There was already a move in HBL prior to the Kavach order announcement wherein stock price went up from its 200 dema levels of around 530 to 690 plus. With this kind of run up, part of the news is already baked in price. There are some players who play these kind of spurts and sell on news. To add to that we have a weak overall market which puts pressure on stock prices.

Kernex already rallied from 750 odd levels to nearly 1500 levels within 2-3 months, which is a significant move for any stock in such a short period of time. After such moves there will be periods of rest, in form of correction, or sideways movement.

There is a phenomenon called Street Lag. Here inspite of news out in open, stock prices often take time to catch up because of any number of reasons, be it weak markets, fancy for other stocks, so on and so forth. We see this commonly in some turnaround companies wherein inspite of a couple of good quarterly results, stock price takes a lot of time to move. Some people use this kind of situation to their advantage and make decent returns.

Stock prices move in mysterious ways in the near to short term. Longer term its highly correlated to earnings. That’s where long term oriented investors with good temperament have an edge.

Medha will get the rest of the chunk and they seemigly have a good order coming there way. Although medha is unlisted

Smart money tends to move before the news. CGPower order came in first and after that almost every TCAS play started to move in anticipation of approvals coming through

The Kavachu budget of 12000 cr for 2025-26 is already factored in as it is reflected in recent order wins. So nothing new here. However, the ongoing reaction in stock may be deep, which will be a buying opportunity for the long run.

This is my observation and I may be wrong. I have vested interest as I am currently holding the stock and intends to add more on dip.

Recent orders were for equipping locomotives with Kavach. Tracks/track side installations also need to be equipped, which is bigger opportunity. We need to wait for budget to get the actual picture, but if it is only 12K Crore, that includes orders already awarded, that is not great news.

