Business Overview:

Company was initially engaged in construction of residential projects. In FY21, company changed its line of business and is now mainly engaged in infrastructural development and works as a sub-contractor in executing various national highway road projects awarded by government authorities such as Maharashtra State Road Development Corporation Ltd and National Highways Authority of India. Apart from this, company has also started the EPC contracting business. New Promoter:

In October 2021, Mr. Pawan Mallawat acquired 25.93% share of company (through direct purchases and his company Keemtee Financial Services Limited) and has since been managing day to day operations of company. Order Book:

Company’s un-executed order book is at Rs. 1200 Cr. as on August 31, 2022. The increase in the order book is on account of receiving the balance part of work order of Nagpur-Mumbai Super Communication Expressway Limited of more than Rs.1000 Cr from Gayatri Projects Limited and originally awarded to them by Maharashtra State Road Development Corporation Ltd. (MSRDC).

Annual Report Analysis by CA Rajesh, who collaborate with me.

Positive:

There is phenomenal increase in Company’ turnover and profit that can be seen in financial statements. Turnover increased from 112 crore to 775 crore (Year to year basis) which is very impressive. Profit increased from 2.48 crore to 45.34 crore.

The main director Mr Pawan Malawat is not getting any remuneration. Further other director Mr. Dinesh is getting salary of only 6 lakh p.a. which is very nominal considering volume of business.

Co has recently appointed chief head / chief engineer for salary of Rs 6.00 Lakh per month which is good sign for aggressive operation of business.

Debt equity ratio has decreased from 0.9 to 0.26 which is sign of reducing debt.

Debtor ratio, RoCE and G/P and NP ratio has also increased which is also good sign.

There is no pending govt dues which is also good sign. Further there is no pending disputed tax liability with government which shows good compliance from Co.

Co has completed major portion of project awarded to it by govt.

There is no major negative comment by St. Auditor, Co secretary which also good sign.

Negative:

The director are getting salary less than most employees. There is no dividend declared except in current year 2023 and back to it declared in 2008. So how director are working without proper pay.

Co has appointed Independent director Ms. Pratima with nominal salary of Rs 5000/- p.m. again doubtful. Sebi has prescribed independent directorship for greater corporate governance.

The Co is not regularly paying dividend. It means co does not have good cash flow.

There is debt receivable of more than 44 crore which is outstanding for long time. In govt contracts, payment are received in 3 months except disputed bills. Even some debt is outstanding since more than 3 years and co has not written off it as bad debt which also not good sign as it artificially shows good picture. This can be ignored as new orders should not have any problem.

Auditor has not pointed any irregularity compared to some apparent things which i can see in fin statements and also firm is not big CA firm so question of due diligence arises.

Co has negative operating cash flow which is surprising considering increase in such profit and turnover. Negative cash was met by issue of fresh shares as mentioned in report. Means co has incurred and managed operating deficit from issue of capital from public. (This is very important).

Investment Thesis:

New management start bringing orders from 2021, it should continue.

Current order gives visibility for 1 year of approx. 939 cr.

New Orders must come in 1 year time.

Promoter should start increasing their stake.

Market cap to sales is only 0.26 and PE 4.

As of now, no negative in media for promoters as far as I searched.

Risk:

Micro cap

Promoter Holding of 26% only.

Inherent risk of Infra business.

No new order will consume current order book and there can be no revenue at all.

Note: As old thread was closed, as advised by Moderator, new thread is created.

Please contribute to understand business well and any red flag.

Disclosure: Have tracking position of 1.5% of my portfolio.

The company is available at very cheap prices no doubt. But certain things need more attention and clarification. If anyone can clear it up.

A. CEO is from the broking /securities background. How experience in broking background will help in roadways and infra business is anybody’s guess. I at least not able to see how these two fields can overlap, as experience in the broking industry is very different from the experience required to build roadways and highways.

B. I skimmed the annual report and noted there are only 9 permanent employees on the rolls. I am intrigued to understand how an infra company can function in a labor-intensive industry

Infra in India is a very difficult undertaking and would be watching the company to see how they shape up. D- No investments.

sougataG Thaks for your input, valid points. Let us continue to collaborate to dig deeper.

I tried to get information from their company secretary, however he did not give any further information and orderbook, future projects etc.

I call on members if we can contact management and understand their plan.

Disclosure: Invested.

Ascendant

Main item we need to track is new order. Orders in hand will be executed sooner or later.

Company do not do conference calls or investor interactions, so difficult to find what is going on inside.

Disclosure: Invested.

