro-optics systems with field proven deployments in over 25 countries. It is also a supplier to the Indian Ministries of Defence and Home Affairs. Tonbo has multi-million-dollar deal for indigenising Indian missiles.

HBL expects Tonbo tie up to start contributing to topline in FY 24 itself with significant potential to scale up. And for large value orders, where Tonbo itself is not financially eligible, HBL will bid based on Tonbo technology and such orders logically, would have better margins.

BEARISH VIEWPOINTS

-

Slow rollout of Kavach: As of FY 22 end, Kavach had been implemented on c. 1450 kms and orders for c. 2000kms were rolled out in FY 23, with expectations of c. 3000-4000kms annually thereafter. Any slowdown in rollout from the government can impact the business case here.

-

Commodity price increase: Understand that there is no commodity pass through under the contract and thus any material changes in commodity prices can adversely impact the margins, like nickel did in FY 22.

-

Key man risk: • Key Managerial Person (Dr. A J Prasad) is now 77 years old.

-

HBL has developed a second layer of leaders across various businesses/domains viz Mr. MVV Vidyasagar – Electronics, Mr. V Natraj – Energy Storage solutions (batteries), Mr. MSS Srinath for Sales & marketing, Suresh Kalyan COO, Ms. Kavita Prasad for Finance and Dr. Raghunandan Seelaboyina for Batteries R&D. Past ARs have assured of a new CEO, but it remains unfulfilled yet and needs to be tracked.

-

Also, he was accused of conspiring with former KGB officer (around 1995) to try to obtain information about a U.S. Strategic Defense Initiative and was jailed and later released on nolo contendere basis (no contest plea) Source:

-

Poor selection of long-term projects: HBL has a track record of excellent R&D - One look at Annual reports of last 10 years gives a colour of their expertise in R&D - but this did not translate into any revenues and profits over the period. In HBL’s own words:

On hindsight, one could say that

-

The management could have done a better job in selecting projects for R&D - Picking many projects for R&D, all with long gestation (viz 10+ years in R&D in TCAS, TMS, electronic fuses) and mostly all in B2G space (which goes through its own cycles) is a tough space to be in for any business and

-

Also, balancing management bandwidth between existing battery business of HBL vs new projects in R&D could have been done better.

But this seems to have changed now in the last 5 years wherein one can see significant increase in Gross and operating margins, better cash flows, significant reduction in debt and higher RoCE.

They clearly are now focussing on operational efficiencies and better margin businesses in

electronics and defence space.

-

B2G risk: TCAS, TMS, Defence are B2G business and come with with risks associated with government business - Lack of consistency in B2G orders - constant delays in orders, delay in receivables etc. These businesses are slated to become majority segment in 3-4 years time

-

Nickel cadmium battery market is a saturated market. NiCd is a decent size segment for HBL c. Rs 200-250 Cr annually. Europe banning NiCd Battery except for very specific applications - medical, alarms, emergency lights, power tools.

Nickel–cadmium battery - Wikipedia.

Developments here need to be tracked. -

Management DNA/Strengths NOT focused on Scalability/Operational Excellence: Given a choice HBL Management will probably always choose solving complex Technology gaps (which is a rare/great capability), rather than make strategic choices to build inherently scalable business models. “Scalability”/“Operational Excellence” traits aren’t strength areas as evidenced by earlier Lead Acid battery segment operational problems/failure of Retail foray (HBL was technically in a great position to become a 3rd player in retail market, after Exide and Amara Raja).

-

Similarly PLT Batteries segment should have been an easy choice otherwise for scaling up (EnerSys global leader in TPPL/PLT industrial battery sales US$1Bn+ growing annually at >20%) given that HBL Power Systems is probably #2 vendor globally to have successfully commercialised this technology. Northstar Battery the other vendor was acquired by EnerSys in Sep 2019. PLT batteries are a good fit for Data Centre market which is clearly a high-growth segment globally, and in India for many years to come.

-

More importantly, this segment investment/scale-up could have been ideal choice for de-risking the over-dependence on B2G Sales which shows promise of scalability in cornered TCAS Sales (Railways) as does Electronic Artillery Fuse (Defence) in the medium term, but comes with its own risks.

