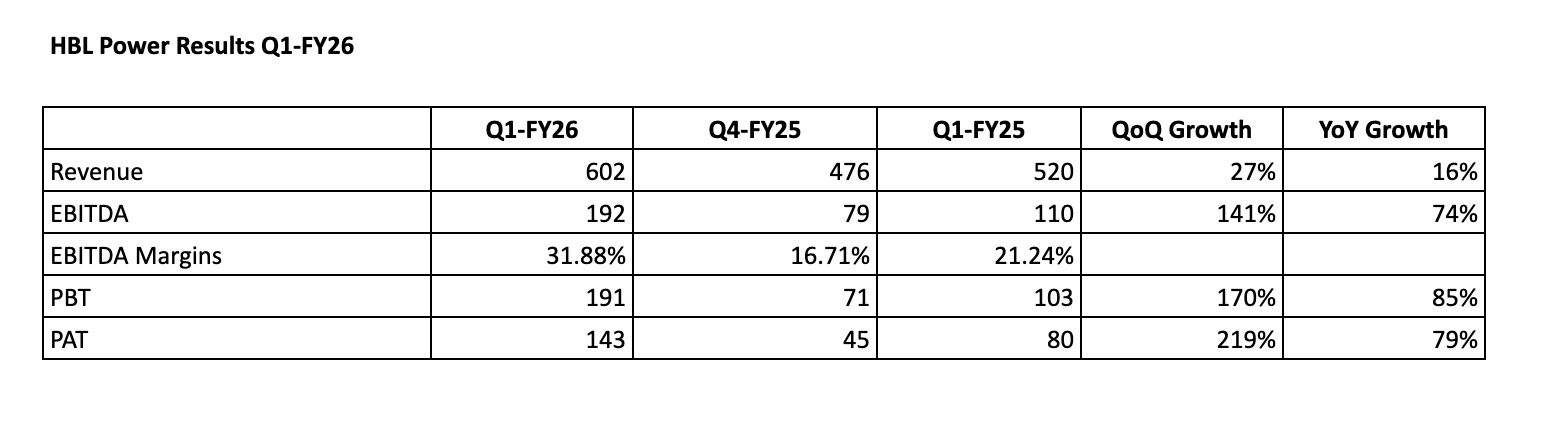

54% revenue growth guidance for FY26

18 Likes

Recently Kernex has won 2 orders for more than 400 cr. How come HBL has not received any order? As yet it is the only company to have received Kavach 4.0 certificate. Which implies that other companies are yet to start Kavach work, when HBL has already started rolling. Company it self projects 50% revenue growth, which it may surpass, as it is a conservative management. But all these developments are yet to be reflected in stock price where as Kernex has almost doubled within last 2 months. Am I missing something?

6 Likes

That’s not entirely true. HBL went from 400’s to 600’s in last 2-3 months. Both Kernex and HBL are 10-15% down from all time high.

Railway contract companies behave like cyclicals. When the tide turns, usually the weaker players give more returns compared to market leader. Street Lag as discussed by @hitesh2710 sir might also be at play. I also think that for HBL, Kavach is an open cracked story, focus must be to investigate the developments on the Electric Fuze and EV Truck front. These two product lines need to fire up before kavach starts to dry up.

15 Likes

HBL Received the order worth 132 cr from south central railway today 14th June

5587b784-d66e-49c2-8ce0-c9e687f26942.pdf (589.8 KB)

