Ex Lloyds is better performance, seems to be trend for few quarters now. How long will this drag or turnaround - mgmt commentary will be key.

Q2 Result Update - performance

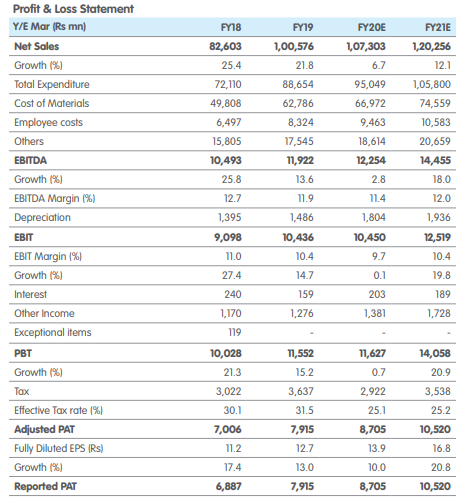

Havells India has reported a dismal performance in Q2-FY20, with revenue growing by mere 2% YoY to Rs 22.3bn led by muted growth across segments except ECD segment (+20% YoY) and Cable & wires segment (+7% YoY). Lloyd revenue declined by 30% YoY due to lower sales in LED panels. The industry experienced aggressive competitive landscape in LED Panels leading to substantial decline in prices, while AC sales were flat during the quarter. Switchgear sales declined by 6% YoY and impacted by slowdown in construction and new projects. Demand has further deteriorated from real estate to industrial and infrastructure segments. Cable & wire revenue has increased by 7%. ECD delivered a strong performance despite tepid market scenario. Investments in distribution and new products drive the growth. Apart from Fans, there is high growth from Water Heater, Water Purifier and Air Coolers. Margin of Switchgear and Cable & Wire improved by 146bps YoY, 442bps YoY to 39.9% and 18.4%, respectively. Aided by lower taxes at Rs237mn (from Rs754mn YoY) PAT increased by 2% YoY to Rs1.81bn.

Muted Revenue Growth barring ECD Segment

Havells’ revenue grew by a subdued 2% YoY led by muted growth across segments barring ECD segment, which grew by 20% YoY to Rs5.5bn. Lloyd’s revenue declined by 30% YoY to Rs1.8bn due to lower sales in LED panels and flat revenue of room AC business. The industry is experiencing aggressive competitive landscape in LED Panels with substantial decline in prices and soft off-take of room ACs. Switchgear revenue declined by 6% YoY to Rs4.0bn due to slowdown in construction and new projects. Revenue from Cable & Wire segment grew by 7% YoY to Rs8.2bn, as industrial cable demand impacted by delay in fresh government projects. EBITDA margin fell by 150bps YoY to 10.5% due to higher employee cost (up 18% YoY) and lower margin across segments except Switchgear and Cable & wire segment. PBT declined by 19% YoY to Rs2bn, helped by lower taxes PAT grew by 2% YoY to Rs1.8bn.

Outlook & Valuation

Market experts still like the business model of Havells, which is largely distribution-centric. With Lloyds in the portfolio, they believe the Company will continue to go for increasing its share in household spending. Looking ahead, it will continue to expand its geographic reach as well as product offerings. Havells is seen as one of the pure plays on likely up-tick in discretionary spend over the medium-term.

Rising pollution levels specially in Delhi has given opportunity to companies dealing in air purifiers. According to reports, air purifiers are among the fastest-growing products in the home appliances space. Rajiv Kenue, Senior Vice President at Havells India Ltd said, “The air purifier industry is touching 200 crores annually, which means two hundred thousand units of air purifiers are being sold per year.”

Lloyd’s poor showing was a cause for concern (it reported <30 per cent decline in revenue during the quarter). Analysts say Lloyd is dragging Havells down. “For Lloyd, although the near term appears challenging, the next summer could be a real test,” With the new plant (for AC) operational, margins and working capital benefits will be the key factors to watch out for.

Detailed report

Samsung’s reentry in lower end ac market may make it harder for Llyod to revive.

biggest wealth creator of the decade is trading close to 52 week low, any views?

On relative valuation basis, it is still at trading at a P/E of 54, which is not really cheap. For one year period it looks cheap as it had traded at 64-65 P/E levels.

Moreover, the acquisition of Lloyd hasn’t been turned out to be spectacular in last year or so.