VALUATION MODEL

FY 22 PAT 94 Cr, Cash net of debt 100 Cr, Market cap 2800 Cr

On a TTM basis, HBL is trading at 28x FY 22.

Medium Term Visibility

- Current set of TCAS orders gives visibility of annual execution c. Rs 300 Cr for FY 24 and FY 25 at c. 25% EBITDA margin. Based on budget allocation / inputs from Railway Minister, next year total TCAS orders can be around c. Rs 3500 Cr. Assuming c. 1/3rd share for HBL, FY 25 TCAS contribution could be Revenue Rs 800-900 Cr/EBITDA Rs 200-225 Cr (based on Topline 300 Cr from FY 23 orders and 600 Cr from FY 24 orders)

- Batteries business – assuming baseline growth at c. 12-15% and margins at c. 14-15% (operating leverage, better product mix) will gives FY 25 Revenue/EBITDA at c. Rs 1400-1500 Cr / Rs 200-225 Cr (Important to note that HBL reported c. 15% EBITDA margins in battery segment in Q2’FY 23 already)

- Overall FY 25 could look like Sales/EBITDA/PAT c. Rs 2200 Cr / 400-450+ Cr / 300+ Cr, and thus available at c. 10x FY25 PAT

- For a company in business of specialised technology applications and massive industry tailwinds from railways and defence business.

To summarise, stable growth in battery business and revenues from TCAS provide considerable visibility for next 2 years. This gives the business ample time for other large opportunity size and high margin opportunities to develop viz. EDT, TMS, Artillery Fuses, etc – for further growth in FY25 and beyond.

CORPORATE GOVERNANCE SCAN

1) Payment of Royalty to Promoter in past

In FY2004, HBL agreed to pay Dr. A.J. Prasad 3% Royalty on Sales of Silver Oxide and Zinc Batteries for providing technology to the Company. While Dr Prasad is the primary driver and technical asset for the company, it is slightly unusual for a company to pay royalty to its promoter. The practice of paying royalty was continued till FY 09 and was discontinued thereafter.

2) Promoter family members not attending AGM

Mr. Advay Mikkilineni, Grandson of Dr Prasad, got inducted in HBL Board from 21 Jun’21, but did not attend the virtual AGM held in September 2021.

Mrs. Kavita Prasad, ED of the Company & Daughter-in-law of Dr Prasad did not attend the AGM held on September 2019.

RED FLAGS/FORENSIC SCAN

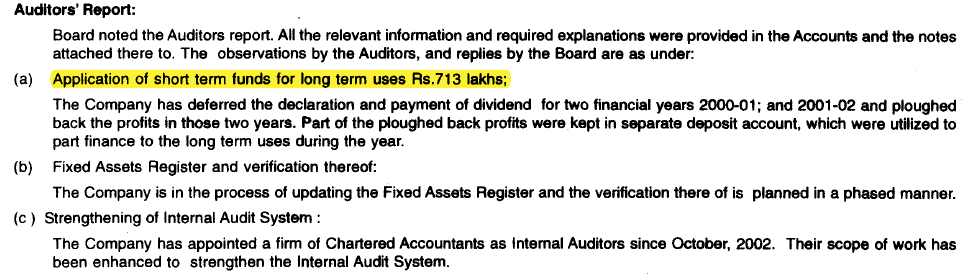

1) Auditors qualification in FY2004 Annual report

While nothing material, the company has been subject to auditor qualifications for usage of short term fund for long term usage and also weaker Internal Audit System.

2) High Contract Labour Charges

The company has almost similar charge to P&L of Contract Wages as compared with normal employee salaries over past 3 years. While it may result in superior flexibility, in past companies like Maruti have faced major issues in 2012 due to dispute among Contract Labour and Regular Workers due to differential charges. It would be important to know whether the contact labour are used at the same premises as regular workers. In such a situation, likelihood of labour unrest has high probability. Since there is no information about average contract wage and salaries paid to Contract worker and Employee, it may be assumed that average contract wages are lower than average salary of employee. If that being the case, then it may result in labour issue in manufacturing company. Having said that, the company has used this way of operation at least FY2014 as per data available and there is no information about labour unrest. So probably management has kept proper check and balance to ensure smooth working and cordial working environment.

