Friends, what makes Havells such an expensive stock despite average growth of 17% as per FY18 annual report over last 5 years. Is it because of the dividend payout.

It has consistently grown for past decades. The growth will accelerate further because of acquisition. Has a very strong balance sheet. It given 37% CAGR returns for last 25 years. A very rare feat.

Very Bad Q4 results; Kotak’s target on this is reduced to 530. Goldman Sachs at 700.

Havells results are reflecting weakness in underlying demand. With weak trends continuing even in April and May (As per con-call), the first quarter results also will be challenging.

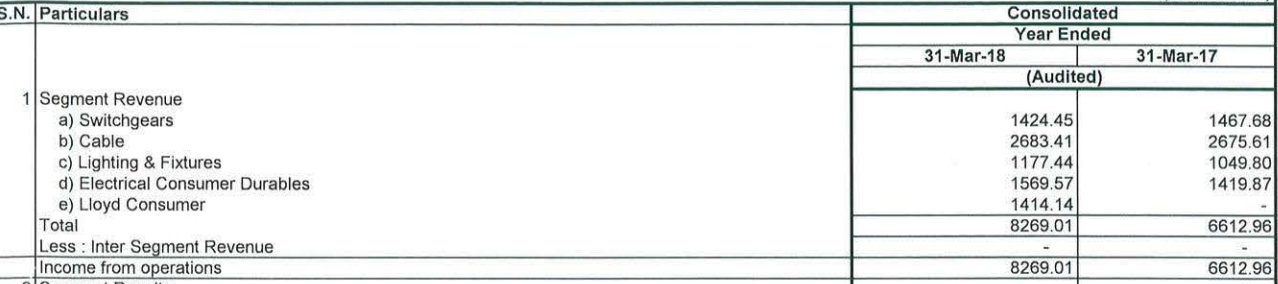

Lloyds have been a big disappointment on results and taking up a lot of working capital; Fans, Lighting and Switch gear hasn’t done well. Wires business is keeping up.

Don’t know why it still trades at 50x FY20 earnings. (At best we can assume a 15% revenue growth in medium term);

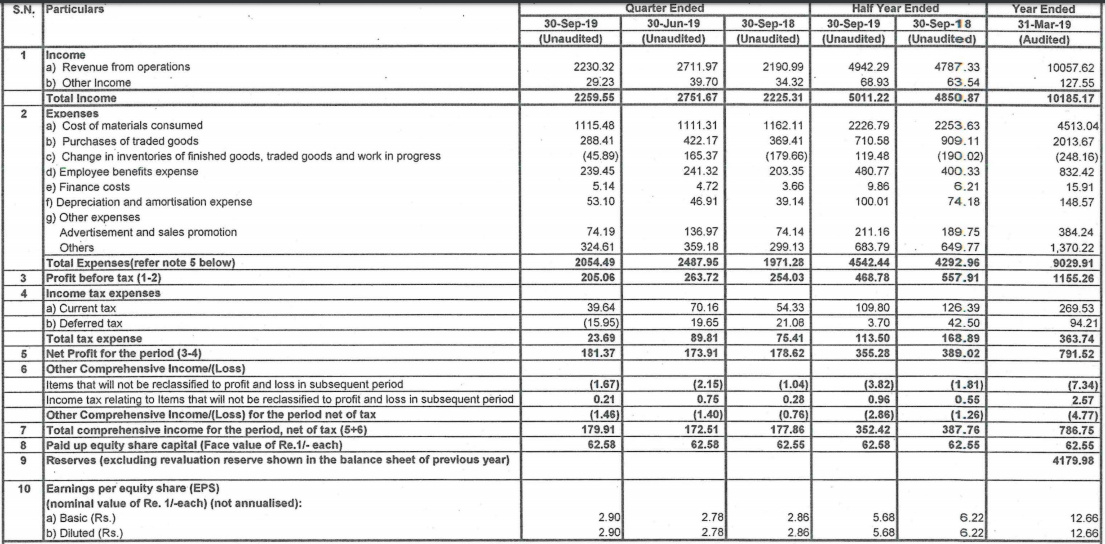

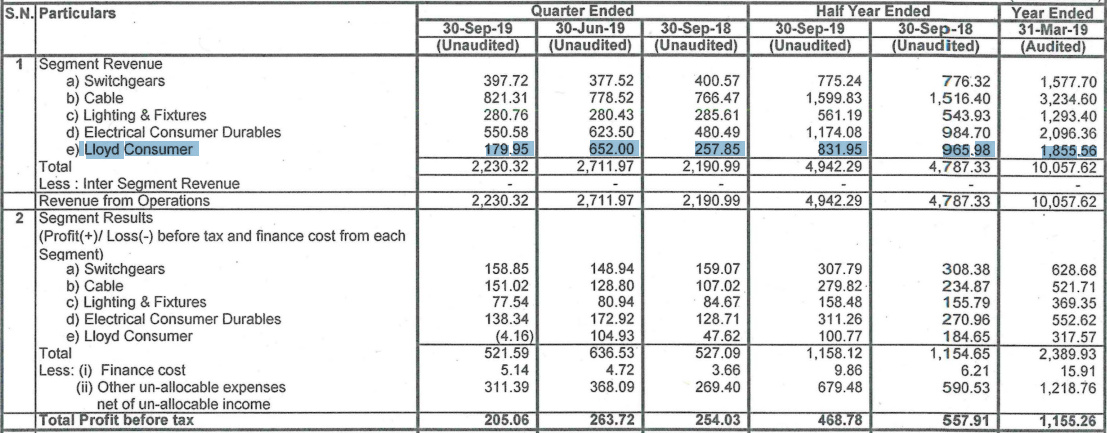

Q2 results don’t show any major change Seems Lloyd Consumer business hit it bad in the quarter

The entire sales decline in Lloyd is attributed to loss in LED panels. The industry is experiencing aggressive competitive landscape in LED Panels and substantial decline in prices. Revenue in Lloyd impacted due to industry-wide disruption in LED panels. Q2 & Q3 are lean season for ACs, accentuating impact of LED decline on composite Lloyd sales.

Q2 (YoY)

Revenues up 2% at Rs 2230 cr vs Rs 2191 cr

Net profit up 1% at Rs 181 cr vs Rs 179 cr

EBITDA down 11% at Rs 233 cr vs Rs 263 cr

Margins at 10.4% vs 12.0%