slow n steady great franchise

3 Likes

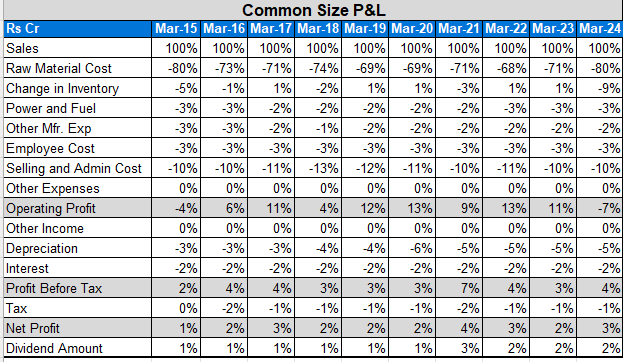

134 cr of NP mainly came from 140cr of gross profit, 73 cr of other exp reduction and increase of 73 cr of IT

why gross profit increased by 2.5% ?

- milk price went up and converted stocked milk powder to milk, and getting higher realisation ?

- higher sale of value added prodcuts added more margin?

why other exp went down by 3.8%?

hatsun analysis and questions.pdf (216.8 KB)

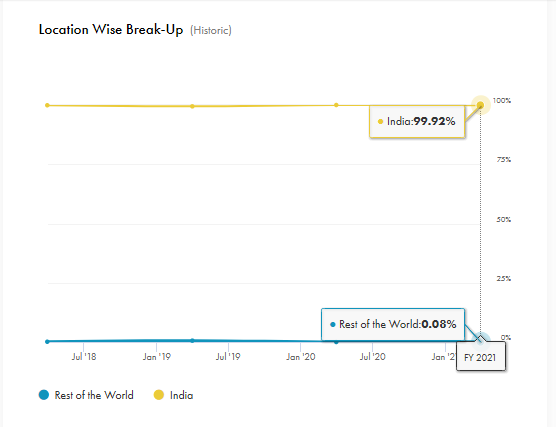

does anyone know from where 0.08% rest of the world coming from?

It’s coming from malaysia as Hatsun is present over there as well.

1 Like

Rights issue for Rs. 400 Cr. Record Date: Dec. 8th.

Milkflation views --18th Apr23 --BQ Prime --Hatsun Agro Products Mr. Chandra Mogan interview :

–There was a shortage but this year ( Calendar Year 2023) it will not be the same in future. Last year we had a diff. issues i.e after 2 yrs of demand destruction due to covid, Demand picked up internationally and domestic. The international fat prices went up dramtically to 583 INR in Indian Value & 7100 USD. So India started exporting before stablising last year so India exported over & above the normal Qty of Ghee branded, they exported 20k Tonns extra. Normally this Qty is built for the lean period in a flush period to protect.

–So after this there was a shortage and inflation started creeping in. I dont expect further inflation

–Demand/Supply mismatch ? --2 things have happened. (1) 20k tonns of extra export of Butter which is the real problem so this was in Jan/feb. Going forward Delhi had comparatively so the flush of delhi extended by a month which is a good news.

–Our normal flush season in south starts from May & it has started now in Apr first week and gaining momentum & by the time delhi is shutting off now the south and Maharastra has started coming up so the problem was acute it was in Jan/Feb & not today and by June noone will be talking about Milk shortage etc and Inflation will also moderate to 3 to 4 % down by June/July.

–We dont think there is no need for importing now and the flush coming in now in south & MH and its too late and it will be damaging the local mkt.

–Peak prices ? do we stablise here ? —Dont expect any price increase here-after , cos had a tough time last year as inflation made them pay a higher price to farmers and the consumer prices they could adjust immediately so a year of this tough times is over and we are on track of recovery. It can only moderate after June but old prices will never come back as from these prices 3 to 4% it might come back only

–How does these price increases impact cos like yours ? – One major issue is skimmed milk powder is taxed at 5% , Milk is separated into 2 parts ( skimmed milk powder & Milk Fat & during the summer we reblend it to make milk to compensate the missing volume say 8/10% so this particular our GST rates are 12% for fat and 5% for Skimmed milk so this is getting added up on reconstitution and which is adding inflation pressures. eg. Fat at 12% + 5% SMP is adding cost by almost 8% to the full cream milk & we have requested govt to consider reducing tax on 12% to 5% for fat & with this move govt. can moderate the inflation by 2/2.5% straight-away

–Price increases like this , how it impacts biz prosects for a co. like yours ? – In the long run its good for co. and country. After 2 yrs of covid farmers were in a shock to whether to focus on this or not & this inflation has given him a leg up and he will be in biz and will continue to supply . I expect that we are on the moderation of coming down by June end.

–Margins–Till march we couldn’t maintain but here after it will be a normal year subject to no other volatility.

PS : Pardon the spelling mistakes

6 Likes

Thanks for summarizing the interview. Dairy industry is FMCG that trades at relatively cheaper valuation. Hatsun is richly valued though. Invested in Dodla which is 2nd best in segment. But with growth it can reach the operating metrics similar to Hatsun.

Highlights of the Interview given by Mr. RG Chandramogan, Chairman of Hatsun Agro Products Limited with CNBC TV-18 on 11th May, 2023:

-

On Milk Inflation: In Q4 FY23, the company’s gross margins came at a 24 quarter low. However, the raw material inflation, i.e. the milk prices have started softening from April onwards. And the commodity prices have come down by 3-4% in April. Going forward, the company thinks FY24 will be a normal year after 2 years of disruption.

