Rating reports/Interviews/conf. calls etc. are public disclosures accessible to all. Another example was physical AGMs where only those who travelled got access to information. There will always be information gaps between active investors who seek info and passive investors. To its credit HBL comes up with excellent annual reports too. Even here on this thread you have been able to figure out the Ashoka Buildcon angle just by digging info.

My personal take is I want to be fairly satisfied by most things like disclosures, corporate governance, capital allocation track record and a lot of other subjective things but get the business trajectory right. I want to get these things ‘Mota Mota theek hai’ but business trajectory ‘Solid hona chahiye’. By doing this I ensure that I have a much larger set of companies to work with and that I don’t miss the wood for the trees.

If you have a different view on this that is perfectly fine too.

I couldn’t find any news about Phase-1 COD (Commercial Operation Date) with Google search or Q4/Q1 results. Here are various companies involved in Lithium ion batteries/cells in India. There’s a GODI India mentioned at CSIR, Chennai with BIS certification. Most are for 2-4 wheelers (not sure how complex & different it is for HBL’s use-cases).

This information is from care ratings report that came out in Oct. last year:

This is from their FY19-20 AR. NSTL is DRDO equivalent for Indian Navy. As mentioned in the AR the usage should be for defence, energy storage and e-vehicle applications.

Thanks Anant.

Below is just info, not related to HBL Power at all.

Apparently, stationary energy storage solutions at home/chargers (esp with Li-ion battery packs) don’t need a fully healthy battery at all, it’s enough to have a bank of “retired old” batteries of various “ages”.

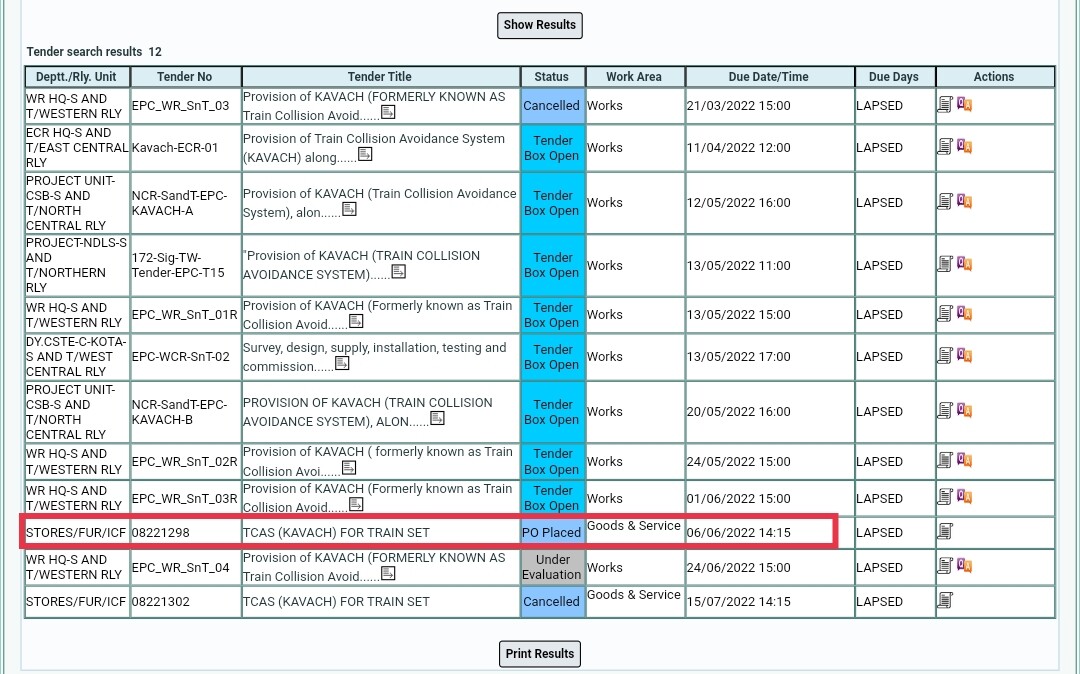

Current status of the tenders - Western railway tender on the top which got cancelled is now under evaluation. ICF tender on the bottom which got cancelled has been finalised with KERNEX (25Cr approx)