Maruti Labour unrest news link

3) Accounting Policies

Aggressive Accounting Policies

- Faced insurance claim related issues at least three times in the past. Insurance claim of Rs 95.16 Lakhs for heavy rainfall during FY2011-12, still shown on Assets side in Claim and Receivables sections.

- Receivables due for more than 3 years - Rs 341.59 Lakhs as on 31/3/22 and Rs 515.12 Lakhs as on 31/3/21 considered good despite long ageing (#of years) and not provided for. Normally, with ageing the chance of recovery declines, unless there is dispute.

Conservative Accounting Policies

- In respect of dies & moulds included in plant & machinery group, HBL Management had (in the past) technically estimated their useful lives at 5 years and the company had continued to charge such higher depreciation (as compared to Schedule II) on the same basis

- Spent higher than mandatory regulatory requirement on CSR over last 2 years.

- Not capitalized its R&D expenditure over more than 10 years despite the fact that some of these products had a long lead time etc.

4) Higher Contribution of Non-Operating items in Net Profit

Sale of fixed assets has been contributing nearly 20% of HBL Net Profits over last 4 years. This is a significantly higher proportion, when compared with other manufacturing businesses.

- Consistently high working capital requirements especially debtor days (FY 21: 215 days, FY 22: 146 days) definitely leave a lot of scope for improvement (though partly mitigated through high payable days)

DISCLOSURE(s) of Stock Story Contributors

Yachna Bhatia: Invested

Donald Francis: Invested

Dhiraj Dave: Invested

BACKGROUND

Source: AR FY 22

Care Ratings

HBL Power Systems Ltd is engaged in manufacturing of different types of batteries, electronics and engineering products based on in-house developed technologies.