2 Likes

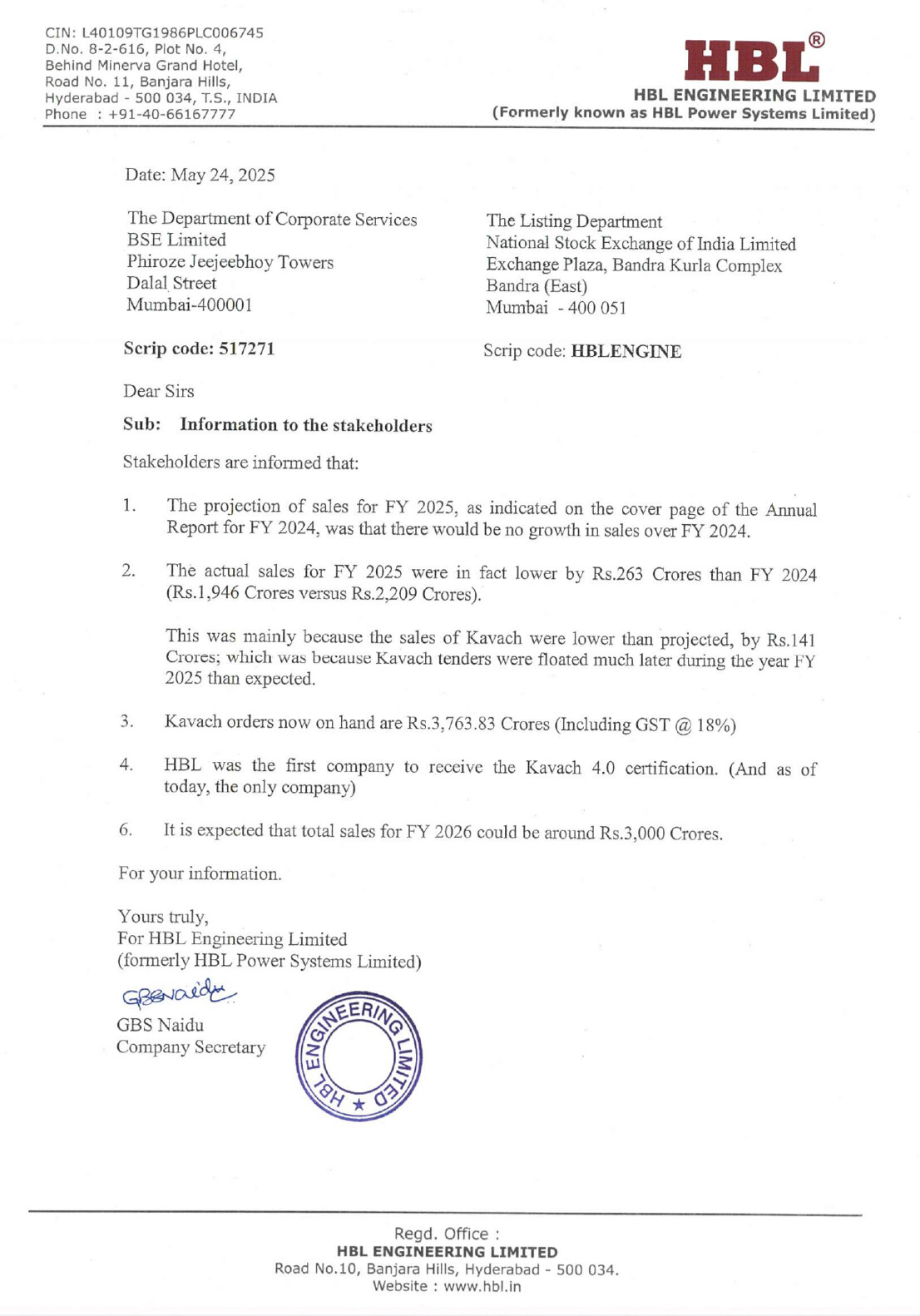

With this the total accumulated order book stands almost at 4000cr (3998.328 to be precise) as compare to fy25 revenue 1967cr. Not sure how much they can realise by march2026 ?