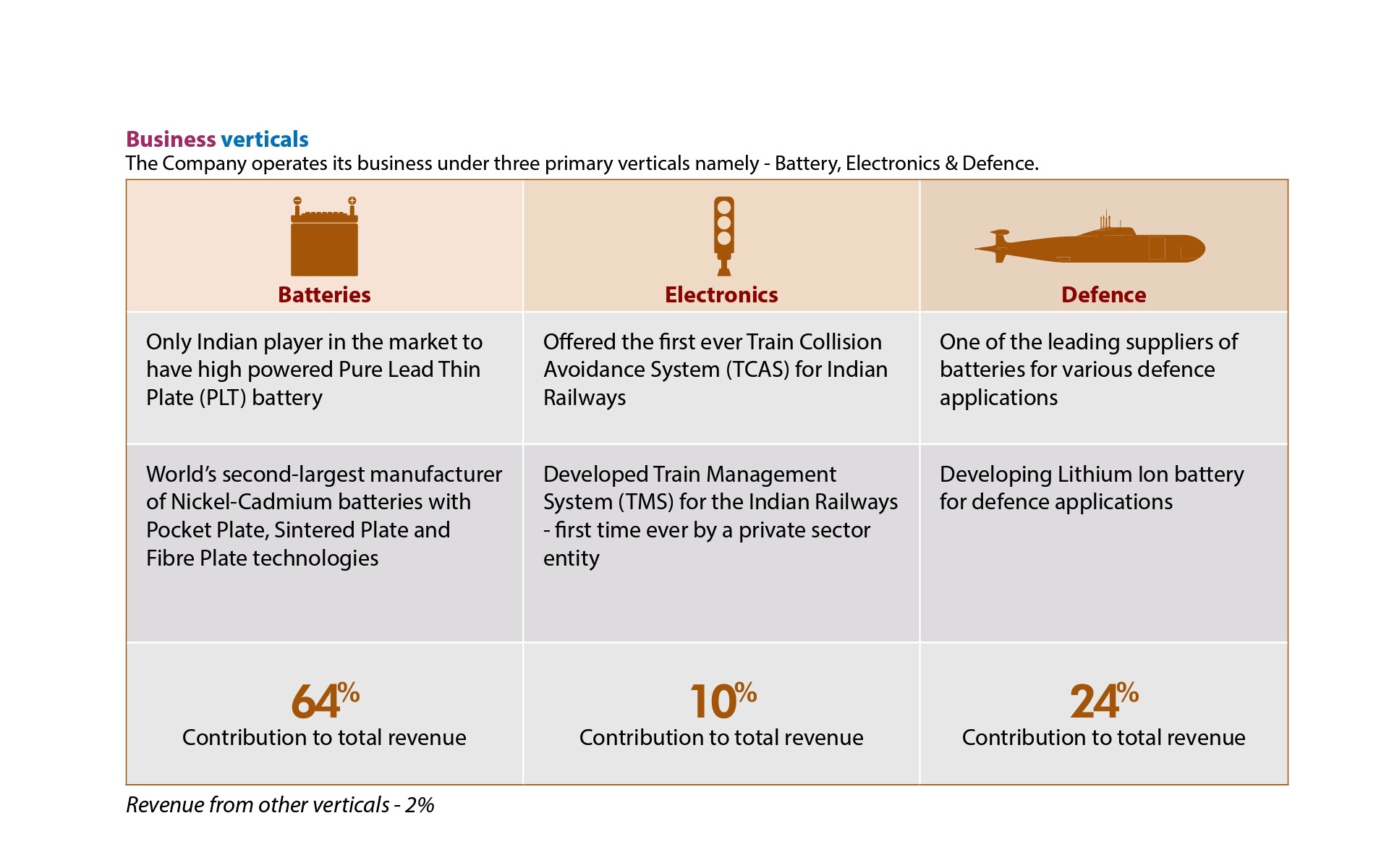

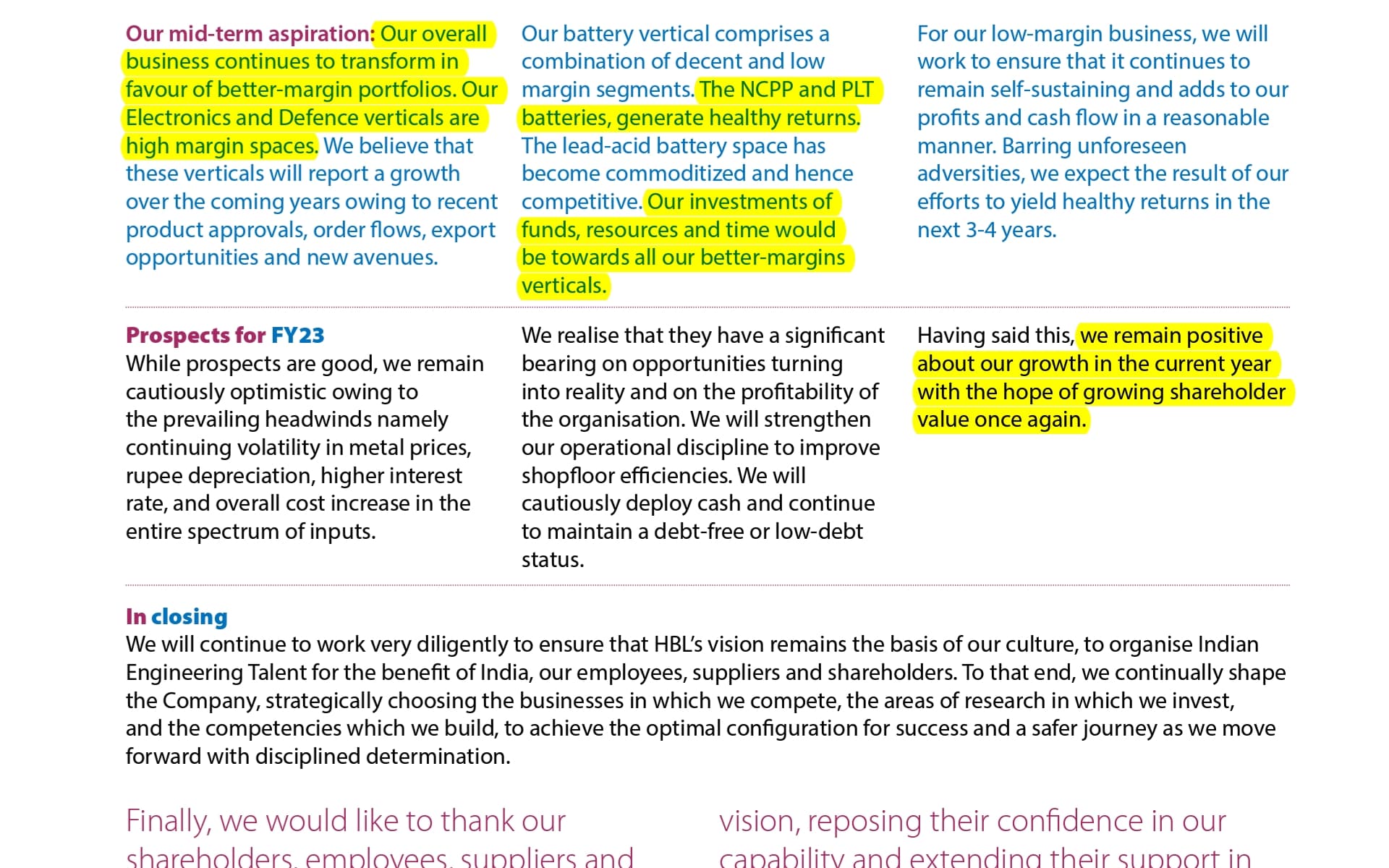

Its an improving product mix thus margins case( low margin battery majority to High margin electronics + defense + battery mix improvement , supported by end sector solid demand tailwind. Being debt free helps further.

Given FY 22 electronic was at 10% of revenue and defense at 24%, 120 cr type railways & 300 cr from defense and margins are nearing low/early teen with.

Looking at recent wins of 700cr+ from Railways ( TCAS + TMS and across corridors as well as Vande bharat coach factory) – 20%+ from railways share is possibile even if 1/3rd order book is executed this year. Defense commentary is strong as well. Together a meaningful higher contribution with growth trajectory, hopefully mgmt gives more details in AGM.

Technicals and newsflow on 700 cr+ Railways bid wins are supporting the case

Thanks @Anant for wonderful insights in thread, including key aspects of R&D success vs R&D conversion to commercial success attribute as key monitorable.

