Is that not an accounting thing arising out of quarterly reporting ? A company making devices has to have it stuck in inventory/WIP until it is sold..here deployed for kavach installation . So the amount showing up here was spent earlier and is ultimately coming to bottomline .So if this is artificial shoot up then there was artificial shoot down in previous quarters .Atleast thats what I think. Explain if something else is there .

13 Likes

Friends if we remove the inventory effect on sales and profit what will the impact on our monitoring parameters? And, may be, on our conclusions?

1 Like

HBL q1 FY 26 results showed impressive growth in profitability on the back of execution of Kavach orders. Segmental results indicate good traction in Electronics division. This division contributed 180 cr sales and segmental profits were 89 crores. There can be debate whether these kind of margins are sustainable or not. One has to look at the bigger picture that can play out over next 2-3 years. And the good news is that the Kavach execution has begun with a bang and on the back of 3600 crores plus orders in its kitty and approval for Kavach 4.0 ( as on date the only player to receive it) we can see further traction from electronics division going forward.

The Kavach 4.0 approval was received midway in the first quarter and execution of orders received post Sep 2024 could begin only after that. So company could have a time of around 1 to 1.5 months to execute the orders during the quarter. Going forward we could see the Kavach order execution for a full 3 months during q2 Fy 26 and subsequent quarters.

Electronic fuzes, defence batteries are other segments to watch out for going ahead and need close monitoring.

Going ahead, the speech of the chairman during the AGM could provide further pointers regarding future growth trajectory. Management has already indicated a revenue target of 3000 crores for FY 26.

disc : invested.

69 Likes

Sir ,could u help understand stock inventory build up in the profit and loss statement. How to understand it . Thnks regards

1 Like

Implementation was slow till Q1 because Kernex said they do the implementation between Q1 and Q3 where as order was received last year in December. So the same was followed by HBL as well, as per my analysis and past track record of the company, 80-90% implementation will be on time rest 20% may delay and this is ideal case.

3 Likes

For companies like HBL with clearly mentioned order book, and approval for Kavach 4.0, the important thing is to see how the execution is going. The current quarter gives some idea on how things are going and directionally things should only improve from here.

The idea is to look at the bigger picture rather than get lost in mundane details. I don’t involve myself in looking into minute details about the company..

27 Likes

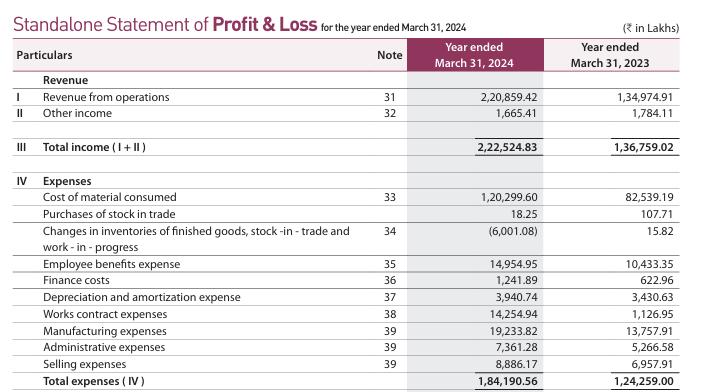

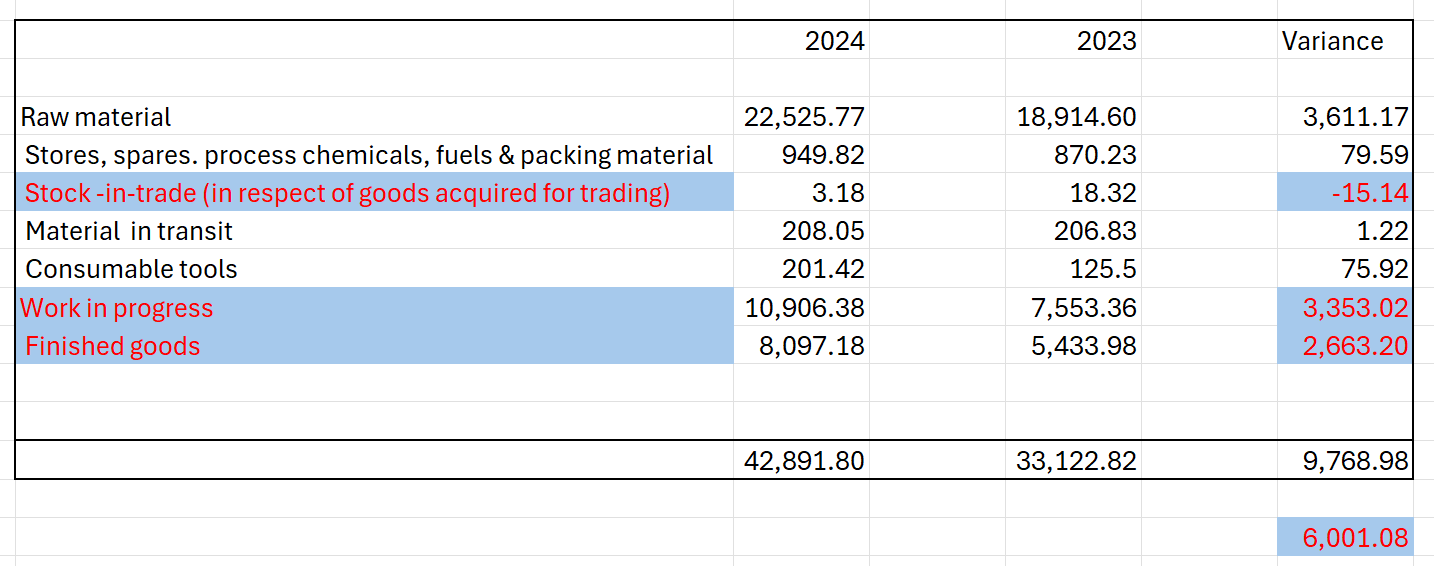

There is nothing unusual about it. Its just a function of accounting in manufacturing companies where in all the costs are initially expenses and at quarter / year end finished and semi finished stock is calculated and reduced from the expense (and added to the inventory in the balance sheet). For quarterly accounts there is no balance sheet and disclosures else you can directly tie it back to the finished goods and work in progress movement. See below from year end accounts:

You will see a similar amount of (6,001.08). This you can tie in inventory movement of fixed assets and work in progress (see highlighted cells below).