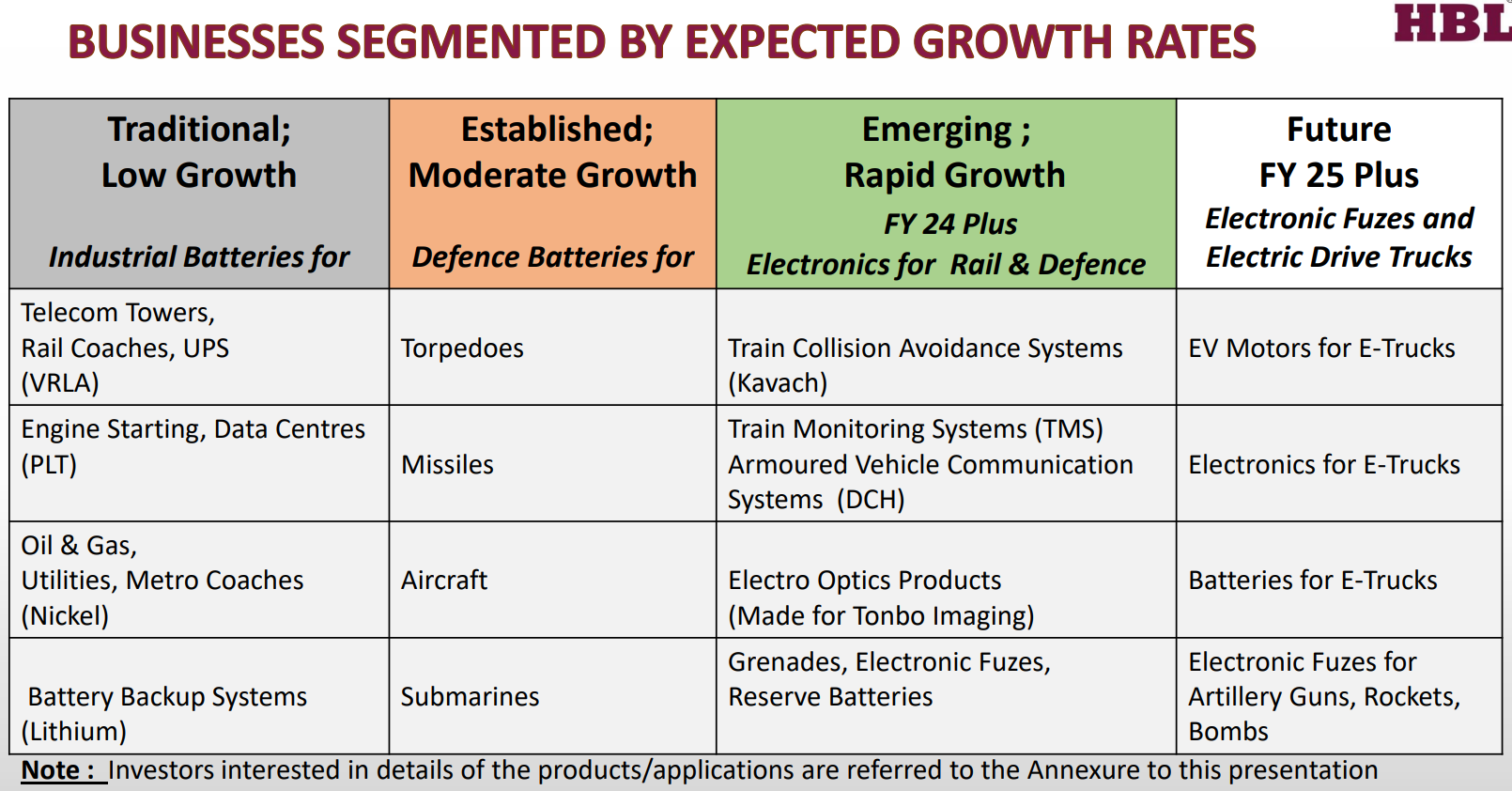

What we as investors also need to think about is what is the sustainable topline growth and margins for HBL.

The recent KAVACH order of 1522 crore is expected to be delivered by 20% EBITDA. But with emerging competition in the KAVACH space, is it likely that margins will dilute in the race to win more contracts?

With the investment cycle not progressing at the anticipated pace and may not catch up due to political realities (e.g., ladli behen). Can this risk be mitigated by selling this tech in other countries?

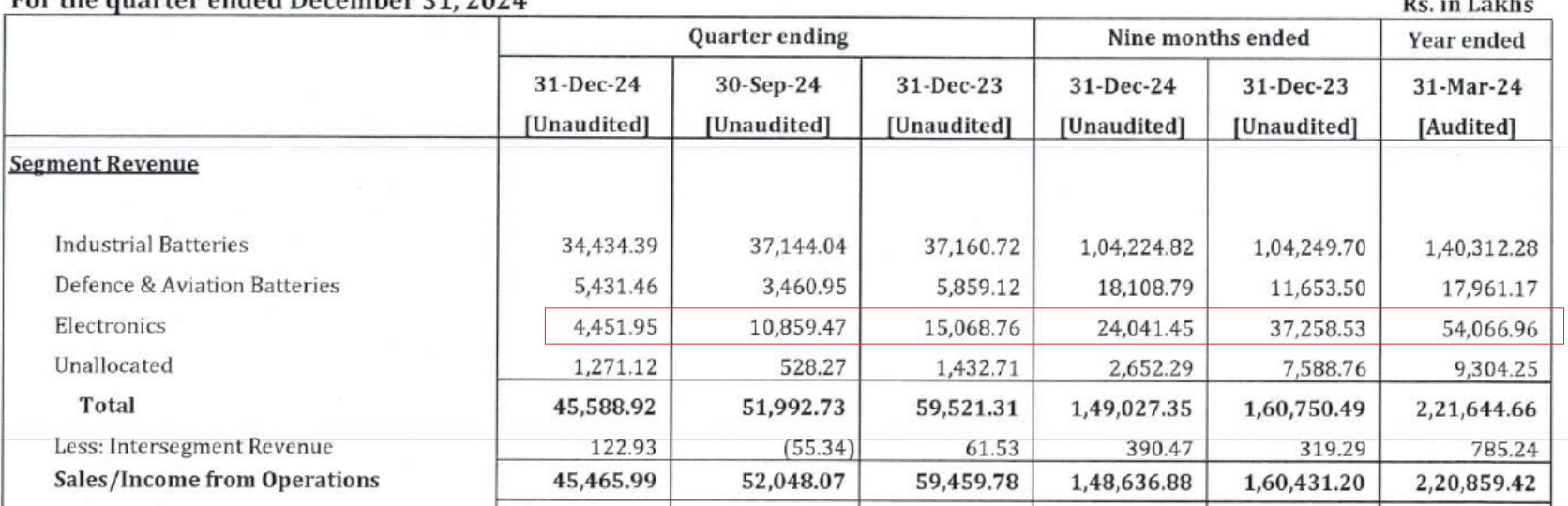

It is because of the lack of Kavach orders in hand for execution due to delay in order awarding activity from Ministry of railways because of the elections. Since the fresh Kavach orders have been awarded the FY26 could be a good year for HBL. That is the reason why the Electronic segment has de grown by 70% YoY. They have done a good job on controlling costs and also the battery raw material prices are trending down which has led to gross margins at highest level in foreseeable history.

HBL receives two track Kavach orders worth 499 Cr. This is 3rd update this year. Adding this, total track Kavach orders this year become 1058 Cr. Expecting few more track order wins this year.

HBL Engineering Limited (formerly HBL Power Systems Limited), based in Hyderabad, India received five letters of acceptance from Central Railway for the implementation of Kavach, a safety system. - Total contract value: ₹762.56 Crores (inclusive of GST). - Covers 413 railway stations and spans 3,900 kilometers. - Each contract has a completion period of 18 months. - The total value of all Kavach contracts awarded to the company during the year amounts to ₹3,618 Crores.