Does anyone have a clue of how their famous dealer channel financing program really work? Do they have some risk in case of default? Any supporting document would be helpful

Lacklustre results

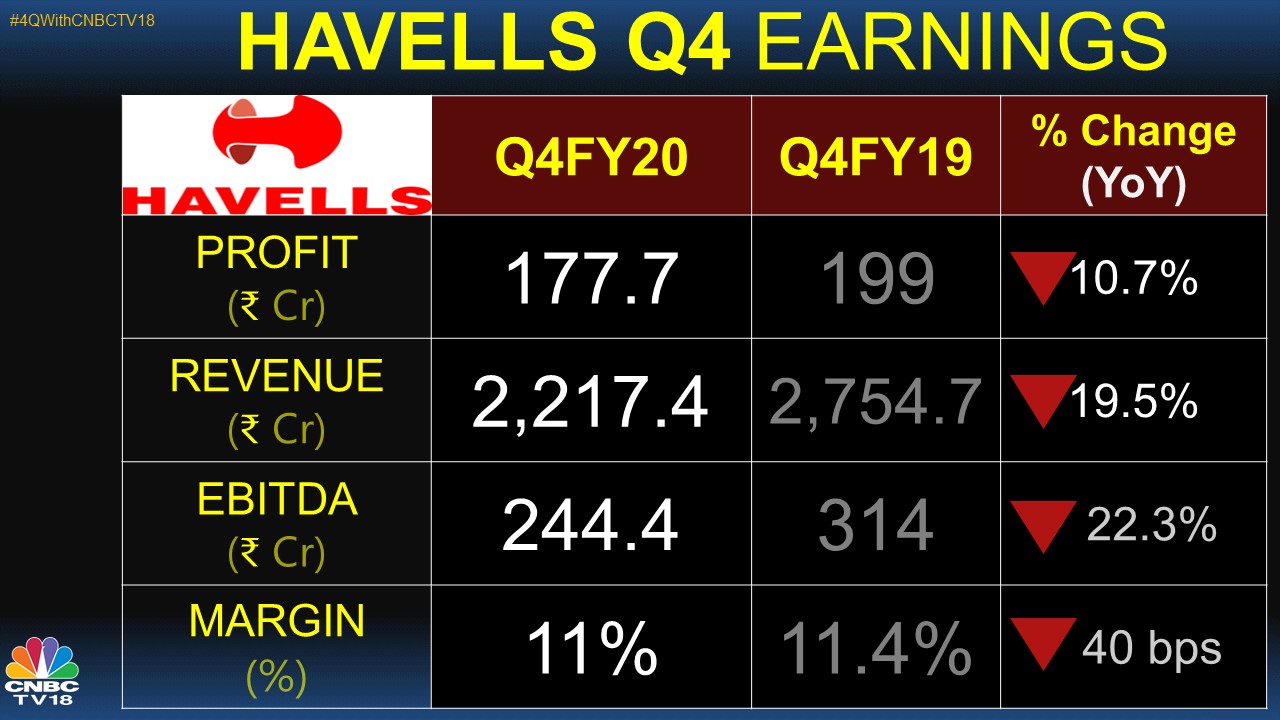

Worst result even though covid impact was not there in full Q4-FY20 but only few days. Now imagine what will be result in Q1-FY21where full Qtr will be washout!!

All these high PE stocks is still waiting for huge correction…this is applicable for blue star also

Most of MF and PMS have been taking cover under such high PE stocks considering safe haven! But wait for Q1 …when they forced to dump such stocks, correction will get accelerated!!

Per Investor presentation Ex Covid would have seen 9% growth for Qtr( assuming we trust mgmt), still muted performance for a High PE stock, almost 4-5 Qtrs now that Lloyd fails to perform and other segments slowing down too.

Annual cash flow and overall balance sheet stays strong, debt free

Stock has corrected from 700+ to under 500, at 40 PE it is surely expensive for de-growth delivered

Some trends that may work out in favor( theoretical yet)

- WFH trend to add tail wind to all B2C product categories ( 60% of revenue ) , some headwinds for B2B( wires etc - rest of biz)

- Supply chain efficiencies from own mfg plant ( mgmt commentary it was planned around Q1)

- Could they gain mkt share? - assuming competition with not so strong balance sheet comes under higher pressure

- Recent launches also aligns well with WFH trend( air purifiers, water filters etc)

With overall correction in mkt , the premium valuation is not deserved. will take final call post mgmt commentary and result trends with other players- Industry seems attractive though.

can anyone hep me to understand dependence of Havells on China

i got this article but still wants more insights

Govt eyes $17 billion investment proposals to boost local manufacturing

This article says that the government is looking to raise import taxes on ACs to reduce the dependance from China. This could significantly affect sales of Lloyd

The Company has setup manufacturing facility for Air Conditioners to achieve superior quality, product differentiation, better customer serviceability and efficient supply chain management system. The plant would have one of the highest level of in-house component manufacturing in the industry. It would be highly integrated plant having substantial levels of automation.

The facility has started operations in March 2019 and is expected to scale upto its potential towards the end of the year. Strategic shift towards local sourcing to substitute imports across product categories to insulate cost escalation caused by currency movements and custom duty hikes.

LIC increases shareholding by 1.44%, not sure if retailers have also followed the ace investor as no of retail share holders has increased by a whopping ~19000

I think the challenge Havells is facing recently are mainly:

- Polycab taking more business in wires and cables business.

- The growth in the Lloyd part of business is slow.

- Also there are many new entrants in the lighting category.

So I see them as continuous headwinds for a company asking such high PE.

I was invested in Havells, but moved out 6 months back and moved to Polycab instead whose earnings are growing at fast face and the valuations are still in affordable range.