-

On Gross Margins: Gross Margins for FY24 will be approximately 3% higher than FY23. Which comes to 30%.

-

On demand trends in FY24: Milk is growing at a comparatively lesser pace, but ice-cream and curd are growing much better and faster. Overall growth will be better than last year.

-

On Milk Volumes: In Q4 FY23, milk volume sales were stagnant. But in Q1 FY24, milk volumes are stepping up and things are improving. All the price corrections to combat inflation have been taken in Q4 FY23 and the market has settled. Inflation is behind and prices can cool off in the coming months.

-

On lumpy skin disease: The lumpy skin disease is a history now and the problem exists no more.

-

On FY24 Revenue guidance: Double digit revenue growth is definitely possible in FY24.

-

On Capex: Over the last 4 years, the company has incurred a capex of Rs 1500-2000 crores. The increased gross block due to this will have a peak revenue potential of Rs 10,000 crores. FY23 revenues were Rs 7,500 crores.

Taking cues from Mr. Market, the company’s stock has started trading above all its moving averages. Also, the share price of other dairy companies such as Parag Milk Foods and Dodla Dairy have been trading above their 200 EMA since a month or so.

Although Hatsun trades at stretched valuations compared to its peers, it seems that taking a position here can be good for one’s financial health on the back of improving business operations! ![]()

3 Likes

First time in last 10 years Negative Operating Cash Flow -71 cr, mainly due to huge unprecedented build up of inventory 1452 cr…

Greed:This will definitely help it achieve 3000cr+ turnover in Q1FY25 and 10000 cr+ FY25 and good margin(stable milk price) and industry tail wind will improve overall financial performance, may be best ever.

Fear: Company is negative on operating cash flow, has increased almost same amount of debt as operating profit for the year and even its dividend are funded by debt for last 10 years. and it cant survive without incremental debt. it may be beginning of end

Disc: Invested

1 Like

Hatsun is a quality trap imo. I have posted some concerns in the past like equity dilution, ever increasing debt, high depreciation, low taxes etc.

1 Like

Update on Acquisition of Shares of Milk Mantra Dairy Private Limited

On January 29, 2025, Hatsun Agro Product Limited (HAP) completed the acquisition of 7,613 equity shares Of Mantra Dairy for Rs. 0.32 Crores.

HAP has now purchased a total of 30,80,546 equity shares and 16,06,372 convertible preference shares for Rs. 231.40 Crores, representing 98.14% of the Target Company’s equity and preference share capital.

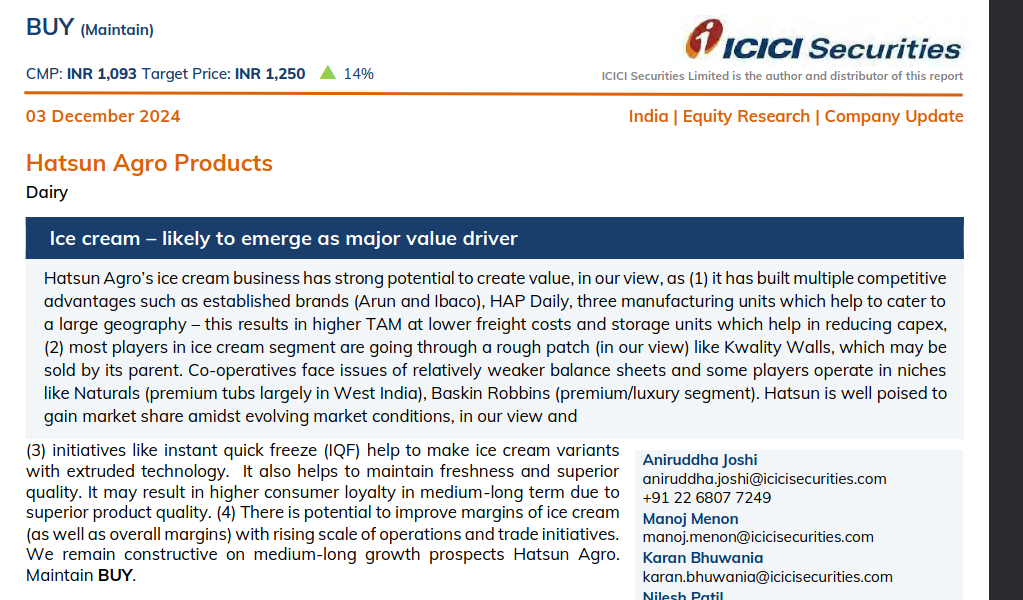

Very richly valued stock and maker of Arun, Ibaco ice creams - has grown sales at ~11-13% in 3-5 years and profits have fallen due to higher Raw material costs that seems temporary

Analysts are very positive about this

Company has invested in capex well and consistently at 500-600 crore yearly. The NPMs are very low at 2-3% that makes me wonder if it is better to put money in a fixed deposit than invest in a company that only makes 2-3% NPM

Hi @rkirana, your comment reg. might as well invest into FD really got me worried and had to get back at the basics.

Firstly NPM is not the measure of return on your investment.

For that you have ROE. Hatsun has had a 20% ROE for over 20 years. Decreased over time however due to accumulated retained earnings.

and for capital employee through long term debt usage, you need to look at ROCE (which is also reasonably good).

3 Likes

7a0b3557-9037-467f-bbab-0f3b256ac0c7.pdf

Can you tabulate FY25 number