A couple of additional observations from the annual report

The business segments described in the report do not tally with the quarterly results for FY2022. I believe it is because of the battery segment which cuts across the defence segment and is packaged differently in the annual report. A minor annoyance, that can perhaps be avoided by being consistent.

The work on EV retrofitting technology for light commercial and passengers vehicle. Powertrain retro-fitment is at a nascent stage. A quick google search tells that the current market focus is primarily on 2W and passenger cars.

As we all aware the main investment thesis for HBL is Railways Electronics TCAS/TMS/Interlock (oligopoly/sustainable scale up). Reportedly this segment is slated to become the major segment in next 3-4 years. Defence segment is seen as lumpy order-flow (though that is changing?).

There is another market that HBL has started addressing with significant vigour - PLT batteries for Data Centres (DC). in last 3 years this segment reportedly has steadily grown to around 150-180 Cr annual business. Given the huge demand for Data Centres in India (to be accelerated with 5G rollout), this could again be a very important fast-growing scalable segment for HBL?

We have been spending energies to understand this market at some depth. Summarising below the takeaways from interviews with two DC domain experts.

Data Centre Market in India - Scale of opportunity/Current Players/Current Active capacity

Initially in '2000 only 3 players - Sify, Tata, RIL. In a few years Airtel, Net4India and another player entered the fray. in 2010 NTT acquired NetMagic. AT&T, BT, Verizon also enetred the Market but mainly restricted themselves to Telecom space. they are yet to expand.

By 2010 other players like CTRLs, ESDS, Tulip (could not sustain). CTRLs has established a Pan India presence. Yotta entered market in 2019 identifying a gap for large scalable player.

By 2020 market was maturing attracted global players like ST Telemedia which bought over TCL. Equinox acquired GPX (more Telecom domain player). COLT and BRIDGE are other players. Adani has a JV with DRT

Hyperscalers - AWS, Microsoft, Google - Cloud players

Data Centre Infrastructure Builders - STT, Yotta, CTRLs, Nextra, Equinox, ESDS - 10-12 active players.

Data Centre Infra guys - are trying to sell to Enterprises, Government, Wholesale Buyers. Wholesale Buyers could be MNC captive, Hyperscalers, OTT/Content players. Nobody talks small these days. Even the smallest guy will say he is building 100-500 MW. And everybody is hoping Hyperscalers will buy from them

RIL Jio is on his own - building for own business needs - not trying to sell infra to others. Though this is likely to change as bulk of the Market is moving from Core DC to Edge DC (closer to the customer, and with 5G Edge requirements will be huge 10x Core). Once RIL integrated offering is ready, probably the game plan will be to serve Enterprise DC requirements from Mobile Edge centres.

Anyone with core expertise in IT Services/Real Estate/Land Holdings looking to expand into DC services in India. L&T is coming up; Raheja has announced plans, as have Adani

Someone like Adani (despite many announcements) will probably NOT go big. He will build as he gets committed business. There are already players like Yotta who have a big presence, and are expanding pan-India

Current total active capacity in India will be about 65000-70000 Racks, 450-500 MW. The market is booming. But we have to take what everybody says with a pinch of salt. One maybe putting up a building that can cater to 25 MW, but putting in DG, UPS/Batteries for 5MW, and actual load maybe 1 MW. So discounting all of that it will be safe to say current active capacity should be around 450-500 MW. Slated to go up 3-4x in 3-4 years

Situation is analogous to how it was in 1998-99 for Telco players. There were like 20-25 players. Similarly here 10-15 players are active today in DC. Some will NOT get any business and will close down. Severe Consolidation expected within 3-5 years leading to only 4-5 players remaining

Trends Big Data Centres vs Smaller Data Centres

in 2016, 7-8 MW was big. 2018 15 MW was a big DC. Today nobody talks of putting anything less than 20-25 MW. Some talk of 50 MW and 75 MW. This is the IT power. Total power you should multiply by 1.5x

One can put up much bigger 200 MW also. But problems are twofold a) Getting large power at each location b) land rates are very high

Instead of building vertically (more complexity/cost in strengthening building load handling capacity, goes up by 3-4x), the trend is now more clearly towards horizontal scale-up within a Campus

Bigger trend is now towards smaller Edge DC (5-7 Mw, scalable to 25 MW) close to the customer

Already established players are taking the position of existing Supply creates demand. Its a supply-driven business, they opine. Customer likes to see the choices he/she has, rather than depending on paper plans (read announcements). They are moving to create pan-India presence.