3 Likes

most of the order values are inclusive of GST at 18%,which doesn’t form part of the top line. Net of GST order value would be ~ INR 3390 Cr. (3390 +18% GST = 4000)

6 Likes

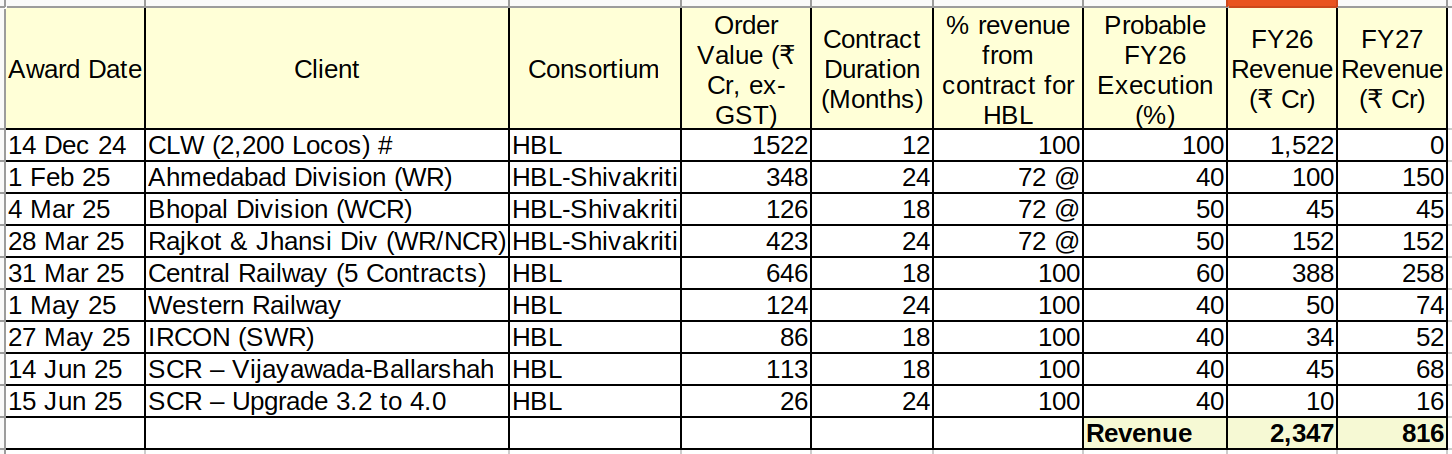

My projection for FY26 revenue -

Also, assuming no growth or de-growth in industrial batteries, defence & avionics batteries.

The revenue as of today should be around 1396 + 227 + 2347 = Rs. 3,970 crores.

#

Basis of assumption that the contract will be delivered in time is the presentation of Kernex microsystems dated March 2025.

The company mentions in the presentation that the following parts of the contracts have been completed -

- The project survey has been completed.

- An awareness program was conducted for client teams at the Loco sheds.

- The layout for test benches has been completed.

- The production of simulators is ready for inspection.

- Purchase orders for materials have been placed, and material supply began in the second week of April 2025.

- Deliveries are expected to commence by the end of May 2025.

- Installations are planned to start from June 2025.

General timeline for such type of projects are -

-

Planning and Design: 1–2 months (per locomotive type)

-

Procurement and Preparation of Components: 2–3 months

-

Installation of Onboard Equipment: 7–10 days (per locomotive)

-

System Integration and Testing: 5–7 days (per locomotive)

-

Field Trials and Validation: 1–2 weeks (per locomotive or batch)

-

Certification and Commissioning: 2–4 weeks (per locomotive or batch)

-

Training and Handover: 1–2 weeks (per batch of personnel)

-

Total Estimated Time per Locomotive: 3–8 weeks (depending on scale and readiness)

@

72% share of HBL-Shivakirti consortium is based on the historical tenders HBL has done with Siemens in 2022 for deploying the Kavach system over 260 km of track and 120 locomotives, worth ₹286.69 crore, with HBL’s work share reported as ₹205.88 crore (approximately 72% of the total contract value), is sourced from the following:

-

HBL Power Systems’ Annual Report (2022–23): This report details the company’s role in the Kavach project and specifies the contract value and HBL’s work share. The annual report is a primary source for financial and project-specific information related to HBL’s involvement in railway contracts.