PRODUCT/MARKET FIT

MAIN SEGMENTS

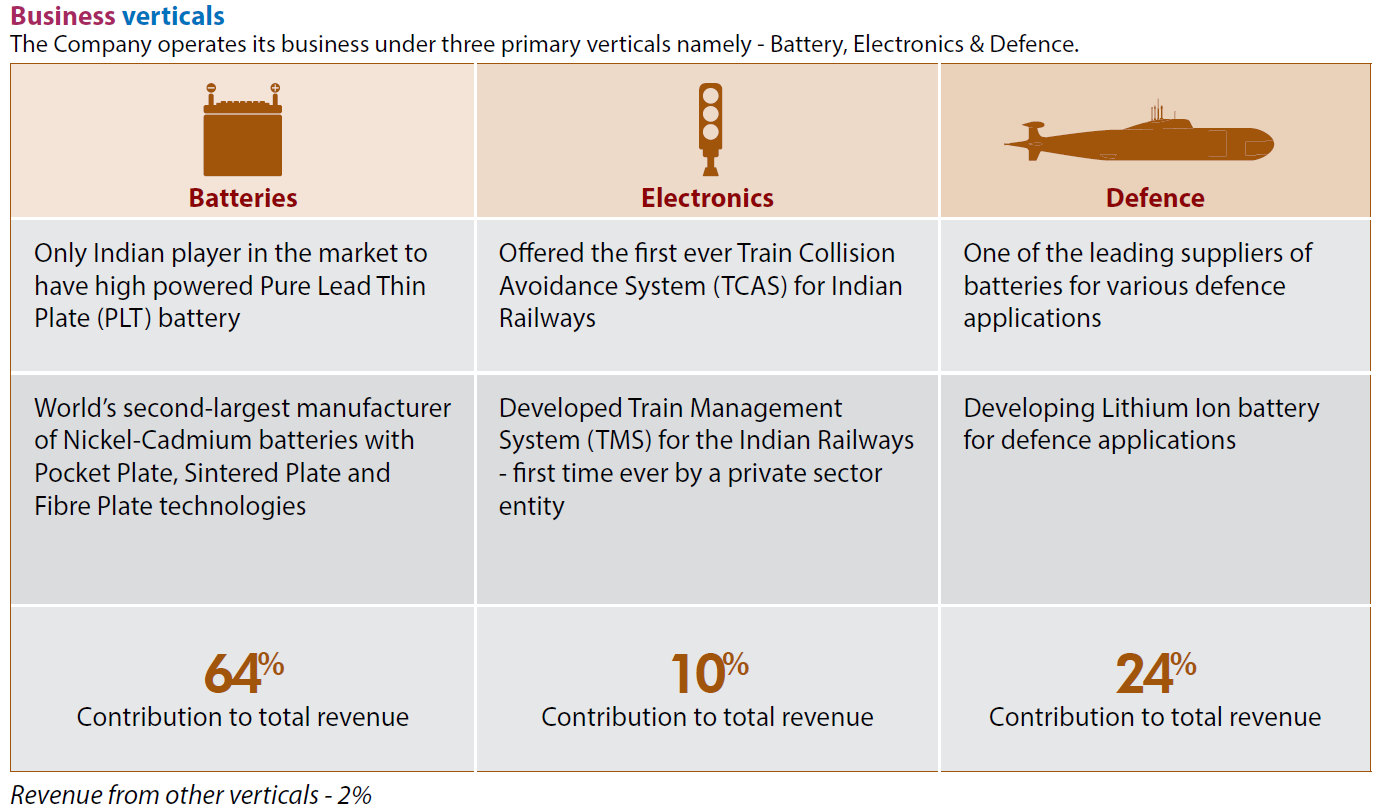

Battery Vertical (~64% of revenues)

The company is one of the large manufacturers of industrial batteries in India. It produces batteries for Telecom, UPS, Railways, Solar, Oil & Gas and power sectors. It produces various kind of batteries such as lead-acid, tubular gel, pure lead thin plate (PLT) and nickel cadmium batteries.

Electronics Vertical (~10% of revenues)

Under this vertical, the company primarily has 2 flagship solutions for meeting the demand requirements of railway signaling in India i.e. TCAS and TMS.

Defense Vertical (~24% of revenues)

The company supplies specialized batteries deployed in demanding applications like fighter aircrafts, unmanned aerial vehicles, submarine propulsion systems, torpedoes, battle tanks, missiles and artillery fuses.

Export Presence

Exports accounted 21% of Sales in FY 22

Quality Certifications/Facilities

HBL is the first company in India to get Silver level certification (upgraded from previous Bronze level) from International Railway Industry Standard (IRIS) during the recent review

assessment by M/s DNV GL as per IRIS Rev 03 (ISO 22163 - 2017).

HBL is approved by FAA (Federal Aviation Administration, USA) for the supply of on-board

nickel cadmium batteries for Boeing aircrafts. HBL is also an OEM supplier of on-board nickel cadmium batteries for aircrafts manufactured by Airbus, IAI (Israel Aerospace Industries), and Bombardier.

The Company’s central test facility at its Shamirpet campus is the only NABL accredited laboratory in India (as per ISO 17025) with the facility and capability of testing all the applicable tests of IEC 60623: 2017, IEC 62259: 2003, IEC 60896 : 2004 and IEC 61427:2013

Change in Name of Company over years

1986: Incorporated Hydrabad Batteries Private Limited

1987: Converted to public limited company & name changed to Hyderabad Batteries Limited

1995: Name changed to HBL Limited

1999: HBL Limited merged with SAB Nife Power System & changed name to HBL Nife Power Systems