Yotta has a 40MW (~7000 racks) live location. Another 60 MW (~8000 racks) coming up in Navi Mumbai Campus. Next is a 10000 Rack DC. Plans are afoot for 100 EDGE, 11 of these are operational. Plan is to deploy 1L racks in 5 years (double of current India capacity)?. Coming up with a Hyoerscaler DC at Kolkata (Kolkata will be the 3rd cable landing station in India) - acquired 100 Acre land (erstwhile Hindustan Motors)

Smaller players/New players are playing a wait-n-watch game, try and catch up when demand peaks. Both strategies bring their own set of pros & cons

RIL/Jio integrated plans are seen as the biggest threat once 5G is deployed countrywide within next 2 years. This again lends some credence to the case for existing players trying to get their feet/roots entrenched before the inevitable onslaught/consolidation

Costing/Contract Trends

Roughly 80K - 1L per KW rentals

Contracts are usually 1,3, or 5 year durations. Renewable yearly with some negotiation from both sides

Hyper-scalers/Enterprise Customers are usually technology-agnostic. Data Centre Infrastructure guys take the technology/vendor decisions based on a TCO (Total Cost of Ownership) approach

UPS/Battery Technology Choices/Adoption

90% of market today is served by VLRA/improved versions like PLT/TPPL

5-10% served by Li-Ion

VLRA shelf-life 5-6 years; improved VLRA 8-10 years; Lion 15-20 years; VLRA space is larger; Lion much lesser maintenance life cycle issues

Lion 3x VLRA costing today; Smaller rack size, smaller SMPS for Lion catching up trend; Lion NOT cost effective for below 10-15 MW DC

From a TCO (maintenance/sustainability/effective life) perspective for big capacity DC guys - 25 MW & above, Lion becomes cost-effective and they are able to compete. For mid-size DC players or someone setting up a captive enterprise DC, VLRA/PLT is more cost effective

Given the market trends of exploding numbers for EDGE DC, Korean Lion players like Samsung and LG are looking at promotional rates/ will be forced to offer more competitive rates in order to harness the opportunity. As consumption increases, prices will decrease

Big players like RIL Jio plans reportedly are of putting up 400-800 MW in next 3 years. There will be at least 4 Tier 4100 MW DCs. Nagpur, Jamnagar and Mumbai and Kolkata are prime locations. 40 Tier 4 MEC (Mobile Edge computing) sites where DC capacity will be around 25MW. MEC sites will start with 5 or 10 MW and eventually grow to 25MW over 3 to 5 years.

These kind of huge numbers are likely to accelerate the trend towards Lion as market forces come into play and make it much more cost-effective and competitive even for lower capacity Edge/Core DC

Environment/Sustainability trends also point towards accelerating Lion

UPS/Battery Main Vendors/Deployments

UPS - Schneider, Emerson, 3-4 main players

Lion - Samsung, LG, Panasonic, Chinese, Others

VLRA+ (TPPL/PLT) - EnerSys, HBL

VLRA - Amara Raja, Others

Outage support requirement is 15-30 mins globally.

In India strangely this is 2-4 hours (UPS/Batteries/DG). Perception is rains play havoc here, besides lesser utility reliability. Players/Customers coming round to accepting 2 hours backup support increasingly (segregating actual IT Load vs other non-IT office loads)

All DC requirements in India are of Tier 3 and Tier 4.

Industry is coming round to offering Tier4 at Tier 3 cost (1L/Kw rentals) by optimising on design/cost affordability. Yotta 40 MW Tier4 Navi Mumbai-Panvel is the 2nd largest deployment in the world (?).