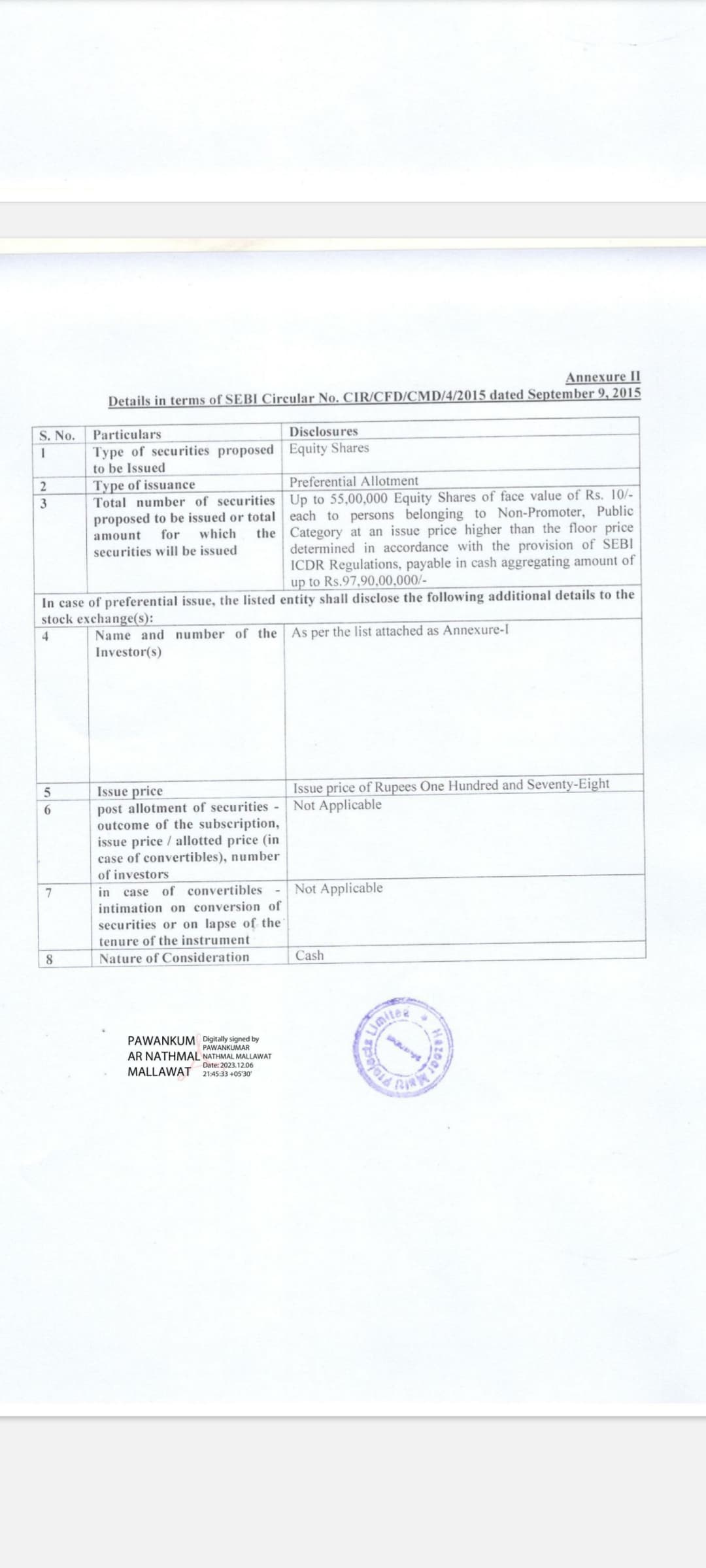

Board meeting on 6th December for-

-In view of considering new business opportunities, accelerate growth further and to augment the

financial resources of the Company, a proposal for fund raising, by way of issue of securities,

convertible instruments, or any other method or combination thereof through permissible modes, for

cash or otherwise, and to appoint requisite intermediaries required for this purpose;

At 202 and a market cap of Rs 306

Cr, Stock is selling for near 5 times earnings, 0.5 times sales, growing fast, Bagged humongous order of Rs 1200 crore…doing preferential issue …sounds too good to be true… obviously there are risks but currently odds are extremely in our favor…

Thanks Shail

Limited disclosures, relatively low promoter holding is already keeping investors on toes.

We would be benefited, if you can elaborate the red flags.

Regards

The Managing Director of Maharashtra State Road Development Corporation holds approximately 10% of the company. This is why the company kept on getting these orders.

A week ago he was relieved of his duty, but he is still part of the the director of CM war room for Infrastructure Projects.

As long as he is invested in the company, I have no doubt on the company.

Disclaimer: Invested 4% of my PF, and yes all SME are risky, they have these issues, that is why they are still SME and not Smallcap.

-9 employees generating 700 crores in revenue.

-Company is bagging 1200 crore in offset orders every year despite the promoter being a stock broker with no infra experience.

-Company is raising capital on one hand while doling out 22 crore loan to another infra company.

-The promoter takes no salary

-The executive director takes Rs 6 lakh salary

This all looks magical. There are more, but cannot be mentioned in a open forum.

Thanks Ascendant for the information related Managing Director of Maharashtra State Road Development Corporation holds approximately 10%.

At 5 PE everything is in price. Our bet is that if company continue to get new orders and execute it will have both engines firing, valuation and earning.

For microcap, there will always be some concerns, even apollo hospitals have concerns.

Let us hope, management do business ethically and grow.

Disclosure: Invested

Good to see more FII’s investing in the company. At least to me it seems that company should be able to execute orders, and these Institutes would have done some DD.