-

Financial Express Article (September 25, 2022): The article titled “Kavach: Indian Railways’ indigenous train protection system gets a boost with new contracts” provides details on the contract awarded to the HBL-led consortium, including the total value of ₹286.69 crore and HBL’s share of ₹205.88 crore. It highlights the scope of the project, covering 260 km of track and 120 locomotives.

Edit 1 -

- Corrected the contract value of CWL loco contract.

- Improved modelling of percentage completion of CLW loco contract based on information previously unknown to me.

- Because of CWL loco completion time, new tender win on 15-Jun-25 and revenue share of Shivakirti in consortium contracts the revenue estimates have changed.

Disclaimer: Invested in HBL Engineering. This post is for academic purposes only, based on publicly available information, company announcement and my assumptions. I’m not a SEBI-registered Research Analyst or Investment Adviser, and this is not investment advice or a recommendation to buy, sell, or hold securities. I may be completely wrong. Do your own due diligence and consult a SEBI-registered advisor.

P.S - I want to thank @fabregas for pointing out the error in amount of CLW contract value.

15 Likes

Thanks for this table, really helps…

Contracts of 18 and 24 months may see higher bookings towards the end of the execution timelines, with adjustment to that effect, and given the execution capabilities demonstrated by HBL, the prospects in the coming year are encouraging.

Disc-invested and biased

4 Likes

Thanks for providing this information. HBL has already given guidance for FY26 of ₹3000 crore, depending on execution. For FY27-28, if the EV truck business kicks off, it will be a business to watch. The only downside is their current over-dependence on Kavach orders. I don’t have huge confidence in EV trucks, as EV adoption has been slowing down in favor of hybrids.

4 Likes

Thanks for the table. It helps us arrive at an estimate for FY26. Some observations:

- The loco KAVACH order value mentioned in your table seems to be incorrect. The total order value is around 1800 Cr incl. GST. Excluding GST it comes to around Rs 1518 Cr.

- You have estimated 85% execution for the loco KAVACH tender. That is quite optimistic in my opinion. During a concall Kernex management had expected the Loco KAVACH execution to begin only by June. No indications by the managements of HBL/Kernex/Quadrant Future Tek or Mr. Market that this execution has begun. I may be wrong.

- Also, if I remember correctly, during the latest concall Kernex management had said that any Loco KAVACH deliveries which are not completed by Dec 2025 will compulsorily go for re-bidding. I am not 100% sure about this but if this is correct then there will be no revenue for this Loco KAVACH tender in FY27.

3 Likes

Thanks for bring it to my attention, I will amend the table accordingly.

Kindly quote the source. I could not find any concall transcript on Screener.in or youtube.com

1 Like

I had attended the concall. There is no transcript posted by the company.

During the concall Kernex management had said that the reason for delay in starting execution of Loco KAVACH tender is because of infighting/uncertainty within Railways regarding who will inspect and certify the installations being done by KAVACH vendors. Apparently the Electrical Division has released the tender but they say that they do not have the technical know-how to carry out the inspections. They want RDSO to do the same. RDSO, apparently, does not have enough man-power to carry out these inspections at multiple sheds across the country. So the management’s expectation of installations starting by June was based on the hope that if they are further delayed then there is no chance that 100% installations can be completed by December. It was more of a request to Railways to not delay installations any further.

12 Likes

Dear Anant sir @Anant

At the onset, expressing my gratitude to you for all the valuable insights over last many years.

Have been following your posts and learnt a lot.

May I request your viewpoints on HBL - especially the road ahead from here and how you are valuing the firm.