2006: Name changed to HBL Power Systems Limited

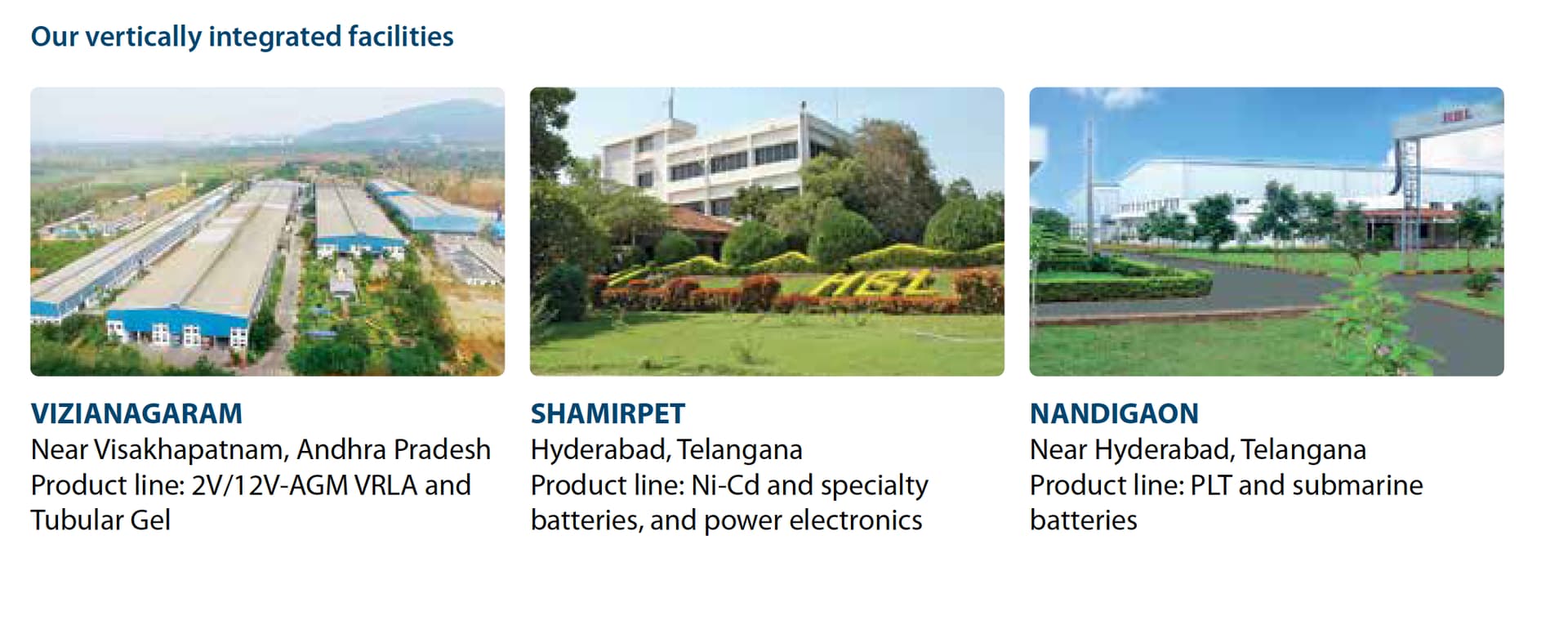

Manufacturing Facilities

Scheme of Amalgamation

In FY17, the company issued ~2.4 cr equity shares of FV Rs. 1 each as per the scheme of amalgamation of Beaver Engineering & Holdings Pvt Ltd within the company. It was the holding company of HBL with equity holding of ~59%. The rationale behind the merge was to enable shareholders of Beaver to hold listed shares of HBL, simplify the group structure, de-leverage the financial statements and enhance floating stock of shares of the company.[1]

Sale of Subsidiary

In FY14, the company sold its entire ~62% stake[2] in its subsidiary Agile Electric Sub Assemble Pvt Ltd for ~175 crores[3] It also booked a profit of ~62 crores on the sale.[4]

Agile Electric was involved in the production of DC and AC motor sub assemblies. It was sold to Blackstone Group.[5]

Sources:

- TCAS Handbook - April 2021 (here)

- Kavach Dashboard (here)

- Cost Breakup of Kavach Work (here)

- HBL Wire - Jul 2020 Issue 03

- HBL Wire - Sep 2020 Issue 04

- HBL Wire - Dec 2020 Issue 05

• Silver Oxide Zinc Storage Battery #

• Ni-Cd Aircraft Battery # - VLRA Battery #

Reference:

- Kernex 2020-21 AGM Recording (here)

- AGM updates of Kernex and HBL AGM Updates