Hope that clarifies the doubt.

8 Likes

HBL ENGINEERING Q1 FY26 Results

Company has outperformed on every front whether it is Revenue, EBITDA or PAT. We have seen Very good execution in Electronics Segment which is basically KAVACH.

4 Likes

Robust Order Book:

•Gives perfect Revenue Visibility

•Company has good execution track record

•More new orders under pipeline

10 Likes

FINANCIAL MODEL FOR FY26 and FY27

Assumptions:

Revenue

- Industrial Batteries - assumed 5% YoY growth.

- Defence Segment - assumed growth rate of 30% in FY26 and 25% in FY27 because as we seen in Q1 results growth is robust and management said there are many good orders for this segment.

- Electronics (Kavach) - Order Book of 4000 Cr and traction come in this segment. Taken as per execution time line conservatively.

Margins

- Industrial Batteries - 24%

- Defence Segment - 40%

- Electronics (Kavach) - 25%

Interest and Other Income - Other Income is as per past trend, and Interest is higher then last year because of higher working capital will be needed as revenue grows.

Depreciation - As per Quarterly runrate, as company is not needed to do much capex.

Tax Rate - 25%

This gives the PAT of 746 Cr in FY26 and 893 Cr in FY27, which is almost 3x in FY26 compared to FY24 and 4x in FY27 compared to FY24.

Valuation seems lucrative as stock currently trades at ~20x FY27E earnings and High visibility order book make it more reliable.

Hence, Room for “multi-bagger” upside if execution continues.

16 Likes

HBL sent a filing to the exchanges regarding “CLARIFICATION ON NEWS ARTICLE APPEARING IN EENADU (TELUGU) NEWSPAPER”. This was on the very next day of declaration of Q2FY26 results. We only know that something was posted about the company, which looks like it was quite speculative in nature, on page No.15 of the Business column dated August 10, 2025 of EENADU. Can any one of our Telugu friends on this forum dig out what was written?

2 Likes

HBL Engineering Limited has received a letter of acceptance from West Central Railway for a contract worth Rs. 54.12 Crores (inclusive of 18% GST) for the survey, design, supply, installation, testing, and commissioning of trackside KAVACH equipment at 18 stations over 166 kilometers in the Kota division. The contract is to be completed within 700 days.

The total order book of HBL Engineering is Rs. 4,083.17 Crores.

4 Likes

seems they misreported the numbers

Please see the section related to HBL

The translation of this article

Hyderabad:

Public sector company HBL Engineering (HBL Power Systems Limited) has reported a net profit of ₹139.73 crores for the first quarter ending June 30, 2025. The company earned ₹607.38 crores in revenue during the quarter.

In the same quarter last year, it recorded ₹516.77 crores in revenue and ₹74.25 crores in net profit. The company stated that its board has approved a dividend of ₹1.50 per share for the financial year 2024–25.

End translation.

Translation generated by ChatGPT.

Edit: Removed the image, and linked the page.

9 Likes

current valuations look expensive .

| Scenario | PE Ratio | Target Market Cap | Change from Current |

|---|---|---|---|

| Bear | 40x | 16044 | -25.30% |

| Base | 50x | 20055 | -6.60% |

| Bull | 60x | 24066 | 12.10% |

2 Likes

Hi, 1 year forward PE seems lucrative as H2 is heavy for HBL. If they cross 3000 cr revenue this year, EPS will come around 22-25, upside still looks promising and there is still some scope for upside from current levels. I wont be surprised if HBL crosses 850-1000 by end of this year. Last 5 year HBL’s average PE is 47. Obviously It all depends on the execution. We all know that Kavach execution is in full swing from q1. If Industrial battery/ fuses business kicks in as well, revenue would be much closer to 3500. Disc : Invested.

7 Likes

How you have calculated targeted market cap ?

1 Like

based on mgmt guidance of 3000 crores revenue , approx 400 crores of pat based on the net profit margin and then you can multiply with the pe . In my opinion my table is a fair view.

2 Likes

I am looking at HBL Engineering for investment but has following concerns:

- I notice that all the promoters other than CMD are non technical in a company which is more positions itself as finding and filling technical gaps. And CMD himself is around 80years of age.

- While Kavach is becoming a revenue generator field now next couple of years, what is next? There seems no other significant revenue stream in Electronics or other verticals.

Considering above, I am asking myself is this stock a 2-3 year play or a long term bet?

3 Likes

Hi @AAInvestor you can read the thread from begining there are multiple potential revenue stream listed EDT / Fuze . They are potential hence may be not in price .

The management has been transparent from the start. And if you have doubts, please go through their yearly reports and past concalls. I started following this company four years ago, and since then it has grown multifold. If all their verticals kick in, it can grow multifold from here too. The only downside I see is not having quarterly concalls. But the best part is their silent execution. They talk less and focus on the deliverables. Their yearly report has a lot of interesting information about their future plans. Disc - Invested

4 Likes