As per information available, it is currently at a very interesting juncture with several strategic business lines ( most of which have tailwinds of different levels)

While I am quite excited about these opportunities , purely from a valuation(and associated risk) I am kind of stuck and seeking your expert views

Salient points

- Hbl at current price is being valued at market cap of 17470 cr

- Even going by company’s version of guidance for next 3 years , sales would be ~3600-3800 cr in fy28 (30% in fy26,20% in fy27,28)

- Even valuing the company at 10x fy28 sales ( which is definitely not cheap from an academic perspective) …return would be circa 2x in 3 years (good but nothing extraordinary)

- While there are multiple tailwinds in kavach, the management estimates are subject to multi year execution risk and delays in government orders etc.

- One side of me says .. Market is seems to be pricing a lot of future positives and there is very limited room for disappointment

- Could we say that most of the re-rating is behind us & going forward -stock would reflect business performance & growth

While this is specific to HBL , using this as a case study to learn about high growth companies with strategic long term opportunities and how to value them.

Many thanks!

23 Likes

Any update on field trial orders for kavach to concord ? Company seems to be not updating any new orders like other SMEs do.

HBL did 2000 crore sales last year, and this year they have guided around 3000; therefore, a 50% revenue growth for this year. Next 2 years they have guided 20%, therefore 3600 for '27 and 4320 for '28. Obviously, it depends on their execution. I believe they should have these quarterly concalls more frequently for shareholders to get more clarity on the next growth triggers for the company.

7 Likes

HBL does not do quarterly con calls. They do an annual investor call. Last year it was in July. Waiting for the announcement this year. It wasn’t very well conducted though.

Their execution has been very good so far. The fact that they were the first to have Kavach 4.0 approved reinforces this.

Apart from the uncertainties in kavach execution (I am comfortable with their execution capabilities, we have to see how IR supports their dependencies), we have to think how long will kavach opportunity last and what lies beyond kavach. current valuations already factor in great outcome for FY26 and FY27.

Disc - invested from lower levels.

14 Likes

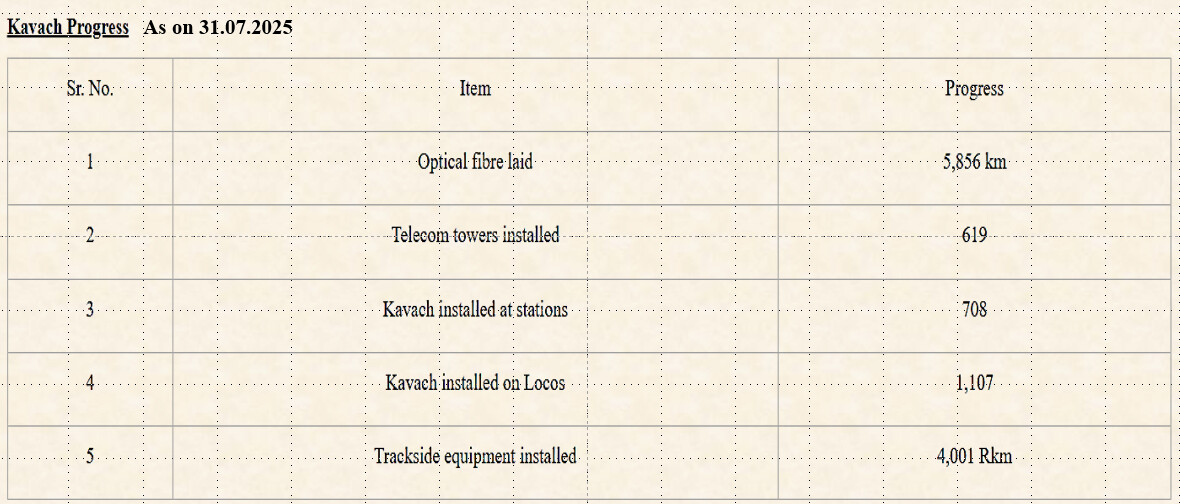

Kavach Installations are in very slow pace?

Tenders are issued to complete the Loco Kavach installations by Dec’25 in approximately 10k locomotives but so far the number is around 1100. Hope the pace of installations are picking up in this quarter and thereafter…

for detailed information:

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2150296

With thanks

Disc: Had holdings

7 Likes