My observations:

I am holding this stock from Pre-Covid time and the management is very conservative in giving the guidance. So far, they are absolutely walking as per their talk.

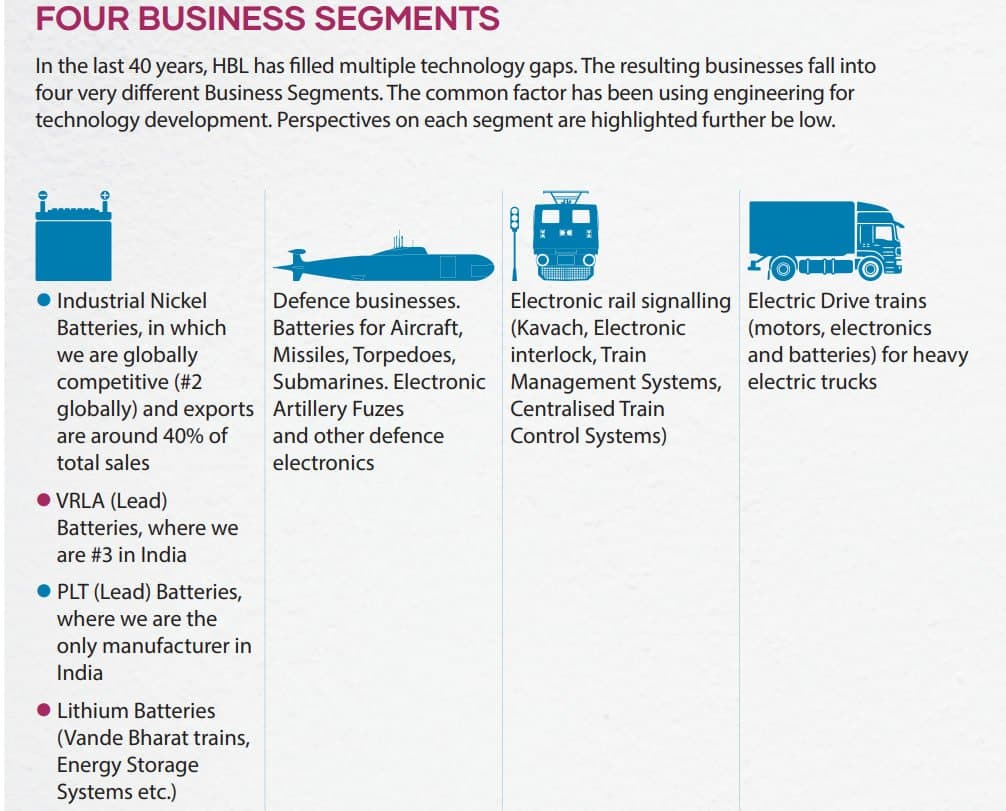

HBL Power spent more than one decade to develop this TCAS/KAVACH and it’s orders now getting in.

As management guided(We are focusing on margins only and not on top line), in the upcoming years their operational margins will definitely increase because of these orders.

They are having another big business verticals which are not started their action and out of these i am believing on their EV retro fitment vehicles and fuzes (related to defence sector) verticals. If they are also starts contributing then HBL Engineering will be in a very big league.

First order value is exclusive of GST while the others are inclusive of GST.

Company’s latest announcement shows total order value of 3618 Crores which seems to be inclusive of 18% GST.

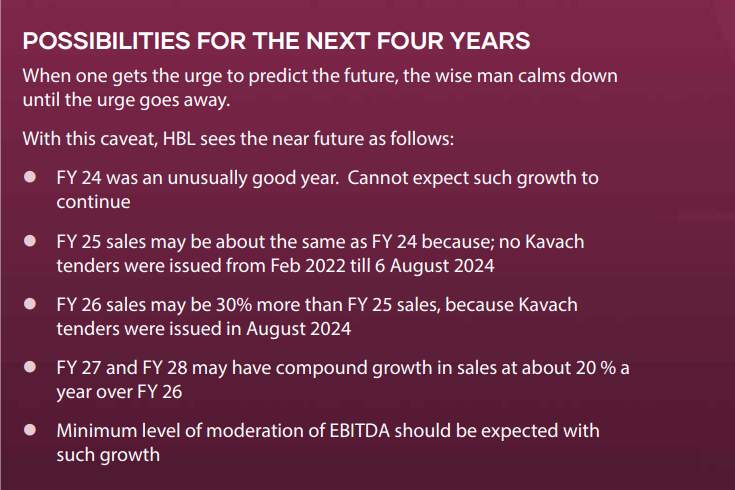

isn’t 30% growth over FY25 very very conservative? Given the duration of contracts, FY26 alone execution should be of Rs 2000 cr. The contract duration starts from the day of announcement right?