DC Standards/Certifications of existing deployments:

Design Certification (mostly everyone boasts of this) (99% in India)

Construction Certification (constructed as per design) (very few can claim this)

Operational Certification ( 0.5% in India can claim this)

Incidentally Operational Certification deployment claims are of less than 5MW DC. Sometimes even for 1MW. Operationally very complex/costly, 6 month audit showing 100% uptime )

Yotta - All Lion

NetMagic - All Lion

Airtel (Nextra) - All Lion (Microsoft Azure hyper-scaler set up)

Availability of Lion is a big issue currently. Lag time is there

5 months has come down to 2-3 months, but can be a big issue for someone looking to accelerate fast execution

TBD (yet to establish)

Addressable market for HBL

Replacement Market share

Attractiveness of PLT/TPPL for VLRA replacement

Effectiveness of PLT/TPPL with Integrated BMS offering with proactive maintenance support vs Lion offerings

Major deployments of big players

PS: Am actively inviting DC Domain experts from Industry to take this forward from here and help us establish Pt 6 more concretely. DC domain guys lurking within VP community, please put your hand up and help refine/take forward findings

The last two days have been extremely eventful incase of HBL.

a) The announcement of award of Kavach tenders of around 660 cr.

b) Annual report.

The following is my reading:

Kavach order win is a vindication of a long journey of over a decade and the pain/struggles/mental and financial stress that a promoter/business owner goes through while working on something as complex as Kavach. What one does not also see are the numerous Kavach like projects which fail to see the light of the day. On TMS:

In my opinion the most important thing in this year’s Annual Report is the +ve announcement of Electronic Interlocking being ready for field trials. EIS is another extremely complex system dominated by MNCs like Siemens/Alstom/Kyosan and Medha being the only Indian player.

On the direction of the company:

Looking at the investments that the company has made in TCAS/TMS/Interlocking/EV it is very clear that the revenue profile of the company could completely change in next few years. In all likelihood Electronics could overtake the revenues of the battery segment in few years.

On the battery segment the focus is on value addition and differentiated batteries with a constant reduction in the standard VRLA for telecom with increase in PLT. As expected PLT seems to be evolving as a major growth driver

Nickel price fluctuated significantly during the initial days of Russia Ukraine conflict. It would be interesting to understand the inventory gains/losses this year.

In conclusion the Kavach order win and improvement in battery segment should ensure a healthy topline and bottom line performance over the next two years. This will give ample time and cash flow for business like TMS/EDT/Li-ion/Interlocking etc. to move forward. The next year’s budgetry allocation for Kavach is a key monitorable as that will ensure further order flows for Kavach as promised by the government.

Apparently any TCAS OEM can share an authorisation to EPC contractor who possesses financial capability to execute

I think Kernex must have used this route – for the ECR tender with Ashoka Buildcon

The 2 other vendors have sought for development as TCAS OEM with RDSO and are getting ready with their own prototype.It may so happen that pace of tender is slower and in this time some new vendors jump on the bandwagon after getting the approval

Also both these vendors are having good relation with Railway already

Quadrant future Tek is manufacturer of E-beam cables and other railway cables which are required to be approved by CLW I suppose

GG TRONICS Bangalore seems a very strong player as it is already doing RDSO approved safety embedded systems for railways I think

Dear Prateek- Thanks for sharing your views. Regarding two new vendors your views are very informative but Kernex or Ashoka had never disclosed as that order is for Consortium.

How much TCAS orders might come from IR for this FY?

Hi Anant(@Anant) - Thanks for sharing your in-depth research.

IMHO, this business lacks an ‘accountable management’ who has the skill to convert the exciting market opportunity into a commercial success. Why so?

In the past few years, the business faced tough times under the current CMD and he is still likely the key decision maker. Across various ARs, nuggets are sprinkled where hardships are assigned to various external factors - external environment, wrong people in decision making etc.

The present COO who is with the business from 2014 onwards is a core finance professional whereas the organization’s core business is the design and development of engineering products, involving R&D in various fields of engineering - Electronics, Electrical, Mechanical, and Chemical.

Past ARs assured a new CEO in FY17, but the same remains unfulfilled. Being an internal matter (suitable CEO, COO), it seems most easy to fix as an outsider.

With such decision-making at the top, I wonder how this organization could influence the external environment to grow sustainably.

Hello Surender,

I agree with your assessment of the management and the management has done poorly on almost all business aspects from operations/sales/marketing/strategy and even capital allocation. What makes me stay +ve on the company are emerging large opportunities on the electronic/railway side and the way they have deleveraged their balance sheet. In my experience business momentum takes precedence over everything else and sometimes when management starved of capital gets access to it a lot of past ills get fixed. It can also go otherwise where they squander these opportunities and that is a risk I am taking.